Die schwarze Null - or black Zero - is a German rallying cry for conservative management of the public purse

A balanced budget, no additional debt and preferably debt down payments, are the guiding principle for responsible German politicians

The budgetary policy is not without Biblical overtones, as the short video (in German) for Land Mecklenburg-Vorpommern makes clear: seven fat years will inevitably be followed by the lean years…

But dire memories of hyperinflation peaking at 4,200 billion German marks to one dollar in November 1923, wiping out the savings of the middle class (and making Adolf Hitler Chancellor in 1933) most probably weigh heavily

Propitiously, the budgetary mantra squares with an economy which became a trading powerhouse by the grace of an undervalued Eurozone currency, allowing the German manufacturing expertise to fire on all cylinders

- With loose central bank policies worldwide, it is not unreasonable to assume that a stand-alone, reinstated, Deutsche Mark would revalue around 40% to the euro, bringing Germany’s industrial house down

But the tremendous success of German exports on world markets is also a poisoned chalice…

The share of exports in the country’s GDP – topping 47% in 2017 – is beyond anything comparable for large industrial countries (France 31% and China 29% in 2017 or USA 12% in 2016)

Chart of German exports of goods and services in % of GDP

source: tradingeconomics.com

Being quite dependent on the common Euro currency, Germany’s economic performance ends up ever more tied to its major exports markets, within Euroland and beyond …

- Approx. 2/3 of exports are destined for Europe - reflecting the powerful draw of German industrial machinery and cars but also deeply integrated supply chains with countries such as the Netherlands (6.8% of German GDP), Austria (4.9%), Poland (4.7%) or Switzerland (4.4%) in 2018, for ultimate destinations in the Far East or the Americas…

- In this skewed count (ignoring exports from the countries affiliated in these supply chains), Asia represents 18% of GDP (China is 6.8%) and the Americas 12% (the US is 8.8%)

The reliance on global export markets is compounded for German industry leaders, and especially for the automotive industry, by their local manufacturing units, mainly in the US and China

- Deeply engaged in China, Volkswagen sells 40% of its total output in China, while Daimler and BMW export 30% of their domestic production to the country

As third largest exporting country in the world (at USD 1.45 trillion) behind China (USD 2.2 trillion) and the US (USD 1.55 trillion), Germany is critically exposed to the vagaries of international trade

The Spring 2019 forecast by the Munich-based Ifo Institute, published on March 14, 2019, reflects the awkwardness of Germany’s economic policies, shouldering international trends from a position of weakness

Trending down from Q2-2018 (second line), the projections for 2019 ‘assume’ some Q1 (and eventually Q2) weakness before returning to normal

Key assumptions have to come true, simultaneously

- the Chinese economy returns to form (following a trade agreement with the US)

- looming trade negotiations with the US have no significant impact on German industry

- the costs to the automotive industry of environmental regulations are accounted for

Leaving aside the risk of a disorderly Brexit (the UK is the fourth largest export market – 6.6% of GDP and USD 95 billion, almost on par with China) and further uncertainty in Italy (exports: 5.1% of GDP), the assumptions might remain a significant drag on growth throughout 2019

- the sharp drop in the trade surplus from Nov. (€ 20.4 billion) in Dec. ’18 and projected in Jan. ’19 (€ 14.5 billion on average) could signal worse to come

Chart in € (millions)

source: tradingeconomics.com

As of March ’19, we suggest that weak growth (if any) spilling into Q3-2019 should at least be considered a workable proposition because none of the issues raised here will be resolved easily and in a matter of weeks

The most obvious consequence of 4 weak quarters (Q4-2018 to Q3-2019), putting potentially Germany in recession, would be the need to boost domestic demand, responding to both Eurozone and international (US) pressure

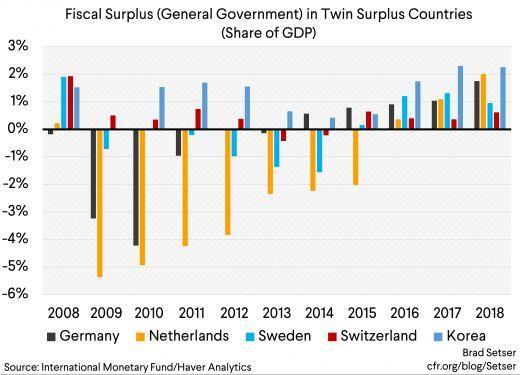

For the world’s twin surplus countries (countries with both a fiscal surplus and a current account surplus), more support for their own growth is a given

Of Germany, with the world’s largest trade surplus (close to USD 300 billion), double China’s surplus of USD 160 billion, nothing less can be expected – the schwarze Null has to go…

Germany is likely to recognize that economic uncertainties may prevail, calling for support to global growth

- the inconsistency between the benefits of an aggressively priced currency - the euro - and a straight-laced budgetary constraints may never be fully resolved and do not need to be

- for years to come, the aging German demography will continue to induce more exports than domestic demand

Flexibility is needed

The implication – especially for the German bond market – will be discussed in a follow-up report