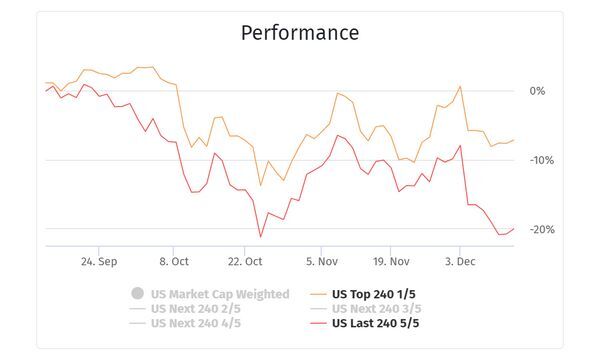

In our comment, 6 weeks ago, about Market indices in times of doubt, we explained how the sharp drop in performance of the 240 smallest shares in the total market index had anticipated the ensuing market rollback by about 10 days

After moving in parallel with the performance history of the largest 240 stocks over the past 3 months, the same pattern seems to be emerging with a sharp drop of the small caps, clearly unhinged from Dec. 4 on

Comparing performances over a 1-month time frame, the downward trend has been very marked since Dec. 4, opening a gap of about 8% with the large-cap equity segment

You may reset the pinindices charts by configuring the total market index for your chosen time frame to evaluate performance and volatility trends by segment in the sub-indices section

Since late September, when the downtrend took hold, our small cap segment has slumped by approx. 20%

Small cap constituents

Structurally, the small-cap segment of 240 companies is concentrated on 5 sectors, with Industrial Goods and Finance dominating with 40% of the category

Industrial goods 60/240

- Oil Services : 12 companies – the share prices were deeply impacted since October for many companies – with extreme cases such as Noble Corp

or Rowan Company Invalid tag asset or Nabors dropping by 50% - Metal Fabrications : 8 companies – though clearly slumping since October, companies such as Harsco Invalid tag asset did well in a specialized service segment and on a yearly basis, while EnPro

or AK Steel Invalid tag asset manufacturing flat-rolled carbon, stainless, and electrical steels, and tubular products appear to be impacted by tariffs, remaining on a continuous downtrend since the first quarter - Electrical power systems, Engines & Industrial components – on average, the segment did poorly, with companies possibly affected by postponed or canceled industry investments

Finance 38/240

- Regional Banks and Savings Institutions– 23 listed institutions - while the segment ends the year, on average, close to 0, very sharp drops of 20-25%, since early October for most banking shares such S&T Bancorp

or First Commonwealth Financial , impacted the whole small cap segment, with rare exceptions (First Bancorp ) or in financial services (Cardtronics Invalid tag asset)

Services 29/240

- Segments such as Home Improvement (Bed Bath and Beyond Invalid tag asset) or Automobile Aftermarket, Office Equipment and General Business Services have been doing poorly throughout the year, and only did worse since 3 months, which appears to signal weak consumer trends

Technology 27/240

- Nothing conclusive can be drawn from very diverse performance records, from briliant outliers (Evertec

, SPS Commerce or Fabrinet ) and from companies often harshly impacted by the October flow

Real Estate 26/240

- With exceptions, the category has remained strong on average – but integrated construction companies (Meritage Homes

or KB Home ) and real estate services (ABM Industries or HFF Invalid tag asset) did poorly throughout the year, signaling a deeper malaise

Overall, it will be noted that the small cap firms rely to a larger extent on borrowed capital (at about 3*EBITDA for the category) : interest rate increases will be hitting their bottom line, after years of affordable debt

Viewed in combination however, flagging demand with

- negative trends in consumer goods (home and car),

- weak order books of the smaller building operators,

- poor performance of the oil service industry

- uncertainty around equipment providers relying on industrial investment

- consequent impact on the regional banking institutions serving these businesses

remains the most probable factor of downturn

The trend requires our full attention - short term