All market cap estimates as of July 30, 2018

Pursuing the pent-up growth potential of rising Asian middle classes, Alibaba

Extending their reach beyond the digital world of sales intermediation and entertainment, the e-commerce and social network titans have entered the competitive field of online orders for offline services, or O2O, either with multiple minority stakes (Tencent) or through full ownership (Alibaba)

O2O is a catchphrase for goods and services that are purchased online, but delivered into brick and mortar businesses, like hotel, restaurant or movie ticket bookings, transportation services or food deliveries… and O2O, enabling physical retailers to reach new customers via the internet (and in particular the mobile), has special appeal in fragmented markets, where Internet platforms open vast choices at once

With more than half of online sales in China by smartphone, the close to 15 trillion-dollar mobile payments are also a key access point to consumer data

Unencumbered by established financial service providers defending their corner in advanced economies, the strategy is most spectacularly about building an unassailable moat in emerging markets, in a brutal, ‘take-no-prisoners’ concentration of fire power, integrating digital services and offline retail with control over the payment systems

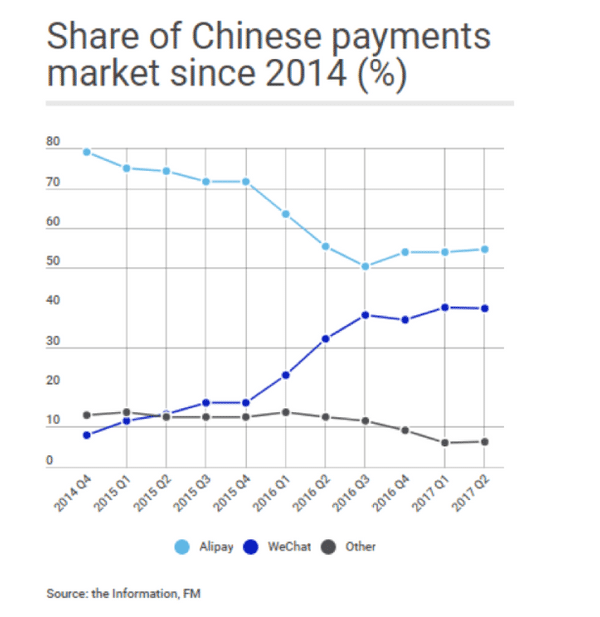

- Alipay, the mobile wallet launched in 2004 by Ant Financial, Alibaba’s financial affiliate, has owned about 80 % of the mobile market in 2013/2014.

- WeChat - Tenpay, launched by Tencent in 2013, as the mobile wallet of Chinese social messaging app WeChat, has fast been gaining ground – with a 40% market share by the end of 2017 according to Beijing-based consultancy Analysys

This is how we view the emergence of multi-billion players in Asia, firmly rooted in their domestic market, used as springboard to conquer Asian consumers next door and international markets further afield

Closely integrated with China's social and e-commerce networks as early investors, Chinese online digital travel is a model of things to come and a force to be reckoned with

Summarily stated, the standard bearers of travel in South East Asia, Ctrip and Meituan Dianping, are primed to dominate internationally

Ctrip

A $ 23 bn marlet cap as of July ’18

Covering everything digital - booking online flights, hotels reservations and packaged tours – Ctrip has built an impressive moat on the back of aggressive price wars, domestic take-over strategies and deep international partnerships

With a China digital bookings market share estimated at 36 to 45 % (accounting for partner Qunar), the market cap of Ctrip doubled since 2015

A model of cross- shareholding intricacies

- Ctrip Invalid tag asset partners with US-based Booking.com

(Priceline Group – market cap $ 100 bn) which potentially holds 10 to 14% of Ctrip capital through a close to $ 2 bn convertible bonds and equity investment. Ctrip and Booking.com share access to the companies' combined hotel inventory, allowing customers to select from price competitive products globally - Baidu

(China’s largest search provider and AI automation, market cap $ 80 bn PE 25) owns approximately 25% of Ctrip voting interest following a 2015 share swap, giving Ctrip a 45% interest in Qunar, originally a competing online travel service, which went private in 2016 at a valuation of $ 4.4 bn - A 38% equity stake in eLong, a mobile and online travel agency, bought from Expedia

and other investors in 2015, was subsequently privatized by a buying consortium including Tencent . Under the name of Tongcheng-Elong, the bulk of its customers come from Tencent-run social-media apps WeChat and QQ, which both offer access to the site, leveraging its ties to Ctrip’s large base of suppliers to expand - Following a private placement in 2015, Ctrip lost control of Tujia, dubbed the 'Chinese Airbnb', but entered into a strategic agreement with Qunar in 2016 to combine the vocation home rental businesses of the two Chinese online travel services . The homestay channels of both Ctrip and Qunar’s web sites, along with their operation teams and the entire business are merged into Tujia and the company also receives logistical support from Ctrip and Qunar, including inventory, traffic, branding and operations support

Meituan Dianping

Valued at $ 30 bn in 2017 - an IPO is projected at $ 60 bn (October ‘18)

Discussed in our Internet Service Platforms note

- Created by the 2015 merger of Meituan (backed by Alibaba) initially cloned from Groupon group buying and of Dianping (supported by Tencent) focused on restaurant reviews like Yelp , the company has been expanding into wide ranges of local services

- Meituan Dianping today is China's leader in O2O goods and services with a platform that offers food delivery and allows users to buy movie tickets, make spa and salon appointments, book transportation and hotel rooms, and access the bike-sharing program MoBike (acquired for $2.7 billion in April 2017)

- As of June’18, Meituan announced 310 million transacting users and 4.4 million active merchants with revenue growth from 4 billion RMB in 2015, to 13 billion RMB in 2016, before hitting 33.9 billion RMB (about $5.2 billion) in 2017

- With Koubei, its own O2O application, Alibaba sold its stake in 2016 (for approx. $900 m while Tencent has maintained a 20% ownership of Meituan