Pin-insights

From a Russian perspective, the end of 2019 has been rewarding

Belated attempts by the US to block the new pipeline to Germany and Europe - Nord Stream 2 - will delay but not stop this major infrastructure project, an agreement has been found with Ukraine for gas transit to Europe and a pipeline serving China will come on stream progressively over the next 24 months (as new gas fields are being developed)

However, the emergence of a new gas major, the US by way of shale production, and of new markets, in China and more broadly across South Asia, boosts transport of liquid natural gas (LNG), a requirement for the exporters to serve new markets in Asia

Two factors stand out

Delivery of LNG circumvents the hold Russia's Gazprom pipelines had on its key market, which is Europe where flexibiltiy and wider choice will lead to supply diversification

Versatility of LNG delivery points will - to some extent - deprive the traditional gas providers of their pricing power over individual countries by integrating an international gas market spot price

Under pressure to master the technology and to finance the new investments, Gazprom has its work cut out

***

Natural gas, as an energy resource, is bountiful and expected to meet human needs for decades as new gas fields come on line

It is also fast becoming the domain where the competing commercial interests of the world's largest gas providers overlap and mix awkwardly with their geopolical interests

An unstable equilibrium

America, a newly minted major gas exporter, keen to gain global market share where its energy industry had none, is bound to clash with Russia, the legacy gas provider to the European markets, the world's largest importers for now

To further complicate the puzzle, the rise of US gas export ambitions materializes as energy demand in China takes flight - with developing Asian countries following suit

Economic interests, geopolitics and keen efforts of all parties to diversify their client base (for exporters) and their energy sources (for importers) are the fragments of an unstable equilibrium

Russia, the most powerful gas provider in Europe, secure until recently in its vast network of gas pipelines, has been preparing for the challenge to its market positions

However, caught in a vise, between technological challenges of LNG (liquid natural gas) delivery, considerable investments of serving a more diversified client base and geopolitical uncertainties, Russia remains the game changer

Against the background of predictable strategies of its competitors (mainly the US) and its clients (Europe and China), success or failure of Russian energy policy will be the variable of interest

Doing well, for now

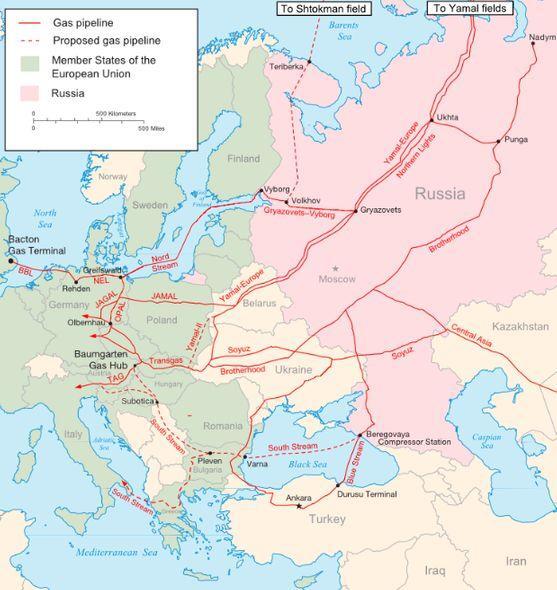

The recent, and belated, American efforts to stall the construction of Nord Stream 2, the gas pipeline under the Baltic Sea, appear to fall short of a strategic vision putting energy at the center of broad security considerations, as shown in ‘Russia’s Rattenfänger’

Strategic thinking however will not go away because of the importance of energy exports for the Russian federal budget and for its export earnings

According to russiamatters.org, a Harvard Kennedy School blog, energy has accounted for 62 to 64 % of Russia’s export earnings in 2015-2018; oil and gas—Russia’s most lucrative energy exports—provided under 50 percent of its federal budget revenue in 2015-2017 and for most of 2018, although they did account for just over 50 percent in January-February 2018. (Fact-check done in July 2018)

From a Russian perspective, which this note will be outlining, the end of 2019 has been rewarding

Looking westward, towards Europe, Gazprom

Nord Stream 2 with a yearly capacity of 50 bcm (billion cubic meter) is expected to add 20% in capacity to record 2018 Russian exports of 251 bcm

