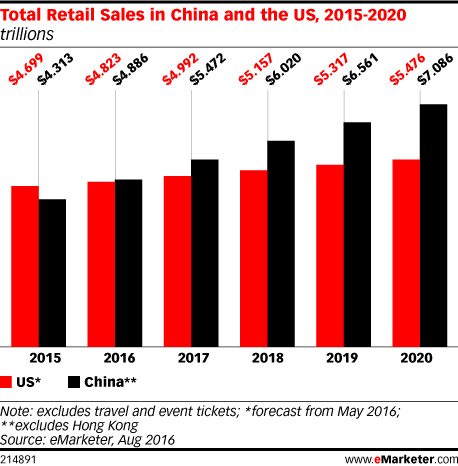

China was expected to become the largest retail market in the world...

That was four years ago, per eMarketer projections dated Aug. 2016

Surprisingly, these assumptions turned out to be incorrect, by a long shot

A comparison with what we now know of 2018-2020 retail numbers and with the trends, projected through 2014, is revealing of the priorities China and the U.S. set out for their respective economies

China's middling support of domestic consumer demand and the U.S. weak consumer goods manufacturing sector both raise red flags

If allowed to perdure, the distorsion between the world's two largest economies will beget hard-to-contain tensions

China Retail - a surprise on the downside

2018 China retail ended up more than 18% below the 2016 estimate - at $4.896 trillion

The consumption boom in China proved to be widely over-estimated

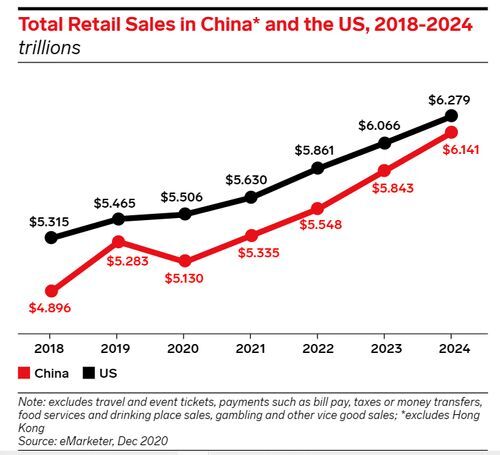

eMarketer's updated projections, as of Dec. '20, are presented below (colors are inverted - China red and U.S. black)

Starting from a much lower base than assumed in 2016, and taking a hit from the COVID crisis, 2020 China retail is expected to pull back marginally at $5.13 trillon

What is more, the growth rate of consumer spending - in line with China's economic expansion at almost 8% in 2019/2018 - could be severely constricted for the foreseeable future

At approx. 4%, the projected growth rate in retail sales is mediocre by Chinese standards but, as argued pointedly by eMarketer, the new trend line reflects the priority of business support over consumer protection

2020 U.S. retail, on the other hand, is in line with the 2016 projection, with sales holding up quite well during the pandemic, picking up speed in 2021 (+1.7%) and rebounding strongly in later years (+4% on average)

While the trends in retail sales may - or may not - play out, the priorities of U.S. economic policy may continue to diverge significantly from Chinese priorities, by favoring U.S. consumption

Economic policies at odds

In discussing macro-economic trends, comparison between per capita retail sales hold a familiar message

The stark contrast is a reminder of the very different stages of economic development reached by each country

Based on 2020 projections, per capita retail sales in China and in the U.S. are respectively $3 600 and $16 800

The wide gap - U.S. retail sales are 4.6 times higher per person - may go a long way in explaining why the post-COVID economic support reflects the fundamental structural differences between how the US and China run their respective economies; discussed by eMarketer author Ethan Cramer-Flood

As set out in detail in the referenced article, Chinese economic planners pushed ahead in Q1-2020 with an array of micro-economic measures to support business by lowering taxes and fees, reducing interest rates and utility costs for small business, and prompting regional authorities to share the cost

Still in a developing phase of its economy, China cannot afford to loose momentum

The priority of business over consumer support may be 'tweaked' in favor of consumption in the good times, but will continue to dominate with great clarity in an economic slump, as has been the case in 2020

The implications are drastic, especially considering the persisting inequality between China's coastal regions and impoverished interior, and the global imbalances, induced by the country's massive surplus in manufactured goods

The U.S. policy makers dance to a different tune, as the paramount importance of the American consumer in economic rebounds, for the U.S. and globally, is firmly established

The trend line projected in retail sales through 2024 reflects this underlying assumption - and the constrictions to which American economic policies have to adhere

...The consumer comes first , as extended unemployment benefits and stimulus checks (round 1 and round 2) have shown abundantly, one more time...

Unwanted consequences

The priority given by American politicians to consumer support is a prerequisite to attend to the needs of the hardest hit families

It is also consistent with economic priorities

The facts are worth restating as much political hay has been made around the allocated amount in the second round of stimulus - $600 - a disgrace according to many politicians, including President Trump

- The maximum amount for this second round of stimulus checks is $600 for any eligible individual or $1,200 per eligible couple who file taxes jointly. For a family of four, that would include $600 for each eligible dependent, or $2,400 in total. (In the first round, adults were eligible for $1,200 and dependents were eligible for $500) Eligibility is based on gross income at - or below - $75 000 ($150 000 for a couple) and the benefit decreases stepwise above that amount

The policy has been successful, American consumption has held up during the spring and, with the first stimulus checks, the positive impact on poverty rates has been clear

Less welcome have been the shifts in consumer patterns

- services (hospitality, entertainment, travel and tourism) have been wounded - possibly beyond recall in already fragile activities - and the rebound seems to be slow at best

- cash unspent on services has led to an upswing in the purchase of goods, encouraged and facilitated by the migration of retail stores on-line and Amazon

has been far from alone

Unsurprisingly, America's degraded potential as a manufacturer of consumer goods (textiles, houseware products, electronics, even automobiles...) resulted in a deteriorating balance of goods, as discussed in recently published 'Imbalances'

Spectacularly so...

At the most elementary level, facts - not political grandstanding - set the agenda

- With little leeway, China's support of its industrial backbone (construction, infrastructure, real estate, state-owned enterprises) is a strategic bet on the future, even if domestic consumption suffers in the mean time

- America's options are even less palatable - compelled to support domestic consumption, demand benefits to a significant extent foreign importers (and China is not alone), while the American manufacturing of consumer goods can only be rebuild over time (if ever)

The fundamental structural differences between how the US and China run their respective economies do not look promising

Because of their size, Chinese and American economic policies cannot ignore their interdependence and the long-term significance of economic policies preferred by the other party

The U.S. continues to rely on its financial strength and the reserve status of its currency, but the country's manufacturing weakness and China's long term commitment to manufacturing dominance are bound to aggravate tensions

...unless America manages to rebalance its economy....