Pin-insights

Alibaba and Tencent, the giant Chinese Internet companies share singular challenges as the core - and very profitable - businesses, which drove their success in China, must be reinvented

Alibaba will be drawn in highly competitive retail markets by expanding beyond the firm's stronghold in mobile e-commerce, in China and beyond

Tencent has to explore with urgency international gaming potential as expansion on the firm's domestic market grinds to a halt, under regulatory fire

Medium term, ambitious high tech projects might come to fruition but for now, expanding core business - e-commerce at Alibaba and gaming for Tencent - is all that matters

***

Competing for investor attention, Alibaba

Although the two firms consolidated their position in China by starting out from quite distinct premises, e-commerce for Alibaba and gaming for Tencent, the drivers of their market penetration are quite similar

These common drivers are the wild-fire spread of mobile access and universal adoption of digital wallets in China

Maturity is only a word in the eye of the beholder

Revenues can hardly be expected to increase for ever and new, rule-breaking market concepts are bound, at some point, to hit the buffers as their share of consumer wallets (for e-commerce) or player's attention span (for gaming) stabilizes

Maturity in markets still remains a matter of subjective evaluation .... and both firms' ambitious growth targets are reason enough to wait and see

Is Alibaba's retail business maturing ?

Alibaba still seems to be flying, unruffled by trade wars and potential economic slowdown in China while times have been less forgiving for Tencent

The e-commerce giant holds a relatively unfettered grip on Chinese domestic online shopping, but may still have to contend with slower consumer growth as market penetration is down to the smaller Chinese cities (tier III and tier IV) with weaker buying power

Seemingly unstoppable total revenue growth hardly suggests that the party is ending ....

| year | in million RMB | year-on-year |

|---|---|---|

| 2014 | 52 504 | |

| 2015 | 76 204 | 45% |

| 2016 | 101 143 | 33% |

| 2017 | 158 273 | 56% |

| 2018 | 250 266 | 58% |

| 2019 | 376 844 | 51% |

| company data | ||

Daniel Zhang, Alibaba's new Executive Chairman, expounded in his conference call, as restated in the Q3-2019 press release (Nov. 1, 2019)

Today, our consumers, merchants, and partners are entering a new journey in the digital era. We will continue to create value for them by leveraging the power of data technology to make it easy to do business for them anywhere for the decades to come. We aim to serve over one billion annual active consumers and help our merchants achieve over RMB10 trillion [equiv. $1.4 trillion at current rates] in annual gross merchandise volume by end of fiscal 2024

In 'helping merchants to achieve over RMB 10 trillion in gross merchandise volume', we understand Mr. Zhang to mean that merchants realizing approx. a quarter of total Chinese consumer sales (RMB 38 trillion in 2018) are expected to partner with Alibaba

The huge merchandise volume is not an Alibaba

Based on 9-months 2019, Mr Zhang estimates total consumer sales in China alone at RMB 30 trillion, growing 8.2% Y-on-Y and e-commerce retail growing much faster at 17% (superseded again by Alibaba's own growth of commerce retail of 25%) - company quarterly Sept. '19 (page 5)

If (under our assumption) the company's retail sales can be maintained at the 25% growth rate, Alibaba consumer turnover could triple in 5 years (by 2024), certainly a worthy target relying on a number of critical assumptions

- Alibaba remains consumer focused but, to achieve ambitious targets, its reach is likely to extend to traditional 'brick-and-mortar' local distribution and internationally

- Head-on , the strategy will encroach on Tencent's merchant network, generating smaller but repetitive orders for daily consumption

- International ambitions may be stymied by 'walled gardens' around the world, with US-based Amazon firmly rooted in Japan, heavily committed to India and to the largest European economies (led by Germany and the UK) but South East Asia could in turn

For reference, Amazon's

- for North America - $42.6bn (+ 24% over the quarter) and $61bn (including international sales) vs Alibaba equiv. $9bn (incl. intl. sales)

- for Jan-Sept 2019 - $117.1bn in North America and $168bn including international sales vs Alibaba equiv. $25.3bn (incl. intl. sales)

