GE Oil & Gas – full steam ahead

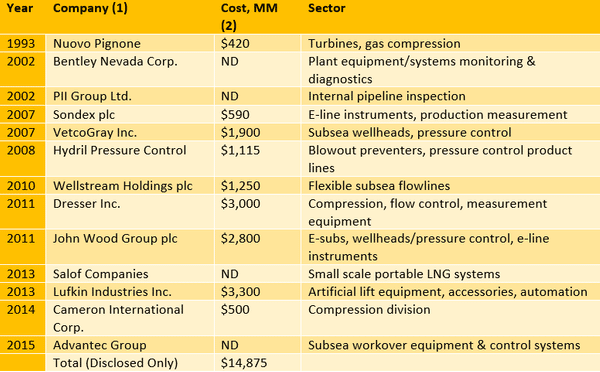

GE began buying companies supporting oil and gas development, transportation or processing in 1993 with Nuovo Pignone but mainly from 2002 on, investing close to $15bn in disclosed deals , 4 deals remaining undisclosed

Questioned in the past, the strategy may still tell what the future holds in store

Sce oilprice.com D.Yager 2016

Initial focus on turbines and gas compression (Nuovo Pignone) offered multiple market opportunities, possibly as part of, or in combination with, GE’s power division and this opportunity may well have been further explored with acquisitions of Dresser (2011 - $3bn) and Cameron compression (2014 – $0.5bn)

But the shift towards highly specialized oil field equipment was clearly under way from 2002 on, with acquisition of internal pipeline inspection (PII Group), subsea wellheads (VetcoGray) or artificial lift equipment (Lufkin)

We are not qualified to estimate the value combined offers of oil field equipment might have created in cross-selling efforts or could potentially create

The possibility certainly exists but, unless the equipment under consideration is uniquely recognized (such as Lufkin lifts), competition from niche specialists may have limited the scope of this strategy

Accordingly, our assumption that the acquired equipment specialists have pursued their industrial activity fairly autonomously under GE, certainly on the technical level and to some extent in separate sales forces, is not unreasonable

Even so, GE’s expansion in oil service equipment has been implemented over the vast, and prolonged, upswing of the up-stream oil service industry since the early 2000’s, which could only comfort management decisions

But, although rear mirror judgments are a dime a dozen, we will question

- the costly build-up of a full oil service ‘catalogue’, putting very low-tech oil exploration and extraction equipment next to sophisticated technologies

- the commitment made by GE to an industry known for its cyclical – capital hungry – trends

We believe the issue is relevant in context of the Baker Hughes partnership and subsequent spin-off

Baker Hughes and GE – on and off

Announced in October ’16 and finalized in July ’17, the BHGE partnership came about in the wake of the down-sizing of GE Capital from 2014-2015 and combined oilfield service company Baker Hughes with GE oil equipment division

As GE Capital had been the engine securing low cost AAA debt financing for its cyclical industrial activities, the partnership could potentially access other venues of credit, an option not be ignored in a context of rising rates

As it turns out – this option will now be exercised in the coming years after the June ’18 announcement of the spin-off of oil services from General Electric

The management decision has been long in the making and reluctantly adopted, reversing a Feb’ 18 announcement BHGE was not to be sold in the short term…

Without being privy to internal discussions, we believe the loose fit of some of the downstream equipment activities with Baker Hughes services and their possibly close and mutually supportive relation with GE Power (the most important division remaining in ‘new’ GE) must have been a central issue

If correct, this assumption puts the onus on Turbomachinery & Process Solutions (TPS), the segment which according to BHGE (Form 10-K year 2017)

“provides equipment and related services for mechanical-drive, compression and power-generation applications across the oil and gas industry as well as products and services to serve the downstream segments of the industry including refining, petrochemical, distributed gas, flow and process control and other industrial applications.”

TPS is also at the heart of BHGE operational income – contributing in 2017 an estimate 60% of income with 30% of total revenue (our assumption is that total pre-partnership revenue and income of Baker Hughes can be assigned to Oil Services, as discussed here)

To further highlight the singular rapport of TPS to BHGE oil services, we take note of the main competitors identified in the segment – not a single one of which belongs to the oil field services industry

In upstream and midstream applications, our primary equipment competitors include Siemens (Power and Gas business unit), Solar (a Caterpillar company), MAN Turbo and Mitsubishi Heavy Industries. In downstream applications, TPS primarily competes with OEMs and independent service providers, including Flowserve, Pentair, Emerson, Siemens, Hitachi, Solar (a Caterpillar company), Ariel, MAN Turbo, Burckhardt, Elliott Ebara and Mitsubishi Heavy Industries. Our aftermarket equipment product line competes with smaller independent local providers such as Masaood John Brown, Sulzer, MTU, Trans Canada Turbine, Chromalloy and Ethos Energy (a joint venture of Siemens and the Wood Group)

Source Form 10-K page 7/173

Competing with the major players in industrial equipment manufacturing, TPS is central to the conundrum which GE management had to confront

- either keep BHGE as part of the conglomerate, with the opportunity to make a strong statement downstream backed by GE Power and TPS expertise – a medium term strategy

- or admit to immediate financial constraints and rebalance the debt load – perceived as a short term urgency

A choice has been made but – because the spinoff of BHGE is caught in a network of legal obligations – its practical consequences remain to be seen