The latest OECD quarterly report - for Q4-2020 - will not be released before February 18, 2021

There is little doubt that the new lockdown measures, introduced since November '20 across Europe, will be impacting the full-year estimates, especially in economies relying significantly on tourism, catering and hospitality (Italy, Spain and France)

However, recently published (mid-January '21) estimates by the largest OECD economies for the full year 2020 remain strictly in line with the earlier official projections (as of Nov. '20, based on the 9 months Jan-Oct. data)

The probability that this Nov. OECD 'base-line' projections will hold is thin - in the light of new waves of the pandemic spreading on the European Continent

Downgrades should be expected by next month, hitting some of the poor performing countries hard - such as France, Italy and the United Kingdom , which are dependent on international travel to support their service industry

As the economic consequences of the pandemic harden divergences between North and South in the Eurozone going into 2021, the future of the euro is a bet on the recovery of France and of Italy

For reference, the table published under the heading "OECD - a trouble outlook' based on the first three quarters of 2020 provides the most recent official projections (Nov. '20)

The data refers to Quarterly Real GDP growth, in % change on the same quarter of the previous year, Q1-20 / Q1-19, Q2-20 / Q2-19 and Q3-20/Q3-19, a measure which makes more sense than the more widely publicized % change of the one quarter over the next (such as Q3/20 over Q2/20)

| GDP % change | Q1 | Q2 | Q2 (update) | Q3 | 2020 proj. |

|---|---|---|---|---|---|

| OECD-Total | -0,9 | -10,9 | -11,7 | -4,1 | |

| European Union | -2,5 | -14,2 | -13,9 | -4,3 | |

| Major Seven | -1,3 | -12,1 | -11,9 | -4,2 | |

| Canada | -0,9 | -13,5 | -13 | -4,6 | -5,4 |

| Germany | -2,2 | -11,7 | -11,2 | -4,2 | -5,5 |

| Japan | -2 | -10 | -10,3 | -5,9 | -5,3 |

| United States | 0,3 | -9,5 | -9 | -2,9 | -3,7 |

| France | -5,7 | -19 | -18,9 | -4,3 | -9,1 |

| Italy | -5,5 | -17,3 | -17,9 | -4,7 | -9,1 |

| United Kingdom | -1,7 | -21,7 | -21,5 | -9,6 | -11,2 |

| source - OECD News Release Nov.19 | |||||

Recently published estimates by the largest OECD economies for 2020 (as of mid-January '21) are strictly in line with the earlier official projections reported in our table

At first blush, the probability that this Nov. OECD 'base-line' projections will hold is thin - downgrades should be expected by next month, hitting some of the poor performing countries hard - France, Italy and the United Kingdom

France

The French Central Bank projects a GDP shrinkage of 9% over the course of 2020, consistent with the earlier projections

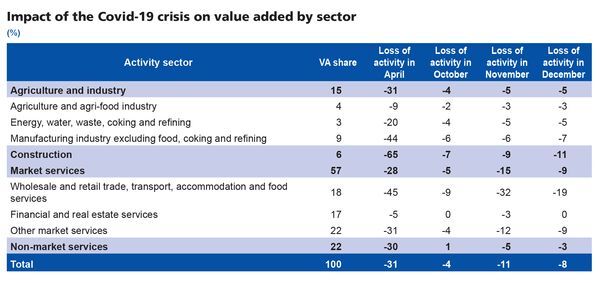

However, the Services category - Wholesale and retail trade, transport, accomodation and food services - greatly impacted by the renewed lockdown measures, paints a dismal picture with revenue losses of 31% (est. November), 18% (December) and 19% (proj. January)

As second largest segment (behind Other market services) and with an 18% weight in global GDP, the negative trend of Retail and Hospitality is likely to reflect in 2020 activity

A 10% fall (instead of 9.1% earlier OCDE projection) in 2020 GDP over the previous year is a reasonable assumption

To be reviewed in Februari....

United Kingdom

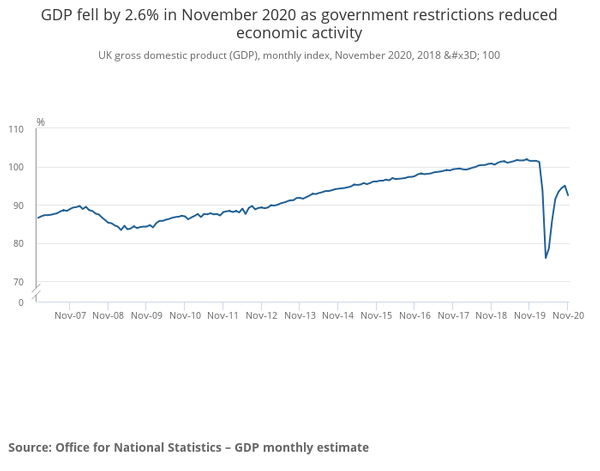

Starting out with an even weaker GDP projection at -11.2% for the full year 2020, the UK has recorded a reversal in November '20 of the 6-months upward correction, after the deep fall of April '20 (hitting a monthly GDP of 76.1 in November measured against ref. June 2018=100)

