There may be light at the end of the tunnel with vaccine roll-out in much of the developed world (developing countries are another matter) but, if the cloud of Covid-19 is lifting, it is far from projecting a balanced patch-up globally

Major economies are lagging as new waves of virus disrupt their plans – foremost the U.S. and the European countries – while new infections rates in Asia breed uncertainty

International trade flows remain valuable indicators of the actual momentum in the world’s major economies to get back on pre-Covid growth tracks

- unbalanced since the early ‘90’s, the U.S. goods and services trade deficit is plunging again and looks markedly unhinged since the second quarter ’20

- the constituents of U.S. imports (consumer goods - up) and of exports (industrial goods - down) are impacted in ways which will not adjust before some years (not months)

- rising monthly trade deficits of the U.S. balance of trade with Asian countries are exacerbated by currency manipulations aimed at boosting their export-driven economies

Feeding a confrontation with growing Asian economies, and not only with China, these tensions are hardly reassuring as unemployment and poverty are at critical heights, and as countries, highly leverage firms and households, all reach record debt level

Insolvencies and distressed households will scar developed economies worldwide for much longer than the virus itself, slowing recovery as the credit crunch bites and making the ‘return-to-normal’ rather more uncertain

Rising popular discontent will stress the geopolitical playbook, stifling global trade in ways yet unknown

U.S. goods and services trade in a vise

A bugbear of the current U.S. Administration

The balance on current accounts includes

- the net balance of trade for goods and services

- income (such as dividends or earnings on foreign direct investments) in (received) and out (allocated) of the country

- current unilateral transfers (defined as allocations with no counterparty in return)

However, the deficit in goods and services is a qualified indicator of how China became the global manufacturing center – with Asian countries following suit

Because the balance of trade is linked to the job opportunities in manufacturing and in services, the deficit recorded with one country (name China...), and with the world, is a tried and true political target

Sharp increases in the deficit will inevitably stir popular discontent early on and become even more critical, when the new imbalance appears to be structurally resistant to speedy correction

More and more monthly U.S. trade deficits

The deterioration of the U.S. balance of trade, since the pandemic gripped the world economies, is striking, sliding from February (-$37billion) to October (-$ 63.1billion)

| U.S. Trade Balance Goods and Services 2019/2020 | ||||

| in $ billion | U.S. deficit | % GDP | with China | in % of total |

|---|---|---|---|---|

| 2019 | 616,8 | 2,90% | ||

| Q1-20 | 111,5 | 2,10% | 53,9 | 48% |

| Q2-20 | 170,5 | 3,50% | 77,8 | 46% |

| July 20 | 63,6 | 31,6 | 50% | |

| Aug. 20 | 83,1 | 29,8 | 36% | |

| Sept.20 | 63,9 | 29,7 | 46% | |

| Oct. 20 | 63,1 | 30,1 | 48% | |

| Q3-20 est. | 210,6 | |||

| 10m.2020 | 555,7 | |||

| sce - US Bureau of Economic Analysis | ||||

| sce - US Census Bureau | ||||

| sce - Gen.Admin.Customs-PRC | ||||

The sharp upward trend of the U.S. deficit in trade reflects both

- an increase in imports of foreign (often Chinese) consumer goods, medical supplies, personal computers and smartphones

- while exports of manufactured products (machinery, industrial components, aircrafts and parts) are hit by a worldwide downturn

A skew which may be lasting...

Our Q3 estimate of a $210.6 billion deficit is not encouraging (close to twice Q1 deficit) and 2020 is on track to become a banner year for importers, contributing to a rising deficit of which China represents 46%

With a focus on the trade of goods only (not services), some unusual trading partners show up, such as Switzerland and Ireland...

10-months U.S. trade deficits in goods with major countries in $bn and as % of U.S. goods deficit in Total Trade 'All Countries' over the same period (estimated at $736.2 billion by the U.S. Census Bureau)

| in billion $ - 10months '20 | U.S. Trade Deficit | % of U.S. Deficit | Rank as Importer |

|---|---|---|---|

| China | 252,9 | 34.3% | 1 |

| Mexico | 92,2 | 12.5% | 2 |

| Vietnam | 56,6 | 7.7% | 7 |

| Switzerland | 51,1 | 6.9% | 6 |

| Germany | 46,2 | 6.3% | 5 |

| Ireland | 46,1 | 6.3% | 9 |

| Japan | 42,8 | 5.8% | 4 |

| Canada | 11,6 | 1.6% | 3 |

| sce - US Census Bureau | |||

Currency manipulators ?

As it turns out, U.S. trade with Switzerland is indeed spectacularly out of balance, with twice the 2019 deficit ($26.7bn) in 10-months 2020 ($51bn) on the strength of pharmaceutical and organic chemicals exports to the U.S.

Even though the Swiss Services trade balance is strongly in favor of the U.S., led by intellectual property (industrial processes) and professional and management services, the U.S. Treasury did not hold back on Dec. 16, 2020 in pairing Switzerland with Vietnam, an up-and-coming emerging market, as 'currency manipulators'

The tresholds on which the Treasury relies have all been reached by Switzerland in 2020 : a $20 billion-plus bilateral trade surplus with the United States, foreign currency intervention exceeding 2% of GDP and a global current account surplus exceeding 2% of GDP

It fact, Swiss currency intervention is not trade-driven, but an effort to keep the run on the Swiss Franc, reputed a safe-haven,in check - and the label attached by America's Treasury cannot be expected to pressure the Swiss

Currency manipulation by America's Asian trading partners are another matter entirely, not only for Vietnam, but also for Taiwan, Singapore, Malaysia and Thailand, raising sticky geopolitical issues...

