In medical robotics, it is all about Intuitive Surgical

Stock performance clearly does not rejoin with our analysis favoring the companies with dominant market shares in the medical device industry - Medtronic, Johnson & Johnson, Stryker, Abbott and Smith & Nephew

With a focus on growth potential over the next 3 to 5 years, these companies enjoy unparalleled distribution networks and relationships, strong in-house technical expertise buttressed by specialized partnerships and potential extension in data management (data flows, AI, machine learning). These strengths were – and remain – our ‘great expectations’

However, as the unremitting progress of Intuitive Surgical demonstrates, other factors dominate investor perception for now

A textbook case

Since 1999, date of its market entry, Intuitive Surgical has been in a unique position to build an impressive moat in a number of surgical specialties with a keen focus on obtaining and maintaining patent, copyright, and trade secret protection

As of the first quarter 2018, 4 666 systems installed around the world (3 010 in the US and 1 656 outside the US) are effectively platforms generating various additional revenue streams

- annual service contracts for the equipment

- instrument and accessory revenue, related to the volume of procedures

- training programs for the surgeons

The number of patents held by the company (2 750 according to the 2017 annual report and 1 900 filed in the US and in foreign jurisdictions), may have delayed the launch of competing robotics solutions, and may continue to do so.

The impact of patents expiring in 2019 – noted by analysts – remains uncertain

Anticipating the emergence of competition, Intuitive certainly has not remained inactive, fine-tuning its distribution in the US and overseas and its pricing strategy

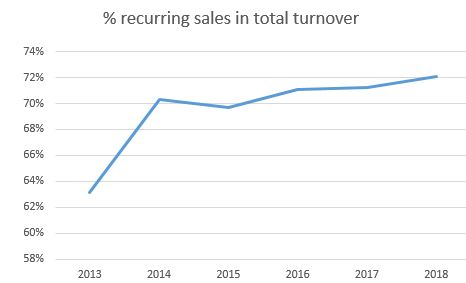

- the weight of the (quite profitable) recurring sales of service contracts and medical instruments in total turnover has notably increased since 2014

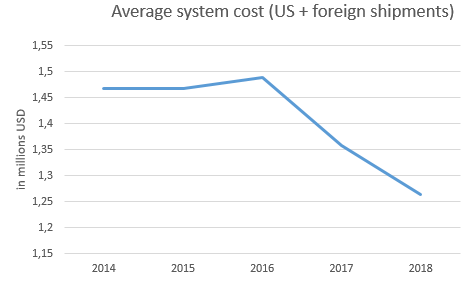

- more aggressive pricing, especially in the US where the market may approach saturation, has boosted the placement of new robots markedly since 2017

Mixing top-of-the-range Xi units in different configurations with lower prices X models, the average price per unit in the first semester 2018 remains purely indicative and must be interpreted with caution.

However, unless the average price on the US market in the first semester 2018 is an outlier, the intent to step up the pace of adoption of the da Vinci robots in America, preferably with the higher end Xi models (84% of the units shipped) can be taken for granted

| Average price / systems (in millions USD) | US Revenue (systems) | Total Revenue (systems) | US share in Total Revenue (systems) | Operating Income Margin(*) | |

| 2016 | 1,48 | 501,3 | 800 | 63% | 35,10% |

| 2017 | 1,45 | 603,5 | 928,4 | 65% | 33,90% |

|

2018 6months |

1,18 | 296,4 | 511,9 | 58% | 31,50% |

(*) Systems refer to the robots shipped by Intuitive Surgical and not to the recurring sales of instruments and services. The margin on operating income is based on the condensed statement of all operations; the company does not report on segment profitability

Reinforcing a position of strength – pricing, product development and China

The pricing strategy, as we understand it, is adjusted to market conditions in- and outside the US

In the US, and possibly some other markets with advanced health care organizations, equipping the hospitals as completely as possible with Intuitive’s surgical robots is assumed to be a priority to crowd out potential upcoming competitors

- The lower average price recorded in the first half of 2018 (-18% on 2017) has probably been a factor in maintaining a 20% year-on-year revenue growth and a shipment of 250 robots

- However, additional factors may have been in play, such as a push to equip medical schools with the high-end Xi robots at sharply reduced price, securing the training of surgeons on da Vinci for years to come – we have no way of knowing but the strategy would make sense

Outside the US, average price of the robot line-up has been notably higher than in the US ($1m39 vs $1m18 in 2018) and the uptake of the new, lower priced X series has been higher (28% of the units vs 13% for the US)

- The sale of new robot systems outside the US has also been quite volatile, with middling quarterly growth in 2016 – mid-2017 (in the 60 units/quarter range) and rapid pick-up by Q-4 2017 and in 2018 (155 units in the first semester 2018)

- Local regulations and reimbursement terms by the patients may be factors complicating – and limiting – foreign distribution, as they will remain also for Intutive’s future competition

Product development – R&D has been picking up notably over the past 3 years (+70 % vs + 35% revenue growth), reaching 9.5% of revenue in 2018, as shown on pininvest - Go to : Asset infos ISRG tab Financials - probably related to the development of the lower priced X robot, launched in mid-2017

It will be noted that according to a Statista comparison of R&D spending in 2016 with projections for 2022 for the top 20 medical devices companies, Intuitive was ranked bottom last at the time…

- Focus on a unique market niche may in fact put the company in a competitive position against much larger device companies with diversified research teams – Medtronic with a R&D budget 6 times the size of Intuitive’s has been delaying its entry in medical robotics, probably until 2019

But Ewards Lifescience

While direct comparisons cannot be conclusive, research efforts at Intuitive could in fact be constrained by the uniqueness of the da Vinci flagship, leaving only two options

- Deepening the robot line-up, as the company chose to do by offering lower-priced Xi system with upgrade options of advanced capabilities. The venue seems to be fully explored and no further announcements have been made

- Create a new, distinct product line as the company announced with the on-going research for a flexible catheter (through a patient's mouth and into the lungs by remote control) for early diagnosis and treatment of lung cancer.

With new product lines, Intuitive will be confronted with a competitive landscape and possibly forced into catch-up strategies as will be the case with Auris Heathcare's catheter platform, approved by the FDA in March ’18 (Auris CEO is Frederic Moll, who founded Intuitive Surgical in 1995 and left the company in 2002)

Playing catch-up, and signaling the intense pressure of competition, Intuitive Surgical announced early September '18 that they have submitted a premarket notification to the FDA for a new flexible robotic, assisted catheter-based platform, designed to navigate through very small lung airways to reach peripheral nodules for biopsies

China, which represents 3% to 4% of Intuitive's global procedures as of Q2-2018 (according to RBC Capital Markets), could well become the growth engine of the robotics range as the Intuitive's established markets mature

The creation of a joint venture with Shanghai Fosun Pharmaceutical with total sales of $3.05 billion and a market cap of $14.5 billion (June '18), 60% owned by Intutive and 40% by Fosun has been announced in October 2016,

Committed to the research, manufacture, and sale of robotic-assisted catheter-based platforms, the joint venture could be a watershed moment for Intuitive to penetrate fully the world's largest under-equipped market

Conclusive research (suggested by the September '18 premarket notification to FDA) and strong distribution, both in China (by the JV) and outside the country (by Intuitive) may lead to a deepening partnership consolidating a lead position for Intuitive

The future will tell...

With a trailing PE of 77, the share price of Intuitive Surgical is projecting a continuing growth trajectory while the strong business, established around its robotics platform with recurring revenues the main contributor to global sales (77%), has all the trappings of a value stock

Competition may - or may not - offer the devices stymying Intuitive's advance

This will be the subject of our follow-up note