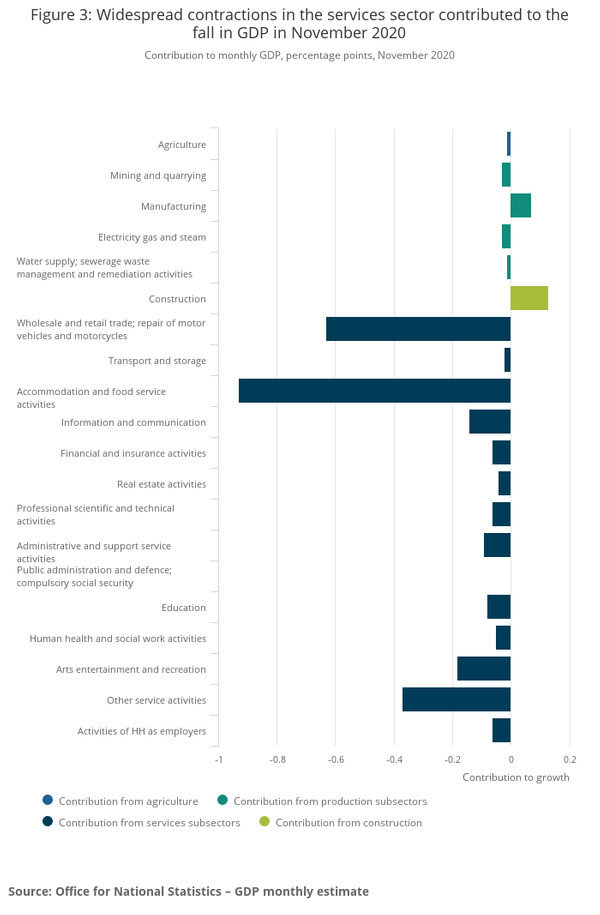

The factors behind the renewed weakness are not different from the causes experienced in France - renewed lockdown measures to combat virus spread impacting wholesale and retail trade, accomodation and food services

New stringent lockdown measures and the extension of the furlough scheme into April '21 point to a weak first quarter of 2021

The November OECD projection - a drop of 11.2% of GDP in 2020 (compared to the previous year) - heavily impacted by the economic collapse in the second quarter, still stands...

However, recovery in the first months of 2021 will be postponed as the British economy is expected to enter a dreaded 'double dip' recession, with a projected contraction of 1.5% in Q1-2021

Projections for the full year 2021 will probably be dialled down, if the weakness of the first quarter leaks in April-May (as furlough compensation extended to April already suggests)

As stated by the British Chancelor of the Exchequer on Jan. 11, "We should expect the economy to get worse before it gets better"...

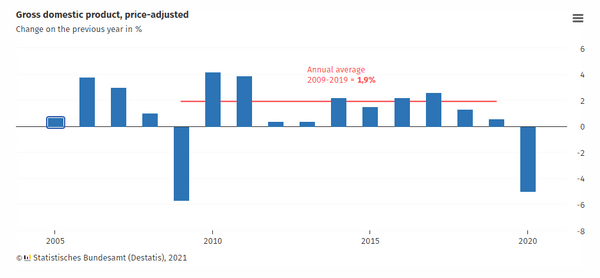

Germany

The projection for the full year 2020 by the Federal Statistical Institute (Destatis), released on Jan. 14, improves on previous OECD estimates, lowering shrinkage to 5% over the previous year

Ever precise, the Institute also provides a 'calendar adjusted' GDP estimate for 2020, as the year counted more working days than in 2019, upping the GDP drop to 5.3%

Measured against the average 10-year annual growth 2009-2019 of 1.9%, the recession of 2020 compares with the financial and economic crisis of 2008 (-5.7%)

With manufacturing rebound compensating in part the slump in the service sector, Germany is having a 'good' crisis in comparison with its largest European neighbors

What is more, strong growth is projected from the first quarter 2021, supported by the vast stimulus program launched from April

With stimulus initiatives worth 39.3% of GDP - 8.3% 'above the line' budgetary measures and 30.8% liquidity supporting loans - Germany is by far the most ambitious in Europe

Starting from a - in % - much smaller government debt - at 59.5% in 2019 - Germany could afford to...

