The medical device industry is a very big tent, dealing in manufacturing and sales of

- eye health devices,

- orthopedic reconstructive devices covering about every body part (hip, knee and other joint replacements,

- spine and neurovascular devices)

- and surgery

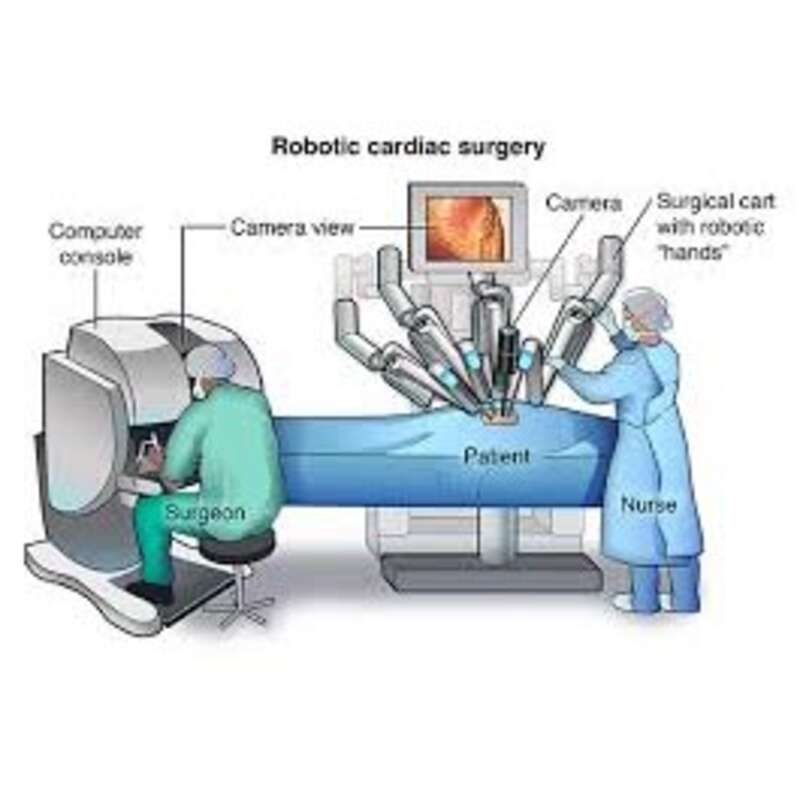

Robotics have for two decades remained a fringe specialty, invented by Intuitive Surgical

Because of benefits demonstrated over time and slowly recognized, robotic surgery has become main stream in specialty surgery such as prostatectomies or malignant hysterectomies (both over 80% of all surgeries in the US, according to Intuitive company data)

As part of a larger trend in surgery toward minimally invasive procedures, the precision allowed by robotic surgery, the faster post- surgery patient recovery and the sharply reduced number of revision surgeries have favored wide acceptance of medical robotics, at least in specific surgeries

However, sizing the opportunity for robotic surgery companies remains difficult because the addressable market is shrouded in uncertainty

- High unit costs (and cost of disposable instruments and materials per surgery performed) are constraining potential demand

- Fuzziness of the range of robotic-assisted surgeries raise more questions than can be answered

Costs of medical robotics

Unit costs remain high today, though Intuitive Surgical has been targeting more affordable price points over the last 2 years, and disposable instruments and accessories for the surgical systems are fast becoming the core profit center of the industry, reportedly 50 to 60% of revenue of established firms Intuitive or Mazor Robotics spine surgery specialist Invalid tag asset

In a range of $1million to $1.5million for top-of-the range systems and $0.5million for Renaissance systems from Mazor, and $1 500 per surgery, the market at large, both in developed countries relying on publicly financed social security and in emerging markets remains out of bounds

Currently 2/3 of Intuitive’s da Vinci robots are in operation in the US, which is indicative of cost / benefit calculations and constraints on the financial capabilities of publicly financed health care

However, if a slew of start-ups in the specialty hold their promises, miniaturization, pressure on semi-conductor pricing and robots uniquely specialized in specific surgeries could drive prices down to a very large degree

Multi-purpose robots

Today, Intuitive maintains its stance with a user base of approx. 4 700 installations with the avowed goal of expanding usage to general surgery for procedures such as ventral and inguinal hernia repair, colorectal and bariatric surgery, by developing the tools to do so

Hoping to deepen the grip on its current market, Intuitive may well be confronted by the same doubts of medical professionals encountered in the early days and – once again – costs / benefits evaluations may constrain the addressable market