The American effort to block the project at a very late stage (some 100 kms piping remain to be laid out of 1250), arguing on behalf of European security interests and Ukrainian gas transit rights, is losing the argument following the last minute contractual agreement signed in late December '19 between Ukraine and Gazprom on transit fees over the existing pipelines

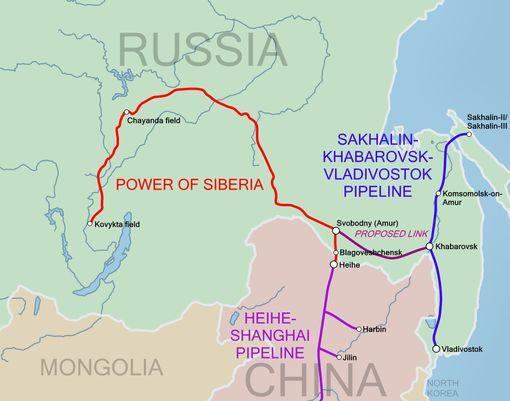

Looking eastward, towards China, a new pipeline, flatteringly named ‘Power of Siberia’, has been put in service in December ’19 by Gazprom

These developments are satisfactory but, in the context of the global gas markets, it will be recognized that the achievements also belong to yesterday’s energy industry

Even if Russia attains essential goals on the global gas markets with its true-and-trusted expertise of laying pipelines, its energy sector has only reached some intermediate stage with nimbleness and has to prepare for the long slog

Of course, the disruption of new market conditions does not catch the Russian planners unaware

Coordinated response on a global scale is another matter...

It is a gas...

It wasn’t until the 20th century that the word “gas” took on the sense of “enjoyment, amusement, fun” in Irish English - source

During the past decade, the gas market has no so much evolved as been turned upside down by two new players

The U.S. veered almost overnight from gas importer to one of the world’s largest exporters, thanks to shale exploration, adding close to 200 billion cubic metres in production by 2025, of which more than half is expected to be exported as liquified natural gas (LNG)

According to IEA estimates, North America could represent between 25% and 30% of gas export growth in the world market and produce more gas than the entire Middle East to 2040

China, almost entirely absent as gas importer in 2008, is becoming the major import market impacting – directly or indirectly all the gas-rich exporters with capacity to spare (Qatar, Russia and today the US)

The massive expansion in China’s gas consumption, which increased by 33% in 2017 and 2018, is the reason for the growth in the global LNG balance, according to IEA

In its "Gas 2019" report dated June '19, the IEA projected that China's gas consumption would rise from 280.3 bcm in 2018 to 392 bcm in 2022 and 450 bcm in 2024

Further developments are projected beyond 2025, with emerging new gas producers (Mozambique and Iran) and growing demand in South East Asia, all of which are already in planning stages given the time frame and the magnitude of the investments

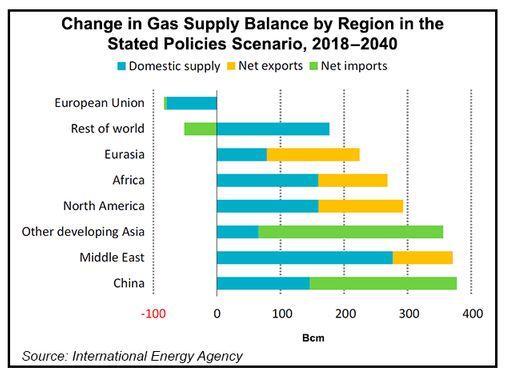

The 2018-2040 growth trends are highlighted by the World Energy Outlook 2019 of International Energy Agency (IEA), issued in Nov.