For review , detailed statistics on European stimulus programs and budget deficits are shown in 'Headwinds battering Europe'

Italy and Spain have not published updated 2020 projections as of Jan. 15

Italy's Central Bank Dec. '20 projections - based on maintaining the pandemic at current levels through early January and gradual fall in infection rates into Q1-21 - also reflect the OECD base line of a 9% contraction

Into 2021, the rebound at 3.5% draws heavily on Gross Fixed Investment (+9% in 2021 - following a 12% fall in 2020) and on Exports (+9.3%, an upward correction of the weaker est. made in July of 7.6%)

As the new wave of infections has spread through Europe in the fourth quarter, actual 2020 contraction and estimates for the first half of 2021 will turn out worse than hoped for

Spain had downgraded its Central Bank projections in September '20 by targeting a decline in output of between 10.5% and 12.6% (instead of previous estimate of 9.2%)

The forecast was narrowed as of Dec. '20 to a band of 10.7%-11.6% fall in output

The exploding infection rate in Spain (from 10 000 on Dec. 22 '20 to 40 000 on Jan. 15 '21) may not change the view held on the full year 2020 but the impact on recovery in 2021 is all but certain

The range of growth hoped for in '21 of 4.2% to 8.6% raised the previous forecast, thanks to the impact of EU recovery funds

These investment-driven measures will be late in working through the econonmy and may not suffice

Outlook for both countries remains negative

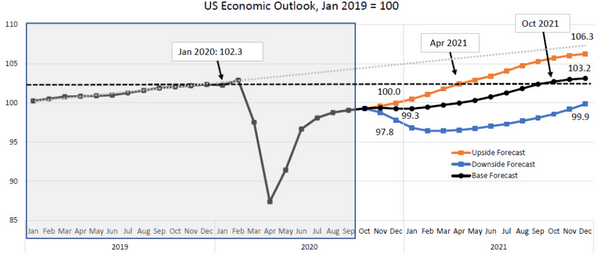

the United States

As of January 13, 2021, the Conference Board Economic Forecast for the US Economy presented a base case forecast yielding a Q1-21 real GDP growth of 2.0% (annualized rate), and an annual expansion of 4.1% for 2021, following an annual contraction of 3.5% for 2020

The underlying assumptions hinge on peaking COVID cases and gradual distribution of vaccines starting in Q1-2021, and gradual deployment of stimulus programs in Q1 / Q2 (for additional support)

The base case is in line with the previous OECD annual projection of last November (3.7%), which turned out to be spot on, supported by stronger than expected economic indicators in November and December

The difficulties encountered in the roll-out of the vaccines in the U.S. and grave concern about new waves of infections make a growth path somewhere between the base line (in black on the chart) and the downside forecast (blue line) more likely

The stimulus package which President-elect Biden expects to present might, if approved at the announced $1.9 trillion, bring the U.S. in line with the support measures allocated in the large OECD economies

The original COVID measures ($2.959 trillion - based on the IMF Fiscal Monitor Oct. 20), the package voted in Dec. 20 ($900 billion) and the Jan. 14 annoucement ($1.9 trillion) - in total $5.8 trillion - would represent 27% of GDP 2019

As shown in our table published before the additional stimulus measures were voted in December and before the recent announcements, the impact on Government Debt should be significant, coming on top of the IMF estimate of 131.2% of GDP

The forthcoming Report of the Congressional Buget Office - CBO - will be of interest

| Covid Stimulus | Fiscal Balance | General Govt Debt | ||||

|---|---|---|---|---|---|---|

| $ bn | % GDP | 2019 | 2020 | 2019 | 2020 | |

| EU (1) | 1 364 | 10,7% | ||||

| France | 535 | 21,0% | -3,0% | -10,8% | 98,1% | 118,7% |

| Germany | 1 482 | 39,2% | 1,5% | -8,2% | 59,5% | 73,3% |

| Italy | 701 | 37,9% | -1,6% | -13,0% | 134,8% | 161,8% |

| Spain | 220 | 17,7% | -2,8% | -14,0% | 95,0% | 123,0% |

| United Kingdom | 678 | 25,7% | -2,2% | -16,5% | 85,4% | 108,0% |

| Switzerland | 79 | 11,2% | 37,0% | |||

| United States | 2 959 | 14,2% | -6,3% | -18,7% | 108,7% | 131,2% |

| China | 904 | 5,9% | -6,3% | -11,4% | 52,6% | 61,7% |

| (1) European Union | ||||||

| sce-Fiscal Monitor chap.1 IMF-Oct.'20 | ||||||

While the new U.S. stimulus might be in line, as a % of GDP, with the support provided by developed countries such as the UK or France, the breakdown between budgetary measures - such as poverty-fighting measures and investments - and liquidity support (business loans) will be the deciding factor

Germany, with the largest support package, essentially allocated to temporary liquidity measures, stands out, again, as discussed in 'Headwinds battering Europe'

As new waves of infection engulf Western economies, UK, Ireland, Spain for now.... and with a predictable impact on tourism and hospitality in the aftermath of the pandemic, the consequences on the economies most dependent on service exports (expenditures by foreign tourists) will be a drag on the recovery of Southern European countries throughout 2021

By hardening the divergence between Germany and its Northern neighbors on the one hand, and the Southern countries, joined by France's fragile outlook on the other, the Eurozone will be exposed to uncertain times...