We wish to acknowledge that the July 2019 report published by S.Horn, C.Reinhart & Ch.Trebesch under the title 'China's overseas lending' is the main source of information for this note

Pin-insights

Grown very large over the last decade, China's overseas loans and financial investments remain mostly outside public discourse while ubiquitous Chinese trade imports cause much hand-wringing in the world's advanced economies

Financial flows invested in sovereign bonds issued by developed countries retain straightforward dimensions of portfolio asset allocation, well known but hardly commented by the general public

Loans in emerging markets and low income developing countries, extended by Chinese state entities in all instances, are much less transparent and contractual terms align almost always with commercial practice (maturities, market rates, collateral backing and secret arbitration clauses)

By nature, Chinese bilateral contracts benefitting low income countries are not fully accounted for by international institutions such as the World Bank or the Bank for International Settlements, except for partial Chinese reporting

The ignored financial flows - qualified as 'hidden debt' - are of special interest because the beneficiaries are in fact a very small number of poor countries, exposed to a large debt load and probably unsustainable debt service

Financing the Belt and Road and beyond

While China’s global ambitions to remake the world’s transportation infrastructure has been popularized under the ‘Belt and Road Initiative’ (BRI) moniker, the terms of China’s financial engagement in the projects remain difficult to evaluate and partially hidden

A few instances made the news

This was the case for the July 2017 debt-for-equity swap of Sri Lanka’s Hambantota port which gave China a 99-year lease for managing the port, as Sri Lanka proved unable to honor a $6 billion loan at commercial rate of 6%

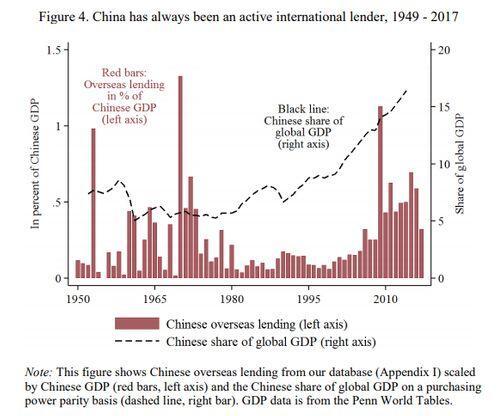

However, China’s active involvement as international lender is not new and since 1949, the country’s leadership has been extending bilateral loans and grants to selected communist allies, representing a sizable share of GDP, even during periods of severe hardship – S.Horn, C.Reinhart & Ch.Trebesch study, fig. 4 page 11

Percentagewise, estimates of China’s international lending today remain comparable to past record (ranging from 0.5 to 1% of GDP) and almost all of China’s overseas lending and investment is official, meaning that it is undertaken by the Chinese government, state-owned companies or the state controlled central bank

A game changer

China’s share of global GDP took off in the early 2000’s, representing more than 19% of world GDP at purchasing power parity as of 2019, according to the IMF (vs 7.4% in 2000)

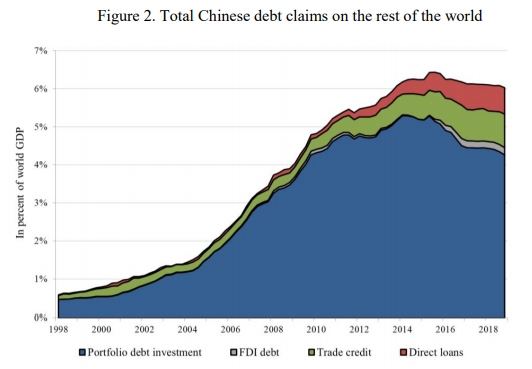

Correlated with GDP growth, China’s financial outflows in the form of official lending have transformed the Chinese government in the world’s largest official creditor (the US remains the largest overall creditor, after including private bank lending) – S.Horn, C.Reinhart & Ch.Trebesch study, page 6

Backed by the well-documented surge of the Chinese economy, the role of China in international finance has been compared to the rise of US lending after the world wars of the 20th century – and to no other occurrence in history – establishing the country as a dominant player in less than a decade

Accounting for China’s portfolio investments to advanced countries (sovereign bond purchases, guaranteed trade credit, equity and foreign direct investment (FDI) and central bank swap lines, aka standing lines of credit), the world debt held by China exceeds $5 trillion (6% of global GDP)

Direct loans and credits, mostly to low and middle-income countries, are reported on the balance sheet of China’s central bank, rising from 0 to $1.6 trillion (close to 2% of 2018 world GDP) in 20 years

Regarding low-income developing countries (LDIC's), these loans have been sizable, exceeding capital flows from traditional multilateral lenders

Credit extended to emerging markets by China is estimated to represent 25% of total bank lending to these countries

But, by occurring for the better part ‘under the radar’, their evaluation and the potential over-indebtedness of some of the beneficiaries are hardly reassuring

The study highlights the discrepancies between debt stock of the top 50 beneficiary countries, researched one by one and official debt- and creditor statistics (as reported by China in BIS statistics)

Quoting the S.Horn, C.Reinhart & Ch.Trebesch study (page 4)

For the 50 main recipients of Chinese direct lending, the average stock of debt owed to China has increased from less than 1% of GDP in 2005 to more than 15% of debtor country GDP in 2017, at least according to our lower bound estimates. For these countries, debt to China now accounts for more than 40% of total external debt, on average.

