Pin-insights

Apple's strategy - rebalancing the loss of momentum in smartphones with a broad push in Services - is a considerable challenge and sales over the past three quarters are not conclusive either way

Success - or failure - can only be ascertained over the next few years and the complexity of the company-wide transition should not be underestimated

Today, a few markers stand out and we hope to argue convincingly about their decisive importance in achieving the company's goals

- In developed markets, on which Apple's high priced gear will have to rely, Europe is an essential complement of the company's strength on its home turf - loss of market share in Europe to the benefit of Chinese competitors (Huawei and Oppo) is dismal and has to be addressed with great urgency

- Sales in China, still significant at $32.5 billion over 9 months (vs Europe's $45.3 billion) , are hit by the combined impact of domestic competition and trade conflict, with a 20% drop over the period. Apple may have to settle with further decline of its market presence and pursue alternatives - the scenario hardly looks improbable

- Services, a critical tenet of Apple's new approach, will only be as relevant as the installed base of hardware allows. At this early stage, Services should not distract from a hardheaded defense of current iPhone sales around the world

***

A fine quarterly balance

Apple's

The gist of Apple’s strategic shift boils down to a simple argument

- Sales of smartphones are expected to remain stable with a slow downward tilt

- Services are a fast-growing segment, diversified and expanding into new categories (such as branded credit cards)

- Services generate a gross profit margin which is in fact much larger than for ‘products’ of which smartphones are the major part

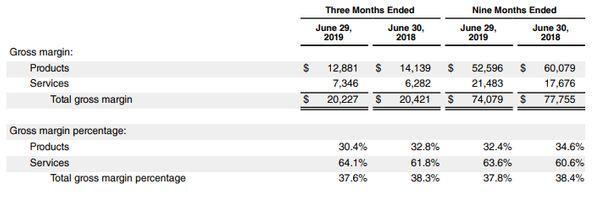

With slight decrease in gross profit margins due to foreign currency weakness and - primarily - to lower iPhone sales in the last quarter according to the 10-Q report, gross margin percentages are holding up quite well with growing margin on services

While attributing margin growth to a different product mix as well as to leverage of the fixed cost structure, actual breakdown of margin contribution by service category is not provided by the company

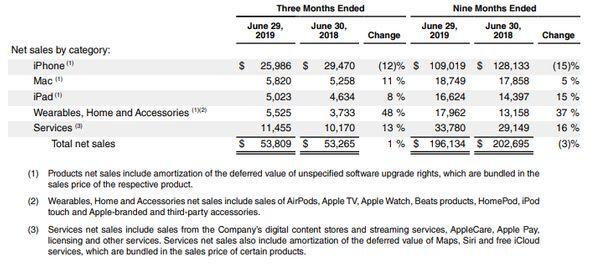

Because the contribution of Services to total gross margin is rising fast - from 22.7% (9-m 2018) to 29% (9-m 2019) to 36.3% (last quarter ending June 2019) - the resilience of the various segments appears to become critical

With the overhang of global trade uncertainties, given additional momentum with the new tariff announcements made by the US Administration, the early August 10% share price drop (partially retraced) may – or may not – reflect company-wide concerns

The business strategy is as credible as today’s market environment, with (fairly) open trade venues and a sturdy legal framework

Without being blindly optimistic, and with fairly priced shares at an affordable price/earnings of 17, Apple does have some room to correct business assumptions as they need to be confronted

However, if the fundamentals of Apple’s business model turned out to be in jeopardy, deeper issues might emerge

- Apple’s supply chain is a model of the global economy and the company is understandably loath to reconfigure an approach in the face of what may be a wind gust, not a destructive tornado

- The legal challenges brought to the company are being treated one case at a time, not as the social protest confronting Apple’s ways of doing business they might turn out to be

All things considered, Apple’s management is right to hold back today : global trade, and the leeway offered by competitive market-oriented structures and by tax laws, may return to familiar grounds

