Pin-insights

The 2019 anticipated 18.4% pull-back of global semi-conductor manufacturing equipment capital expenditures (capex) must be placed in context of the very strong growth since 2015, almost doubling volume from $36.5 billion to $64.5 billion in 2018

Driven by the conjuncture of semi-conductor demand (data centers, automotive applications, Internet of Things, 5G) and technological advance (extreme ultra-violet process, 3-D memory stacking), close review of investments in Asia highlights a determined push by legacy suppliers (located in South Korea, Japan and Taiwan) to maintain their shares in the global semi-conductor industry

While the 'foundational' stranglehold of foreign (mostly U.S.) equipment suppliers on China's ambitious semi-conductor program has been bandied around in the U.S., capex investments for equipment in China increased by 60% between 2017 ($8.23 billion) and 2018 ($13.11 billion)

Involving both Chinese and foreign semi-conductor firms operating in China, the capex investments, and the build-up of domestic expertise, clearly remain on track

China's 2019 capex may drop according to the latest SEMI projection (July 2019) but the country's ambitious plan of semi-conductor self-sufficiency will not be held back for long

***

According to the latest projections by US-based Semiconductor Equipment & Materials International (July 2019), global sales of semiconductor manufacturing equipment by original equipment manufacturers are forecast to fall 18.4% year-on-year in 2019 to $52.7 billion from $64.5 billion a year earlier

Taking the long view, the share of the 4 Asian countries set to dominate the semi-conductor industry have increased their share in world sales from 66% (2014) to 78% in 2018

- the increase is almost entirely related to China’s build-up of a domestic semi-conductor industry since 2016

- with equipment sales to China growing from less than $5 billion in 2015 to $13.1 billion in 2019, the country represents a 20% share of the global market in 2018

Amongst Asian countries, only South Korea has made a more significant push to increase its semi-conductor production capacity with a 133% jump in equipment acquisition from 2016 ($7.67 billion) to 2017 ($17.95 billion)

Many factors may explain the investment strategy of the South Korean semi-conductor conglomerates (Samsung Electronics, SK Hynix), but a $10 billion capex increase in 2017 cannot be entirely disconnected from China’s planning, launched the previous year and build-up ever since

While not on the same scale as Korea, Japan’s commitment to grow its semi-conductor production capacity is equally clear with a 40% increase in capex in 2017 (reaching $6.49 billion) and a further 45% increase in 2018 (capex $ 9.47 billion)

Taiwan, the fourth key Asian semi-conductor manufacturing hub, committed to a 27% capex increase as soon as 2016, with a capex of $12.2 billion, a level of investment expected to be maintained through 2020 according to SEMI projections

Shuffling the cards

As geopolitical considerations seem to weigh in on capex planning, projections have become haphazard

- In July ’17, strong capex in South Korea for the full year 2017 was becoming clear, but the magnitude was not (proj. $12.97 billion – real. $17.95 billion – a $5 billion miss)

- Capex projections for China have been even more difficult to pinpoint – growth between 2016 and 2018 doubled capex from $6.46 billion to $13.11 billion but neither SEMI nor any other industry expert might confidently project capex – and related import approvals – in 2019/2020 in a conflicted trade context; analysts are suggesting a modest fall back in the current year while getting back on a growth trend in 2020

| China capex actual investments and projections 2016/2020 | |||||

| $ billions | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|

| SEMI proj. date | (proj.) | (proj.) | |||

| July 17 | 6,46 | 6,84 | 11,04 | ||

| July 18 | 8,23 | 11,81 | 17,32 | ||

| Dec. 18 | 12,82 | 12,54 | |||

| July 19 | 13,11 | 11,69 | 14,5 | ||

| actual capex in bold | data sourced from SEMI | ||||

Asia firmly in command

Based on capex by country, as ascertained in 2018,

- Asia dominance in terms of capex investments, year after year, is absolute – at 78.2% in 2018 and still growing

- North America has apparently lost its footing entirely – with investments dropping from a 21.8% share of global investments in 2014 to a projected 8.8% in 2020

- Europe has remained a stable, albeit minor, player with a 5 to 6% share of global capex

| Capex / Country | 2014 | 2016 | 2018 | 2020 (proj) |

|---|---|---|---|---|

| China | 11,7% | 15,7% | 20,3% | 24,7% |

| South Korea | 18,2% | 18,7% | 27,4% | 20,0% |

| Taiwan | 25,1% | 29,7% | 15,8% | 19,6% |

| Japan | 11,1% | 11,2% | 14,7% | 15,3% |

| Sub-Total | 66,2% | 75,2% | 78,2% | 79,6% |

| North America | 21,8% | 10,9% | 9,0% | 8,8% |

| Europe | 6,3% | 5,3% | 6,5% | 5,7% |

| Pininvest - credit for capex statistics - SEMI | ||||

Because of strong growth in global semi-conductor manufacturing equipment, the Asian effort is even more spectacular

- in 2016, Asian countries invested $31 billion in the technologies and capex recorded for 2018 has been $50.5 billion, a 62% growth in two years

- in the same period, North American capex did grow from a much smaller base and at a lower rate - $4.5 billion in 2016 and $5.8 billion in 2018

The long and the short

At a glance, projected trends for equipment and for the semi-conductor market at large send a dismal message, short term

- according to the industry, equipment manufacturers expect to be down more than 18% in 2019 and the course correction of 2020 would still leave the industry 9% below 2018 record capex sales

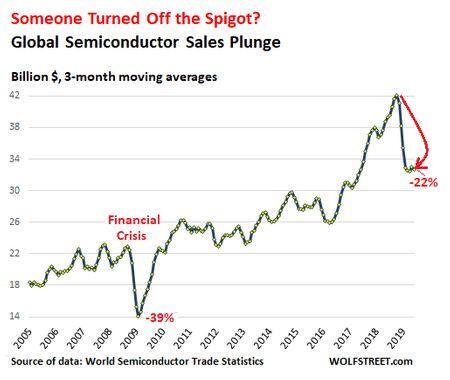

- the chip manufacturers have little to show on their end, with a sharp drop in global sales

As reported on Wolf Street, [June] was the fifth month in a row that the three-month moving average has been in the range of $32 billion to $33 billion, down about $10 billion from the peak in October last year, the steepest dollar-drop ever

The observer is left in a quandary when the performance of the Pininvest theme 'Semiconductor manufacturing' must be discussed against such a background

Ignoring the large market dip of year-end 2018, the theme notches up a 25% performance from early October '18 (a peak month of the semi-conductor industry)

Rather than looking in the rearview mirror for an explanation, a few observations might be relevant going forward

- China's push for domestic semi-conductor production still has a long way to go and will be pursued doggedly

- Current semi-conductor majors - located in South-Korea, Taiwan and Japan - are determined to hold on to their market share

- Capital expenditures in the industry requires 3-5 year planning and the dominant players, caught in a competitive race, uder a geopolitical cloud, have no choice but to engage

- Equipment manufacturers and semi-conductor firms are confident that the recent fall-back in sales is a hic-up related to maturing smartphone business, temporary slow-down in data center demand and cooling of the crypto-mining excitement

- Within the capex timeframe of the industry, demand for chips is assumed to grow exponentially as 5G, Internet of Things and Automotive come of age

The vision will undoubtedly be tested by global market reversals and geopolitical uncertainty, making the industry's broad commitment more credible still