Pin-insights

Chinese Financial Technology, or FinTech, has opened a window of opportunities in a mostly dormant market; 2013 is widely recognized as an inflexion point, launching rocket-like growth

We argue that consolidation and collapsing share prices of Fintech companies signal the first stages of financial realignment, leaving the industry in the cusp of radical transformations

How fast and how far the Chinese government will choose to go is not known in a balancing act betweeen the competitive advantage of a flexible payment- and lending system and the need to protect State banks and their vast army of employees

***

By its magnitude and by its profound impact on Chinese society, the stages of this radical upheaval, propelled by insatiable consumer demand, are difficult to apprehend - the tidalwave of the 19th century Industrial Revolution comes to mind...projected on the scale of the Chinese hemisphere

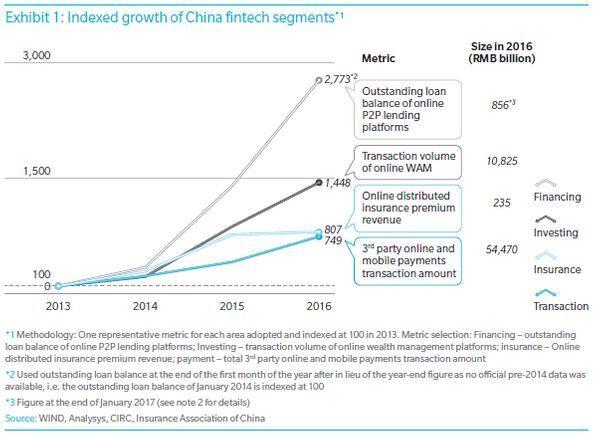

Highlighted by the Olivier Wyman chart over 3 years, online payments and online insurance increased by a factor of 8, online asset management 14 times and peer-to-peer lending 27 times...

Though spectacular, these trends could well be nothing more than a growth spurt followed by extended - and necessary - consolidation and the collapsing share value of a number of FinTech platforms might suggest so much

But this report argues that the early stages of this financial revolution, fairly substantial in urban China, are only part of the story,

- as mobile technologies explore new services,

- deepen their penetration of urban markets

- and engage vastly underserved rural China

However, the momentum to gain (or maintain) market share across different business activities will be costly

And to complicate estimates as FinTech permeates all sections of everyday life, the Chinese regulators are swapping the fine balance they had struck with novel - often experimental - financial services for a more constraining framework

The segments of the China's FinTech will be affected in very different ways as the regulators are enhancing their scrutiny

The new mix of regulatory scrutiny and market potential is likely to favor

- FinTech companies, positioned to deepen their coverage of urban markets and to serve the rural areas with flexibility, accounting for much lower average buying power

- established Internet champions, with the financial strength to take on the national markets of South-East Asia

- and, potentially, technology-driven firms prepared to recast the architecture of established financial institutions worldwide

At the nexus of consumer demand and technology

To measure the strengths of the contenders, an understanding of their foundational strategies is relevant

A three-pronged advance has led to exponential growth because of the convergence of mobile technologies, e-commerce penetration, underbanked consumers and underserved small business

Transformative under the impulse of new players and some established financial institutions, Internet lending, on-line insurance and third-party payments drive a deep integration of technology and finance

- Internet lending – in various guises of peer-to-peer (P2P) lending – is led with a 22% market share by Lufax, a subsidiary of esteemed Ping An Insurance (listed in Shanghai - ticker 601318)

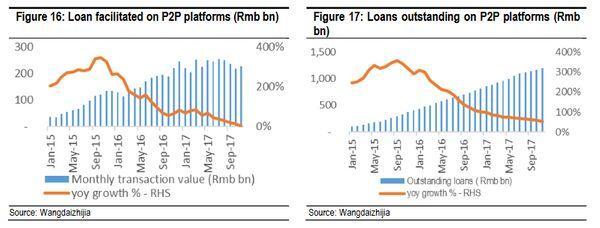

, but exponential growth of demand generated a large - dodgy and poorly regulated - domestic industry - With strict regulation, protective of the lenders and speeding up the compliance with the '108 rules', as of September '18 legal P2P platforms are expected to regain credibility following the shake-out

