The sizable imports of semi-conductors, exceeding China's oil demand, and depriving its own exporters of much potential value added, suffice to concentrate the minds of governmental planners

And the country's aerospace, robotics and military build-up will undoubtedly be pushing the production of semi-conductors to the very top of strategic priorities

With 2 companies, affiliated with Huawei and Tsinghua Unigroup, in the ranks of the largest 'fabless' companies worldwide for Integrated Circuits design, China can vaunt remarkable success

But the focus on the production of the semiconductors themselves has become more intense since the 2010's - and strategic plans published from 2014 on have locked the State, the local governments and the largest private companies in close partnerships

Booking partial success in 3D NAND production roll-out (2018/2019), it remains to be seen if China's very ambitious goals of self-sufficiency by 2025 can be achived in DRAM memories and in Logic semi-conductors

Technological challenges will be surmounted, giving it time, but geopolitical confrontations remain a wild card

According to estimates from Bernstein Research, quoted by SCMP, China imports some US$260 billion worth of semi-conductors in 2017 (from $200 billion in 2013) - the heart of its vast electronic export machine (of more than 90 per cent of the world’s smartphones, 65 per cent of personal computers and 67 per cent of smart televisions)

Famously insistent on ‘Made in China’ goals, seen as a token of independence and as a symbol of a resurgent China, governmental planning has, unsurprisingly, taken a dim view of the reliance on foreign imports for these essential components

Official initiatives for Integrated Circuits may over time book the expected results of manufacturing autonomy

But the road ahead is tortuous, strewn with complex issues blending Intellectual Property rights, unrelenting technological advance and manufacturing know-how, and political power play

Integrated Circuits (IC) - The Plan(s) and the Big Fund

The June 2014 “Guideline to Promote National IC Industry Development” is a framework to support the supply chain, by growing Chinese semiconductor industry revenue from $57.5 billion in 2015 (¥350 billion) to $143 billion by 2020 (¥870 billion) at a 20% CAGR

- Integrated circuits (with a domestic production of $13.4 billion in 2015) were presumably paid special attention because of its growth potential and China's slow start in the field

In 2015, the all-encompassing “Made in China 2025” strategy increased goals for domestic IC production from less than 20% in 2015, to 40% in 2020, and 70% by 2025 (source IC Insights)

- These targets - if they prove to be exact - made up in political intent (and support) what they lacked in feasability. In 2015, Chinese IC producton was just 13% of total market

- Projections by IC Insights set a more probable range between 15% (2020) and 20% (2022) of market demand

- At an est. $33.6 billion in 2022, China's production would contribute slightly more than 7% to the world total - and even outstanding growth would still take in less than a 10% share

The 13th Five Year Plan (2016-2020) posits adding value to the manufacturing of high-tech products by reducing the reliance on imported key parts, components and manufacturing equipment

Funding has been allocated on a large scale to the IC supply chain over the years, by the State and State-owned enterprises (SOEs), supplemented by local and regional entities, and engaging the largest private tech firms more recently

- the National IC Fund or ‘Big Fund’ is the Chinese government’s primary vehicle to develop the domestic semiconductor supply chain

- the original (2014) funding round of ¥138 billion ($21.8 billion) included the Ministry of Finance (36.74%), China Development Bank Capital (22.29%), China Tobacco (11.14%) according to a filing by Shenzhen-listed Nantong Tongfu Microelectronics (February ’18)

- Local municipalities - as was the case early on for Beijing, Hefei, Shanghai, Wuhan, and Xiamen - and private equity firms pledged a further $100 billion at the time

- in April ’18, a 120 billion yuan ($18.98 billion) investment round for a second fund to support the domestic chip sector was under consideration and the trade tensions and the ZTE ban (announced in April by the US government and withdrawn in June) contributed undoubtedly to accelerate investment in the sector

- And today, the tech giants, Alibaba, Baidu and Huawei, have all committed to research and production of chips

What the range of funding entities suggests - and what a 'Silicon Valley chip veteran' confirms, is that