This was why Hansen Medical, a start-up launched by Fred Moll after leaving Intuitive, failed to introduce robotic catheters to avoid open-heart surgery as the system could not compete with the cardiac stent

Cost / benefit ruled and still does, making the case for specialized robot devices, uniquely dedicated to repetitive tasks making up the initial investment in speed and potential volume of operations

The success of Intuitive has probably long been viewed as an outlier by the largest players in the industry, who remained uncertain about the surgical specialties involved, credible results and support both by surgeons and health insurance

While allowing for an extended, and unusual, lag in responding to the challenge, the 20-year old robotic industry Intuitive created single-handedly is about to confront a wave of novel alternatives

Robotics competition – a fragmented landscape

The singularity of the medical device industry resides in

- a wide range of clearly differentiated devices in orthopedics, eye health and surgery requiring distinct and specialized expertise in research and manufacturing

- non-overlapping specialties, such as joint replacement, spine and neurovascular devices or wound closure (surgery) where narrowly focused research by start-ups have a realistic chance of a technological break-through

- a few multi-billion companies with deep coverage of devices, supporting most, if not all, of these specialties with their distribution network

Johnson & Johnson

Size as gateway to efficient commercialization is demonstrably the critical differentiating factor in the industry, fanning a never ending cycle of acquisitions and disposals by these global companies to upgrade and adjust their product selection

Johnson & Johnson, the largest company in health worldwide with sales of approx. $27billlion in devices in 2017, is leading this global trend

- Some acquisitions stand out, such as the purchase of Swiss-based orthopedics major Synthes in 2012 (for $21billion), expanding exposure to international markets and trauma surgical devices

- According to the 2017 annual report, referring to all the JNJ divisions (pharmaceuticals, devices and consumer), "17 acquisitions and licensing agreements of various sizes" were completed that year

- As of March 2018, the company announced the sale of its LifeScan Inc unit (blood glucose monitoring products) for an expected $2.1billion to a private equity firm and in June, the sale of Advanced Sterilization Products to Fortive for around $2.8 billion

What growth by ‘bolt-on’ acquisitions – and the reshuffling of portfolios – imply is that the largest players in devices have in effect often been outsourcing a significant part of research to smaller companies, as attested by the relatively small % of their total revenue spent on R&D

| in bn USD | in million USD | |||

|---|---|---|---|---|

| Mkt Cap | Revenue | R&D | R&D/Revenue | |

| Johnson & Johnson | 368 | 80 684 | 11 252 | 13,9%(*) |

| Medtronic | 130 | 29 947 | 22 90 | 7,6% |

| Stryker | 64 | 13 040 | 8 23 | 6,3% |

| Intuitive Surgical | 61 | 3 455 | 3 61 | 10,4% |

| Zimmer Biomet | 25 | 7 918 | 3 81 | 4,8% |

| Smith & Nephew | 17 | 4 765 | 2 23 | 4,7% |

| Mazor Robotics | 1,2 | 65 | 8 | 12,3% |

| TransEnterix | 1,1 | 15 | 21 | 140,0% |

Dedicating their efforts – and financial resources – to the development of new technologies, but falling short on the organization of a sales network, the start-ups have been prepared to bring their invention under the large umbrella of major distribution networks, controlled by the majors

This business model, fine-tuned by the majors over the years, may explain why Intuitive has been able to create an entirely new product category

- Surgical robots could not be ‘bolted onto’ any existing device category - and were probably viewed as a doubtful proposition in the first place

- Distribution could not rely on the existing sales organization of a major because of its dual functions: presentation and sale of a complex system – and clinical sales follow-up (and on-the-spot training)

Today, a broad market may be opening for medical robots but, to challenge Intuitive or to broaden the field for new medical situations, the hurdles are not for the faint-hearted

- For approval of robotic solutions, systems must pass a test of ‘equivalence’ of existing robots on the market, as Transenterix

discovered when its Surgibot was rejected by FDA in 2016. In effect, new systems are expected to bring technological ‘improvement’ and manage to bypass the patent bulwark erected by Intuitive - While robots were arguably sophisticated additions to the surgeon’s ‘toolbox’, the build-up of interconnected robotic databases changes the paradigm in profound ways

- While nimble start-ups may tweak robotic applications and offer attractive ‘step-up’ solutions in specialized segments – such as exist in orthopedics – the challenge confronting the major players is develop the research capability and embrace robotics 2.0 or 3.0 – all at once…

Success and failure will be discussed in our follow-up note Robots - orthopedic evolution, surgery revolution