- P2P lending reached ¥ 1.2 trillion in 2017, from ¥ 856 billion in 2016, and the loan balance is stable at ¥ 1.3 trillion as of June 2018; the chart, sourced from Chinese wdzj.com, is indicative of the trends, by refering to total volume transacted and to the loan balance outstanding

- Insurance innovation was initiated by Hong Kong listed Zhong An (ticker 6060) Invalid tag asset , founded in 2013 with the backing of Tencent

, Alibaba (through affiliate Ant Financial), and Softbank (listed in Tokyo - ticker 9984) - China has become in short order the world’s second largest insurance market and growing fast

- According to statistics from the Insurance Association of China, online insurance premium scales increased 70 times between 2011 and 2015, contributing 9.2% of industry total that year

- Confronting different sources, the trend is unmistakable - $45.4 bn (2016) - $100 bn (est. 2018) - $145 bn (proj. 2021)

- With distinct business models, Zhong An, Ping An and Alibaba are leading the way

| On-Line Insurance in USD (billions) | 2016 | 2021(projected) |

|---|---|---|

| non-Life | 19,9 | 63,8 |

| Life | 25,5 | 81,2 |

| Total | 45,4 | 145 |

| Source CBInsights - O.Wyman On-Line Insurance Trends in China | ||

- Mobile – third-party – payment became a full-fledged, and world challenging, industry in a few years, powered by the Internet behemoths, foremost Alibaba and Tencent

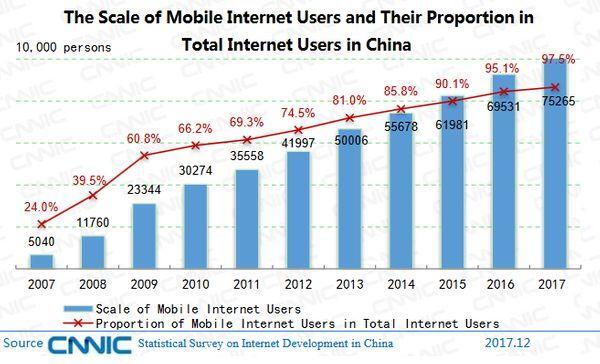

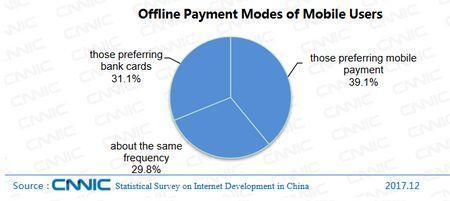

- As of December 2017, the CNNIC Statistical Survey on Internet Development in China offers an eye-catching summary of the ubiquitous mobile Internet, the growing on-line retail sales and the impressive share of mobile payments in off-line transactions

- As a percentage of total Chinese population (1.386 billion in 2017), mobile Internet users are 55% (753 billion), which represents almost all of Internet users (97.5%)

- With the giants of e-commerce (Alibaba) and chat (QQQ and WeChat of Tencent) leading the charge,

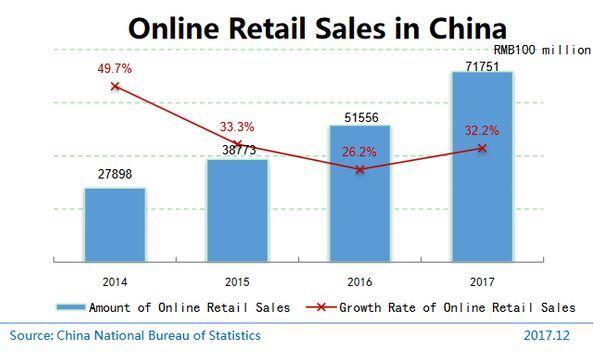

- online retail sales of goods and services in China reached a record high of RMB 7.18 trillion (approx. USD 1 trillion) in 2017, an annual increase of 32.2%. Total retail sales of consumer goods was RMB 36 626.2 billion (approx. USD 5.1 trillion) , up 10.2% over 2016 (National Bureau of Statistics)