- In China, the central government is the strategic passive money. It’s almost like a matching grant. Some oversight but pretty much uninvolved and un-participating in profits. There is one requirement, local government and private industry must provide more than 50% of funding

The IC plan may be massive, ambitious and farsighted, but rivalries among local regional governments and cities have fired a race to attract the largest investment and the dominant moat in the industry, a recipe for dispersion and not necessarily a factor for success

The Chinese strategy still exudes the confidence in a winning combination of vast cash allocations and audacious experiments, taking on the entire supply chain of integrated circuits manufacturing

Relying on a strong domestic network of innovative product development and design, the Chinese authorities are expected to boost local semi-conductor demand for products that will then be considered Chinese in origin because of their China-manfactured constituents

A tall order, all things considered, but the approach must sound familiar

The car- and car parts industry early on and, more recently, the battery production have been planned in similar fashion – as coherent industrial policies, willfully executed by meshing State subsidies, local government initiatives and private ventures

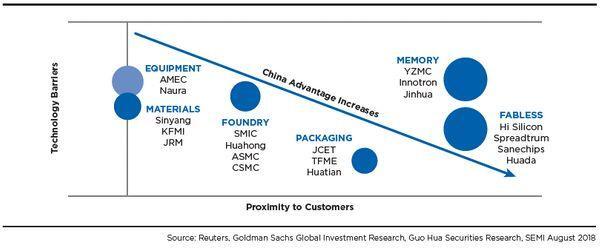

The Integrated Circuits supply chain - design and fabs

IC design

With revenues of $31.9 billion generated by close to 1 400 companies in 2017, China’s IC design ranks third in global rankings

The production by these ‘fabless’ design houses targets defense, telecommunications and finance, but also the wide range of consumer goods

With a few exceptions, these companies remain small with revenues under $1 million

Uniquely, HiSilicon (wholly owned by Huawei) and UNISOC (ex-Spreadtrum, a core subsidiary of Tsinghua Unigroup), China’s two largest domestic IC design companies, rank in the global top 10 of fabless companies, and are making notable progress in communications and application processors (mobile industry and data centers)

The close proximity of China’s fabless companies to the region’s electronic systems makers is a key advantage for their competitiveness and a decisive factor in the financial viability of the numerous small firms

Low margin consumer applications have offered the opportunity to broaden the expertise of the IC workforce incrementally, by framing the complexity of the device makers' demands stepwise

Instead of controlling the manufacturing process of the chips, as international fabless companies do (COT model), China’s IC design industry has relied on partnering with international fabless companies to acquire advanced technologies and intellectual property

Fabs

A 'fab' is a foundry, fabricating the chips designed by the firm itself or by 'fabless' semiconductor firms

As of late 2018, 25 new fabs (both domestic and multinational) were under construction in China, with 10 of those projects being 300mm plants, according to SEMI

Producing for both local and multinational customers, China’s IC foundries include international firms (Taiwanese TSMC and UMC, and US based GlobalFoundries) and domestic players

As noted by McKinsey (2015), if Chinese manufacturers were to hit the 2025 self-sufficiency goals the government has laid out for this segment, roughly all incremental foundry capacity installed globally over the next ten years would have to be in China

With a 10% market share in 2014, and a total addressable market (probably under-estimated) at $78 billion, in 2015, China aimed at growing its share to 28% (2020) and to 46% (2025)

Projections are only indicative but the drift is unmistakable with a production share of 13.3% at a standstil in 2017 and an est. 16.7% in 2022

Chinese industrial planning will need to straddle so many contradictions as to prove doubtful, if not unworkable

Going forward, the semi-conductor industry – in fact, the entire electronics ecosystem relying on ICs, involving Chinese as well as international device manufacturers – requires a roadmap to navigate the minefield of geopolitics

The issue is central to any future negotiation because ICs are the core of technological advance, defining our future way of life and our very security, as we will discuss in Silicon Hearts, our follow-up note