The IEA's 'Stated Policies' scenario - which incorporates current governmental policy intentions and targets in addition to existing measures - pictures the transformations vividly, as measured in billion cubic metres per year (bcm)

The three exporters, marked in yellow, stand out - Russia (and Central Asia) with an expected increase of approx. 150 bcm, the US with 130 bcm (from 0) and the Middle East (Quatar and potentially Iran) with 100 bcm

Africa is seen as a possible fourth exporter adding to growth at a later stage, from Mozambique offshore gas discoveries – with another 115 bcm

Marked in green, the import markets seen as most likely to absorb this tidal wave of gas on the world markets are concentrated in Asia, China with 250 bcm and a possible 300 bcm in ‘developing Asia’

Europe is expected, according to the IEA, to roll back its domestic consumption by 2040 (marked in blue), as renewable sources of energy take hold - a projection with deep consequences for Gazprom if proven correct

Unpicking Gazprom's Western slant

Much of the politics of energy focuses on gas pipelines because Gazprom's sizable infrastructure, for all to be seen, built during the Soviet era, is like a web crawling (mostly) through the Eurasian landmass – serving Europe (a lot) and China (more recently)

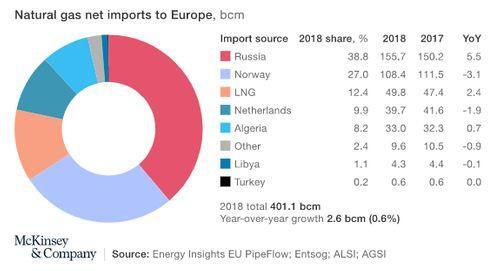

Pipe line infrastructure has transported increasing amounts of Russian gas to Europe, culminating in record sales of over 200 bcm in 2018

A lot can be said about the inordinate power wielded by the gas exporters and about the dependence of the importers, at the end of the gas line, which turned out to be Russia, with its powerful exporter Gazprom

This could become even more the case as nuclear energy loses traction around Europe and the transition from coal-fired electricity generation gains momentum in Germany, both feeding into demand for substitutes, gas along with renewable sources of energy, at least for the short-to-medium term

Exports via pipeline have historically stayed within a region or, at most, been conducted between two regions, from Eurasia or North Africa to Europe, for example

This is also the basis of the argument put forward by the US Administration highlighting security concerns and exposure of NATO allies to Russian interference

However, the argument could, and should, also be seen in reverse as a weakness inherent to Russian gas exports, overly dependent on mature European demand and lacking sufficient delivery capacity to China and to the fast growing Asian markets

'Power of Siberia', the gas pipeline to China, inaugurated in Dec. '19, is part of a comprehensive effort to rebalance Russia's energy client base but...

'Power' will deliver 38 bcm, when at peak flow level.... by 2024

Starting at 6.9 bcm initially, streamed from the Chayanda field gas field, the pipeline will be reaching 19 bcm by 2022

The Kovykta field is expected to come on stream in 2023 with production of 5 bcm and 15 bcm in 2024...

There is a long way to go indeed...compared to Nord Stream delivering 50 bcm to Germany and Europe today, and expected to double capacity with Nord Stream 2

Competitive markets

Keeping our sights on the Russian perspective of the global natural gaz markets, two factors stand out

For energy importers, sourcing LNG is a factor of flexibility in their choice of gas providers, diversification of energy sources being a strong inducement.

- This is especially true of Europe, where Russian gas has been dominant with approx. 40% of total imports, making the region Russia's most important export market

- Even more significant in the medium term, the Asian developing countries (as well as China) will become the only global growth markets for natural gas exporters, and the capacity to deliver LNG will be the game changer. By 2040, net imports are projected by the IEA to increase by 300 bcm (Asia ex-China) and 250 bcm (China)

Because of the versatility of delivery points, LNG has started to upend the traditional pricing model of natural gas markets, a marketing strategy Gazprom has perfected over decades

- Tethering its clients to the gas delivery pipelines, and for lack of alternatives (except for gas sales from one importer to another, as practiced by Germany for the benefit of the Ukraine and Slovakia until 2014, and still for the Czech Republic), Gazprom was proficient at dealing with each country separately and according to its standing ...and not loath at playing national interests against one another

- This familiar playbook is likely to crumble under the dual pressure of the European Single Energy Market regulations, in play at Nord Stream 2, and of international market spot pricing, a clean break from the link of gas pricing to oil

None of the changes will come easily to Gazprom

With pushy competitors waiting in the wings, the race is on, as we will discuss in 'Novatek Invalid tag asset, Russia's icebreaker'