Even accounting for much lower average purchasing power in China and certainly in the South-East Asian markets targeted by Alibaba, comparison with Amazon's sales suggests strong growth potential in retail going forward

| Alibaba Retail | all data in billion RMB | ||||||

|---|---|---|---|---|---|---|---|

| Quarter | China Retail | Intl Ret. | Total Ret. | China Retail | Intl Ret. | Total Ret. | |

| Q4-18 | 69,8 | 5,8 | 75,6 | Q4-17 | 60,1 | 4,7 | 64,8 |

| Q1-19 | 44,9 | 5 | 49,9 | Q1-18 | 40,2 | 3,9 | 44,1 |

| Q2-19 | 58,8 | 5,6 | 64,4 | Q2-18 | 46,8 | 4,3 | 51,1 |

| Q3-19 | 57,5 | 6 | 63,5 | Q3-18 | 46 | 4,5 | 50,5 |

| 12-months | 231 | 22,4 | 253,4 | 12-months | 202,7 | 18,5 | 210,5 |

| Source - company quarterly data | pininvest.com | ||||||

Alibaba China retail sales include commissions - Total Retail includes China & International Retail

Over 12 months (as of end of Sept. 2019), total retail sales growth has been 20% and over the 9 months '19 (Jan-Sept) 22%

Our focus on retail sales set various retail related items - essentially logistics - apart to get a precise understanding of Alibaba's e-commerce growth driver

Retail sales remain at the core of the company and contribute to more than 50% of turnover

| Alibaba | all data in billion RMB | |||

|---|---|---|---|---|

| Quarterly Data | Dec 2018 | Weight | Sept.2019 | Weight |

| Total Retail | 75,6 | 64% | 63,5 | 53% |

| Tot. Core commerce | 102,843 | 88% | 101,2 | 85% |

| Total (all) | 117,278 | 119 | ||

Alibaba's business segment of 'core commerce' includes revenues related to commerce wholesale, logistics and services, growing even in a weaker quarter (such as Q-3 ending September '19) and potentially weighing down profitability

With the build-up of new business lines - in cloud computing, digital media and 'innovation initiatives' - the weight of core commerce in total company revenue is being rolled back

Whether the emphasis on new business is a strategic shift or - as Mr. Zhang seems to suggest - data technology is the latest powerful driver to consolidate Alibaba's commercial empire remains to be seen

Is Tencent's gaming empire mature ?

Challenges facing Alibaba and Tencent are eerily similar, while the powerful revenue base of each company could not be more different

- While e-commerce retail drives Alibaba, Tencent has a stranglehold on gaming

- The ventures top 50% of total turnover in both companies

Tencent

Reminiscent of Alibaba's grip on mobile retail, Tencent’s massive game entertainment market share is topping 60% in China (accounting for international sales)

In the company's accounting, gaming is reported in 'Value-added Services', engaged in the provision of online and mobile games, and in social network services (digital content such as live streaming, video streaming subscriptions and music streaming services)

| Tencent Revenue | all data in billion RMB | ||||

|---|---|---|---|---|---|

| Quarter | Value-added Services | (VAS) | |||

| Q4-2018 | 43,6 | Q4-2017 | 40 | ||

| Q1-2019 | 49 | Q1-2018 | 46,9 | ||

| Q2-2019 | 48 | Q2-2018 | 42,1 | ||

| Q3-2019 | 50,6 | Q3-2018 | 44 | ||

| 12-months | 191,2 | 173 | |||

| Source - company quarterly data | pininvest.com | ||||

Gaming is critical for Tencent’s core profitability, as discussed in ‘Tencent of China’, much like retail e-commerce is central to Alibaba's

As is the case for Alibaba in e-commerce, Tencent's share of game revenues has dropped from 80% in 2014 to about 50% today, with smartphone games and digital content services picking up flagging PC client game sales

| Tencent Revenue | all data in billion RMB | ||||

|---|---|---|---|---|---|

| Quarterly Data | Dec.2018 | Weight | Sept.2019 | Weight | |

| Value-added Services | 43,6 | 51% | 50,6 | 52% | |

| Advertising & Others | 19,6 | 23% | 19,9 | 20% | |

| Total Revenue | 84,9 | 97,2 | |||

Yearly game-related revenues exceeding RNMB 190 billion (USD 27 billion at USD 0.14 / RMB) might obscure the magnitude of the challenges awaiting the firm

- Management has laid out the plans to navigate the regulatory constraints of the domestic Chinese market and international expansion

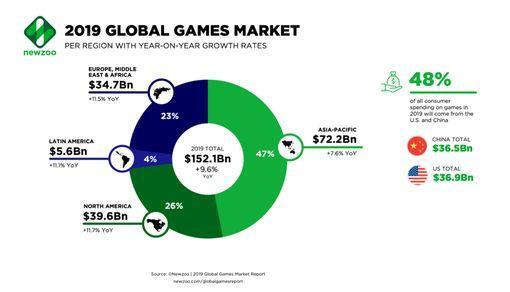

- Worldwide, gaming, projected to grow close to double digits (+9.6% in 2019 for a $ 152.1 billion turnover) according to the July 2019 Newzoo Global Games Market report, raises the stakes

Tencent's long-held international strategy of partnerships and licence agreements with many of the key videogame developers around the world is a positive...