More importantly, using unpublished data from the World Banks’s Debtor Reporting System and data on BIS reported bank claims, we find that about 50% of China’s lending is “hidden”. Neither the IMF, nor the World Bank, nor credit rating agencies report on these “hidden” debt stocks, which have grown to more than 200 billion USD as of 2016

Lending with Chinese characteristics

China could – but did not – align its lending strategies with international standards

China is not part of the Paris Club and does not share debt sustainability data, does not communicate on trade credits (Berne Union / OECD), only informs on bond holdings and asset purchases in aggregate at the Central Bank of China and reporting of bilateral loans to the BIS remains confidential (as well as recent - 2015)

Furthermore, China is proceeding on a country-by-country basis, with bilateral covenants falling outside established international practice

The S.Horn, C.Reinhart & Ch.Trebesch study highlights a paradox – while all the capital outflows are official lending by state-owned banks and enterprises, the terms of the loans have characteristics of commercial lending in more than half the cases of the sample

Mostly denominated in US dollars (85% of the sample), at interest rates of 2 - 3% for low income countries (not the interest-free rates and grants often received from bilateral and multilateral creditors) and at market rates for emerging markets, the Chinese loans have on average shorter maturities and are often backed by collateral (in an estimated 50% of cases)

Enjoying a fair degree of seniority, including secrecy and arbitration clauses, repayment amounts, default and possible restructuring details remain outside the public domain

Simply stated, China’s official lending overseas diverges systematically from international lending practice as it has been understood since 1945, with emphasis on concessional lending, a grant element of at least 25%, very long repayment terms (30 years is not unusual) and transparency

In the dark

In carefully argued section 3 (pages 18-25), the S. Horn, C Reinhart & Ch. Trebesch study assesses that the under-reported Chinese loans are not evenly spread, but cluster around some of the lowest income countries, where the under-reported debt will represent a significant percentage of GDP (increasing the debt burden by 7-10% of GDP)

Putting aside extreme cases such as Angola, Venezuela and Zimbabwe (with under-reported loans scaled respectively from 13 to 20%), the debt-to-GDP profile of Asian countries in immediate proximity of China and resource-rich African countries has risen strongly after accounting for estimates of under-reported debt

While secrecy might enter China’s financial calculation, a more straightforward explanation suggested by the study is ‘circular lending’ of Chinese banks benefitting directly Chinese contractors of the infrastructure projects in low income countries, avoiding disbursement to the accounts of the debtor government and leaving the loans within the Chinese financial system

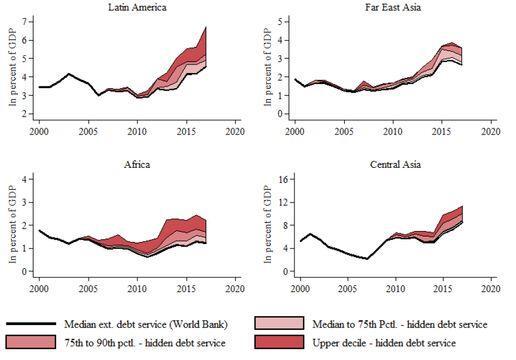

Debt burdens of the low-income countries – as detailed in the study on p.26 (fig. 17) – present even more critical profiles in terms of debt services (interest and loan amortization) after accounting for hidden debt (fig. 18), reflecting the high interest rates required on Chinese loans

While the sharp uptick in Latin America might be related to Venezuela's dismal economic status, Central Asia stands out with a 'hidden' 3% of GDP tacked on to already towering debt service recognized by the World Bank (8%)

The study, extensively quoted in this note, draws a dire parallel with the debt crisis of the 1970's, involving often the same countries, but declared sovereign defaults have in fact risen only modestly, although commodity prices have collapsed since 2012 and international capital flows have declined sharply

The authors conclude that sovereign debt restructurings and write-offs are a part of the missing defaults, credit events that should have occurred and did not .... Restructurings engaged by China and reported in the study since 2000 number 140...

If, as is frequently argued, overseas lending serves China’s broader strategic interests, the debt burden of Central Asia - and possibly of South Pacific Islands - should be carefully considered, the subject of our follow-up notes