- online retail was close to 20% of total retail in China in 2017 - in the US, e-commerce accounted for 9% of total retail in 2017, according to Statista, and is projected to reach 13.7% in 2021

-

- Online retail sales of physical goods reached RMB 5.48 trillion (approx. USD 765 billion), an increase of 28.0%, accounting for 15.0% of the total retail sales of consumer goods (up 2.4 % over 2016)

- Online retail sales of physical goods reached RMB 5.48 trillion (approx. USD 765 billion), an increase of 28.0%, accounting for 15.0% of the total retail sales of consumer goods (up 2.4 % over 2016)

- Off-line payment habits make penetration of the mobile Internet in China all the more remarkable

- Alibaba and Tencent together control approx. 92% of third party payments; keen to maintain their grip on the data trove of consumer consumption profiles, both companies are extending their Alipay and WeChat services to off-line merchandising

- The strategy proves to be successful in scaling traditional services (food delivery, ride hailing) by an order of magnitude and by penetrating retail shopping, including the straight acquisition of chains

- Statistical evidence bears this out with an impressive 39% mobile payment preference and only 31% still attached to bank cards and cash in off-line transactions

In retrospect, as has been widely commented, the explosive growth of financial services in China was almost pre-ordained

- The large Chinese banks, such as ICBC, China Construction Bank

, Agriculture Bank of China and Bank of China, have been serving the needs of large business and infrastructure but hardly met the expectations of the medium & small industries, waking up belatedly to the competitive challenge - Sensing an opportunity, Internet firms have been rolling out an ever-expanding array of features, providing more and more data and deeper knowledge of user profiles beyond the core businesses of e-commerce and enterainment

- The 'ecosystem' created by the Internet giants is a self-feeding stream of continuously refined and updated information on the Chinese consumer and on the small and middle businesses active on Alibaba's Taobao platform

To Chinese regulators, the expanding Internet data empires are both a challenge and an opportunity

- The challenge resides in the growing ability of Alibaba, Tencent and possibly Baidu, to compete with the banking system on its own turf with refined credit scoring, informed - and swift - lending procedures, attractive monetary funds, insurance and wealth management, putting the costly infrastructure of traditional banking at risk

- The opportunity is to further market penetration beyond the urban middle class and into the South-Asia region, targets shared by the firms and the regulator

Rural areas, a new frontier

In an balancing act, we believe that the Chinese regulator will continue to fine-tune the financial requirements imposed on Internet finance

- with measures protective of savers, proved to be indispensable, for instance, to reign in the abuse of the early P2P years

- but also rules providing the Internet firms with the leeway to secure an denser coverage, directed towards the rural, also much poorer, areas

Lagging in the adoption of mobile communications, thesel areas are at a great economic disavantage and their lack of progress will be concentrating the minds of the Chinese authorities

The structural imbalance between the urban network and the impoverished, underserved provinces, encouraged massive labor transfers over the past 30 years

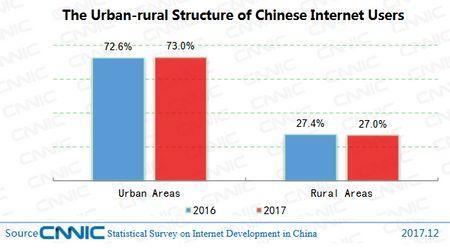

But there is little doubt that the still sizable rural population - 42% of total population in 2017, compared to 82% in 1980 according to the World Bank - is holding the country back

Because access to mobile communications has been a catalyst across consumer retail, access of small business to new markets and credit facilities for both business and consumer, the poor adoption rate in rural areas (27% and falling) signals deep fractures and absence of the social harmony pursued by the authorities

As we will argue in follow-up reports, the dominant positions acquired in often overlapping market segments by the leading companies will benefit from the enhanced regulatory scrutiny

But their expansion will be likely to shadow the priorities of the Chinese authorities, in an effort to favor rural development and to strengthen Chinese inflluence in South-East Asia

Capital expenditures may weigh quite heavily in these ventures over the medium term, well beyond current estimates of the investment community