However

- Fast shifting technologies, such as game streaming, Tencent's preferred mobile gateway may come under fire

- With emphasis on international markets to maintain growth momentum, costs of game developments tailored to national tastes and of user acquisition may be rising

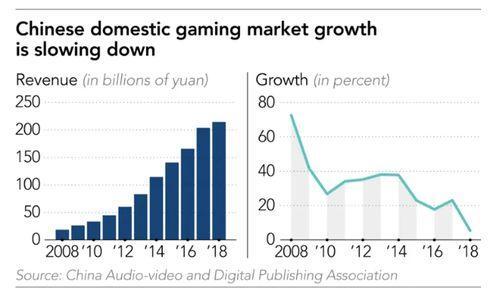

On the regulatory front, China’s nine-month licensing freeze on new games in 2018, the new approval process, as well as measures to reduce screen time among children, have taken their toll and will reverberate throughout 2019

- Tencent’s voluntary action, as well as regulatory steps taken by the Chinese authorities throughout ‘18, to block new game releases, to restrain videogame ‘youth addiction’ and to limit inducements to acquire virtual add-ons (a key source of profit) has been a major factor

- Withholding approval for new games crimped the company’s profit targets for 2018 and release dates for new games on a much reduced scale in 2019 still cloud projections today

The resulting slow-down of mobile gaming growth in China, the main driver of Tencent's player engagement, is expected to constrain the country’s premier share of the global market, still estimated at $36.5 billion, in a tie with surging US sales at $36.9 billion, according to Newzoo

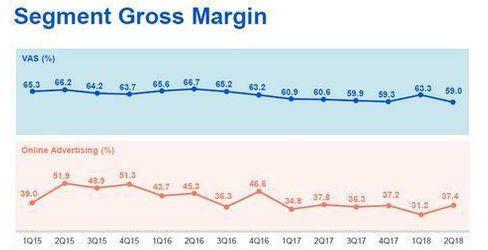

The new regulations impacted gross margin from Q2-2018 onwards

Dragging down Tencent's gross profit of Value Added Services (VAS), regulatory constraints are likely to impact full 2019 results

| in billion RMB | Jan-Jun 19 | Jan-Jun 18 | Jan-Jun 17 | |

|---|---|---|---|---|

| VAS Revenues | 97,05 | 88,94 | 71,91 | |

| Gross Profit | 53,49 | 54,47 | 43,96 | |

| Margin | 55% | 61% | 61% | |

| Interim reports | (p.50) | (p.49) | pininvest | |

While segment information on operating profitability is not provided, operating profit for the entire company is indicative of the sensitivity of gaming as core value driver

Operating profit has been taking significant hits

- Sinking from approx. 40% in 2017 to less than 20% by Q4-2018, operating margins have been regained in part by Q3-2019 at 27%

- A push for online advertising may have been - in our opinion - the stop-gap measure to keep investors on board...

- An international rebalance of Tencent's gaming empire is likely to remain the top priority

Alibaba

It is likely that expansion will come at a price as both firms have to venture beyond their familiar terrain

- International expansion is an imperative Tencent cannot skirt because regulations are putting a lid on domestic growth

- Alibaba is - in contrast - confronted with domestic priorities because - in a global perpective - the firm's international ambitions will be constrained by the many 'walled gardens' erected around the world

Because of their considerable size and investement capacity, the two firms will shake up the markets

- Alibaba's opportunities to expand on the Chinese market overlap at every turn with Tencent's WeChat 'mobile to mortar' retail network of small shops

- Tencent will be raising the bar in gaming by fine-tuning its entertainment to local tastes, with a likely focus on South-East Asia and India

Either way, profitability will suffer short term

Equity valuation rightly puts each of the two stocks in the growth segment, confidently forecasting their potential, but such expectations imply more radical transformations, relying very much on each firm's expertise in payment systems and cloud-based initiatives

Ambitions we hope to discuss in 'Withering digital wallets ?'