The popular Robinhood platform has gained strong following amongst young investors with its mobile app and free trading features

Building on awareness of price momentum of some stocks, Robinhood might encourage investors to 'jump on the bandwagon' and in some cases, this might be quite good but not always...

Our series will provide some background information and focus on the inherent weaknesses - or the strengths - of some top industries and companies favored by the Robinhood investment community

Every Pininvest factsheet is supported by a theme listing companies of interest, with up-to-date pricing, performance & risk ratios, and fundamental data

Visit Tesla-related themes - The Ultimate Communication Platform - and - Electric Vehicles in China

Facts in brief

Leading the innovation in Western markets, Tesla Motors

- because the firm is not burdened by the legacy industrial investments and internal combustion know-how accumulated over decades by conventional car manufacturers,

- and because capital expenditures for Tesla cars are distributed - and expenses shared along its supply chain

The significant valuation of Tesla reflected the difficulties weighing down car makers on both counts – giving Tesla an early start in the market

But these problems have been overcome, the carmakers ponied up the cash for innovation and their line-ups of EVs and hybrids are in the showrooms

Unique technological advance of Tesla was always a dubious claim - stopped in its tracks by the firm's reliance on research and investments by its supply chain, especially battery-providers Panasonic (Japan) Invalid tag asset and CATL (China), firms who supply all the EV makers worldwide

To give a voice to yet another warning about speculative frenzy and overvaluation of Tesla Motors is very much like blowing in the wind (or rather a hurricane) of eager stock buyers

Tesla is – probably by far – the most popular ‘buy’ for Robinhood investors today and it is true that investing isn’t about being right or wrong, it’s about making money, as they use to say on Wall Street

To keep it short – and practical – here are just a few observations by none other than...

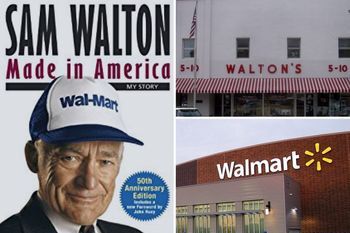

Back in 1987, Sam Walton, the legendary founder of Walmart Invalid tag asset, was interviewed about his huge losses following the brutal market shake-out on Monday, October 19 – the famed ‘Black Monday’ when the S&P 500 lost 20% on the day, overwhelming computer and communication systems

Mr. Walton – with a Southern drawl – answered with a single liner

‘Well, my friend, it (referring to his stock holding in Walmart) was paper before … and it is paper now’

…of which any investor should draw two lessons

Lesson one

As long as you have not sold your shares, all you have is paper – your wealth, and the wealth of Elon Musk, is just paper. Only once the cash of stock sales roll into your bank account can you feel richer (or poorer….!) than before

Lesson two

What Sam Walton knew to be true – and it was all that mattered to him – was his sprawling empire of retail stores – in other words, the real value behind the share price

Facts are stubborn

Yes, enthusiastic investors feel richer after jumping on the Tesla ‘bandwagon’ but they are not…

Unless they sell and take their gains off the table, it is just paper … and nothing more

Investors who still hang on to their holdings might want to remember that

- selling into a booming share price is hard (especially if the share keeps rising !); it goes against the grain of our intuition...

- selling into a falling market is even harder – much like crowding out of a cinema when the fire alarm goes off – too many sellers all of a sudden and no buyers…

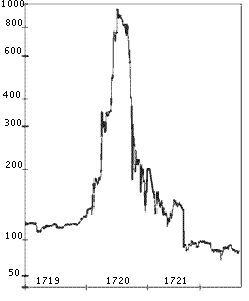

There is of course nothing novel about any of this

This is what the ‘South Sea Company’ extraordinary rise and collapse looked like in …1720, exactly 300 years ago, with a share price rising on the London Exchange from £100 to £1000

For history buffs, an early study of crowd psychology was published in 1841 (!) by Charles Mackay, studying folies, manias and economic bubbles under the title 'Memoirs of Extraordinary Popular Delusions', lauded by economists to this day and referenced by Kurt Vonnegut's Slaughterhouse Five

And, not to put too fine a point, the great financier Bernard Baruch credited Mackay's book in his decision to sell all his shares ahead of the crash of 1929, anticipating the downturn as early as 1927 ...

