The commedia dell'arte of our title refers to an early form of theater, popular in Italy from the 16th century on : masked characters were following scripted, and entirely expected, set pieces conforming to well-known social types - not so different from the widely reported gatherings of EU leaders

We argue that, though uncertainties surround Italy’s domestic affairs, the very real unknowns on which the outcome of the new Italian government hinges are subsumed in the relationship with Europe - and the willingness of all parties to drop the pretenses - and the masks - of their constituencies

The relationship with Europe

Fraught by immigration issues which geography and long coasts stretching towards South towards Africa brought to a boil, the relationship with the European Union, so close and yet so brutal, is a two-way street and economic issues are at the core

Both parties have a lot to lose – Europe a trusted partner since the early days of co-founders Alcide De Gasperi and Altiero Spinelli and its considerable heft as third largest economy of the Union – and Italy would lose everything, its credit worthiness for starters, its seat at the table of all major decision on the Continent and every last shred of credibility

Public debt, the not-so-remarkable inheritance of decades of mismanagement, looming at €2.3 trillion (representing 132 percent of gross domestic product (GDP) – is second only to Japan and Greece); but the debt burden should – and will – focus attention not on reimbursements but on the sensitivity of the national budget to rising rates, a most likely scenario

In the context of a fiscal policy we will loosely define as consumer-demand driven and expansionary, the easy-going assumption creditors will be willing to provide external financing seems farfetched, implying at the very least drastic increase in bond yields and, in a worst case scenario, shutting the country out of the credit market

However, because the average maturity of Italian bonds has been extended in the years of low-interest rates, sharply rising rates will only affect new bond issues and the overall impact of the interest burden on the national budget will be dampened – a saving grace…

With domestic savers owning a very large chunk of outstanding Italian debt – 69% – the country remains insulated from international speculation (overseas holdings are pegged at 5%) but, ultimately, the ownership structure effectively ring-fences the public debt from any temptation to meddle with debt commitments or … for that matter, in its € denomination…

Italy and the European Central Bank

With the understandable lack of appetite of overseas lenders and the uniquely high share carried by domestic savers – all eyes are focused on the European Central Bank as lender of last resort

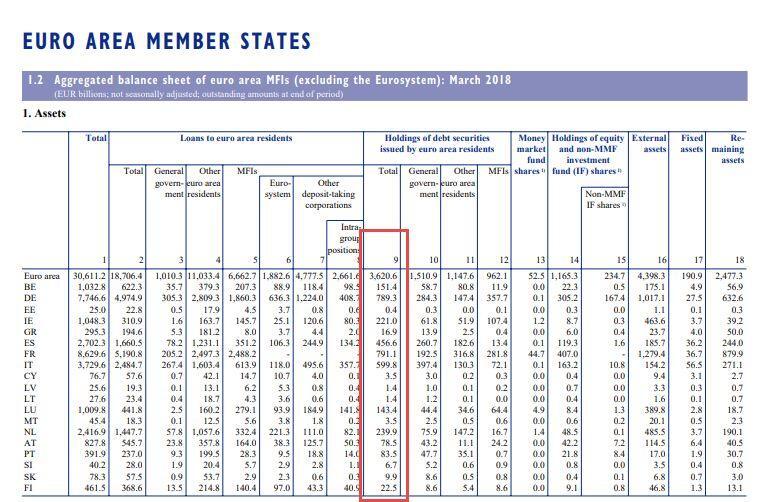

Currently (March 2018), the ECB which has been buying substantial debt through its quantitative easing programs, increasing its holdings from € 2 trillion in early 2015 to €4.5 trillion after three and a half years.

Signaling its intention to bring its bond buying strategy to a halt from September ’18, the bank’s policy – if enacted – will put considerable pressure on Italy, with a debt above 130% of GDP, weak overseas bond holders and – potentially – growing financing needs

March ’18 public debt held by the ECB - €400 billion + €200 billion (other Italian debt securities)

No other country compares

To add to the country’s uncertain financial future, Italy’s banking system’s deficit in euros by way of transfer to other countries banking system’s and domestic euro-denominated cash hoarding – in other words, capital flight – has grown relentlessly

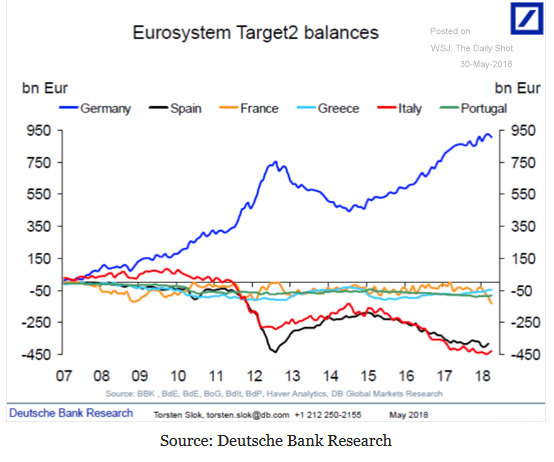

Relying on the Target-2 Reserves system, deficits are automatically compensated between the euro-land central banks but, as they build up, they turn into effective ‘loans’ from the surplus country (Germany) to the deficit countries (mainly Italy and Spain)

As of May ’18, the deficit of the Italian Target 2 reached € 426 billion

The purpose of our analysis is not to suggest what course the Italian government or the ECB may pursue but some assumptions stand out

- No, cancellation of €341 billion Italian debt held by the European Central Bank (ECB) is a no-go for the new government, whatever their program may say. Signaling the critical situation of Italy in this fashion will only make the burden much worse by cutting the country’s financial support altogether

- No, Germany will not fathom solutions ‘inflating the debt burden away’ as some commentators have been suggesting; the dramatic experience with hyperinflation which destroyed Germany’s wealth after WW1 (from 1923 leading right up to the election of Hitler in 1933) is burned in the country’s psyche and any price, including economic hardship, will be paid to keep the monster at bay

This being posited, we believe the evolving political realities in Italy and – ultimately – the credibility of the ECB, reflecting the powerful economies of Germany and of the Northern countries but also of France, will carry the day