Or they may not …

A tilt or a slide

Sales numbers for iPhones, the company flagship, have stood out for many years - with contributions to company revenue (more than 62% on average, year after year for 2015-2018) punctually reported in the 10-K annual report

Since 2015 (230 million smartphones sold), Apple managed to defend its market share (212 million in 2016, 217 million in 2017 and 218 million units in 2018)

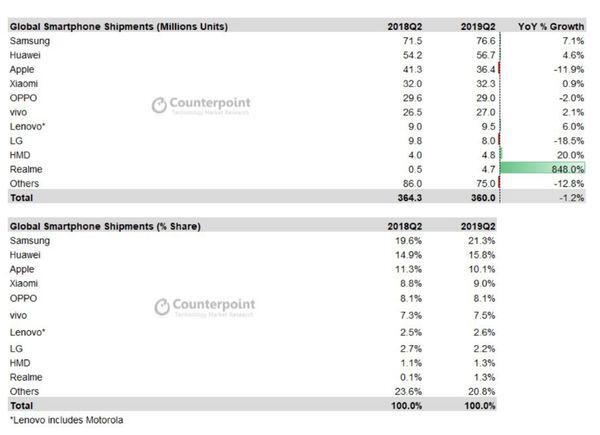

The 9-months sales reported in July '19 tell a different story, one of a loss of momentum with iPhone sales down 15% (at 55% of total sales), still trending down by 12% year-on-year in the latest quarter ending in June with the share of iPhones dropping below half of total sales (48%)

Hardly a tilt, the downturn has structural and geopolitical causes

- structural with close to perfect coverage in Apple's choice markets, slowing replacement patterns, costly next-generation phones, sharp-priced competition in emerging markets and lack of innovative breakthroughs

- geopolitical with stalling trade negotiations, weakening Apple's acceptance on the Chinese market and exposing potentially its supply chain

Apple's buyback programs have mitigated the duration people hold on to their phones (originally two years on average, creeping up to three years today) but the impact on 2019-2020 sales of delays in expected roll-out of 5G and phone availability in coming quarters may push holding periods up again

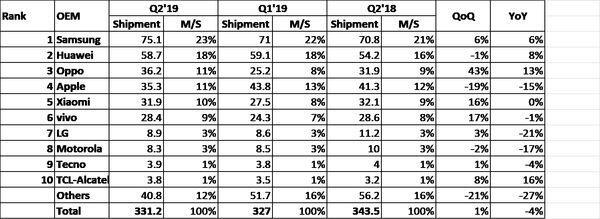

With the exception of Apple

- Samsung (listed on South Korea exchange - ticker 005930) maintains its lead with a 1.7% increase in market share in Q2-2019 and a 7.1% year-on-year sales increase

- The Chinese makers, taking the second, third, fourth, fifth and sixth rank hold a market share of 43%, up 1.4% in the quarter, not including HMD (phones manufactured by Foxconn under Nokia brand) up 0.2% and RealMe (an OPPO spin-off) up 1.2%

IHC Markit Research confirms worldwide trends mid-year with a 4% drop in global shipments year-on-year and a 15% fall in iPhone shipments (upping the Counterpoint quarter-on-quarter Q2 estimate of 11.9%)

Pushing Apple down to 4th place, Oppo's growth spurt stands out - with a 43% increase in shipments quarter on quarter - presumably because of a strong showing in India

(We hope to discuss the presence of Chinese companies in India in a follow-up report shortly)

Walking a tight rope, Apple needs to set its key decisions right

- the company's strengths in developed markets is the outstanding result of a far-sighted marketing and retail strategy - a powerful presence in the US but also in Europe. By going on the offensive, Apple still has time to build on its strong base of faithful customers - as we discuss in Pressing Priorities, our follow-up report

- services are unquestionably a valuable source of additional revenue but not an end in - and by - itself, as we hope to show in 'New Global is Local', to be published shortly

As if it were not enough, legal challenges will keep swirling around the company, calling for still more far-going decisions, detailed in the 'Legal Challenges' series