Malaysia, 14th importer and Taiwan, ranking 10th, add respectively a further $25.3 billion (5%) and $24.1 billion (4%) to the U.S. deficit

Asia on the doorstep

Asian countries together - including Thailand, India and South Korea contributing around $20 billion each - account for a U.S. deficit in goods of $462.2 billion - 62% of America's trade deficit in goods as of Oct. '20

U.S. focus on China could become obsessive - as another 7 Asian countries weighing about as much as China, and on track to grow much faster, are taking center stage

In the short term, the incoming Administration is bound to follow in the footsteps of the current US Trade Representative, Mr. Lighthizer, leveraging the tax regime implemented under President Trump to make sure negotiated Chinese committments are honored (they are not as of this writing) and possibly taking another run at intellectual property protection and access to the Chinese market

While putting renewed emphasis on Democratic priorities, increasing protections for workers, mitigating climate change and raising standards for consumer protections, the rise of Vietnam, Malaysia or Thailand might require some deft footwork to balance U.S. geopolitical influence in South East Asia - a critical priority in its own right - with a check on the most egregious export policies

'Benign neglect' under many guises made China's quick rise in the ranks possible but, to avoid repeating past mistakes, clarity about what is - and what is not - acceptable to access the American marketplace seems preferable to vain attempts to dictate corrective rules after the fact, when the horse has bolted...

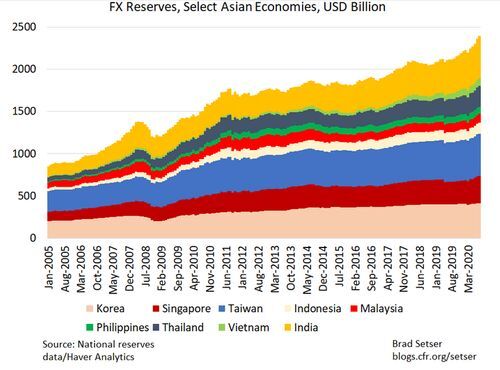

Leaning against the wind

Strong fundamentals, a steady flow of foreign investments rebalancing manufacturing facilities across Asia and weak domestic consumer demand for foreign goods ready the Asian economies for a replay of the first decade of this century (from 2003 on) - with sturdy currency manipulation

Highlighted by analyst Brad Setser, of the Council on Foreign Relations, these currencies should be on the rise as trade surpluses contribute to the accumulation of foreign currency reserves

And the reserves have been rising since 2019 - even after setting aside India which has no current account surplus

As discussed by Mr. Setser, the currencies have not risen in tune and the reserves appear in fact to be lagging the trade surpluses' upward march

The transfer of foreign reserves to State banks, pension funds or investment funds - creating pools of foreing currency in a familiar playbook - stabilizes official reserves posted at the central bank and obscures intervention

As Mr Setser concludes :

Add all this up and a substantial number of Asian countries with relatively large trade and current account surpluses are now adding to their disclosed—and in some cases hidden—reserves in order to keep their exports competitive at a time when many Asian economies are outperforming the global economy

Mercantilist monetary policies are probably as actively pursued by China when trade surpluses are running at $385 billion (Jan.-Oct. '20 Chinese statistics) and rising - on top of which foreign investments in the domestic bond market are expected to add $200 billion on an annual basis (Setser estimate)

And, all the while, central bank reserves have not moved significantly...

... making currency manipulation another favorite topic that the new Administration cannot leave alone

Offsetting conflicted priorities

In absolute terms, the pull of domestic economic policies favoring relocation of manufacturing hubs at home lays out the tangled contradictions with the geopolitical priorities of America in South East Asia

And the dynamics of the irreconcilable goals pursued by the U.S. on the domestic and foreign fronts are set to clash before long

- for all the bluster, China can be expected to manage its surplus on the U.S. market conservatively, keeping its 'share' of the deficit in % and possibly in value but neighboring countries are riding the swelling wave of 'not- made-in-China' exports

- with economic policies aimed at creating local job opportunities and following the Chinese playbook (of which currency manipulation is a frontrunning tactic), Asian countries will undoubtedly be a major factor of increasing U.S. trade deficits

- U.S. aid packages protecting distressed households as well as benefits and grants forestalling insolvencies have had the unwelcome consequence of powering the demand for imported consumer goods - if the skew favoring such goods in import statistics are any guide - a development which has to be kept in check...

- if U.S. foreign policy remains focused on the Pacific, as is most likely, constraints grow worse because they raise the specter of renewed efforts to conclude a Trans-Pacific Trade Agreement, indispensable to counter recent regional initiatives, with and around China, and forcefully opposed from a vocal bipartisan isolationist base

Deep contradictions between goals on the domestic front and in foreign affairs strengthen the case for marginal adjustments of the issues - hardly an exciting reversal of policies led by the current Administration, but probably realistic....?