Measuring enterprise value

Sam Walton’s second lesson – about evaluating the company’s assets, and prospective growth opportunities – is just as powerful

...which is probably why - as reported by Market Watch (Sept. 1) - out of 36 analysts surveyed by Factset, a financial data and software company, only seven have the equivalent of buy ratings on Tesla’s stock

Asset managers, who generally know a thing or two about the industries they are analyzing for their clients, are unusually vocal

- The stream of losses is never ending and in fact, Tesla rarely made a profit on the car business - since 2014, net income was positive in only 4 quarters (Sept. 16, Sept. and Dec. 18 and July. 19)

- Tesla only got by selling 'EV credits' to other car manufacturers, as discussed in more detail in 'Tesla - avant-garde or poster child'

- Accounting numbers have been questioned frequently, especially 'Accounts Receivable' which is money still owed to Tesla by its customers - the number has been increasing over the past 3 quarters while the car sales have been dropping and Tesla buyers pay in advance ...Explanations about delayed payments on European car sales sound iffy, especially if sales in Europe are dropping (they are...)

Optimism about Tesla's entry on the S&P 500 turned out to be improvident : S&P Dow Jones did not include the firm in its latest review, as of Sept.4, 2020

A favorable decision would have provided a boost to share ownership by compelling tracker funds such as iShares Core S&P500

Earnings of the last 4 quarters, discussed in our Tesla - avant-garde or poster child, have to be positive to enter consideration for the S&P and, although no reason was given, it may not have escaped S&P Dow Jones that the sale of regulatory credits have been the only factor contributing to positive earnings

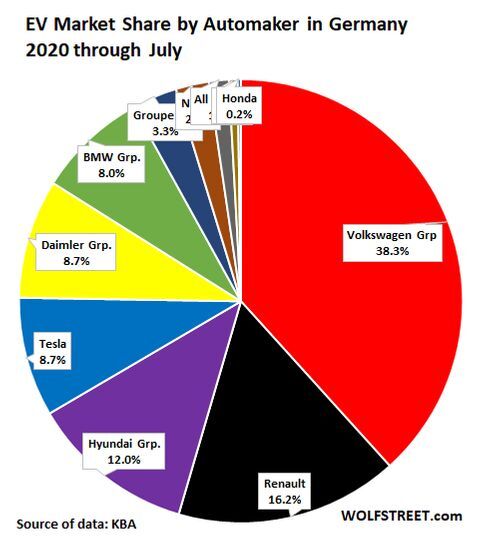

And then there is competition, heating up around the world, in the key EV-markets, China of course and Europe this year

Even the true believers must realize facts come back to haunt the best story-teller

Flatly stated, Tesla’s market value makes no sense at all, unless of course you believe Tesla is not a car maker but a 'tech' firm, which raises other questions about who owns the battery technology, the semi-conductor expertise and the radars, delivered by the all-important supply chain...

Down more than 15% by Sept. 4, the firm's market cap as of Sept. 1 2020 was close to beating the valuations of Toyota

These car makers have the experience, the know-how to mass produce and to distribute cars – and have the financial resources to launch entire new lines of electrical – and hybrid – vehicles

And they do… EVs and Hybrids under the trusted brands of these carmakers are now on the market, as in Europe, EVs strongest growth market in 2020, where Tesla is feeling the squeeze

To cap this note, we refer to a May '20 presentation made on CNBC (listen from 5'04") by Mrs C. Wood – a Tesla supporter from the early days – who explained how her investment firm – ARK Invest – bought and sold Tesla shares on a regular basis – and kept Tesla holding within a reasonable % of total holdings – 10% - letting it run - taking profit, buying again on a dip and 'trading around the volatility'

In other words (of wisdom), diversify and do not put all your eggs in one basket …know when to sell and to buy back ...even if you truly believe Tesla adventure is just starting ...