Russian gas exports sit at the cross-roads of geopolitics, Cold War memories, renewed anxieties about Russian influence, and competition for market share, as abundant gas is flooding the world markets

Essentially a commercial understanding beneficial to both parties, gas exports since the 1970's from the USSR have served Europe's energy demand and are replenishing the coffers of the Russian State to this day

However, the rise of the US as a major energy exporter since 2017, with a large and increasing gas oversupply, has roiled global markets : American gas production and vastly increased shipping capacity of liquid natural gas (LNG) will press for market share in every region across the northern hemisphere

LNG may not make the front pages every day (maybe it should), but the interests of the world's most powerful exporting nations and of no less powerful importers keep raising the stakes

Europe stands out as a preferred US LNG destination where traditional exporters are most likely to be curtailed drastically, because of the volume potential and a price structure making costly LNG palatable

All of which has brought the existing network of gas pipelines linking Europe to Russian gas fields in focus, as the potent means of Russian leverage on gas price structures, putting the more costly American LNG at risk

And a worst case scenario, from the American perspective, will be further increase of Russian delivery capacity with additional pipelines - which is about to happen

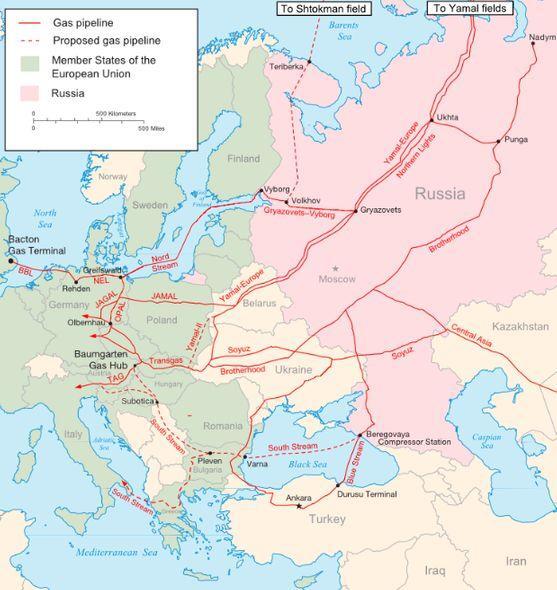

Nord Stream 2, the pipeline in the final stages of construction on the bottom of the Baltic, linking Russian gas fields with German and European markets, is emblematic of disjointed interests of America and its European allies over energy access, but also of the contradictions festering at the core of Russia's energy policies

Very much in the news with an aggressive push by American congressmen against Nord Stream, arguing on behalf of European security, the US pressure needs to be reevaluated in the light of commercial interests, of American eagerness to gain market share from inimical exporters (Russia) and of Russia's vested interest in energy exports

Competing on a mature - and probably shrinking - European energy market, both contenders, the American and the Russian, act on multiple and contradictory agendas, as climate change weighs in as the real game changer

The potential energy demand of the Asian countries is - to a degree - still a blueprint with many contenders - from Australia to Qatar and Malaysia, all in the top 5 global natural gas exporters - hoping to crowd the emerging markets with gas

On the other hand, the emergence of the US as a major natural gas exporter is a fact with which all its competitors have to contend

New kid on the block

Facts are facts and the World LNG 2020 report spells it out...

There were just four major natural gas exporters in 2019, hogging close to 60% of global exports : Qatar (22%), Australia (21%), the US (10%) and Russia (8%)

Malaysia (7%) and Nigeria (6%) rank below the big four

The big shifts in export volumes highlighted in the report will set out the competition between the US and Russia, which may be overlaid by geopolitical considerations, but is not less commercial

Russia's LNG exports grew from an average of 15 bcm (billion cubic meter) through the early 2010's to 24.9 bcm in 2018 and increased by 60% year-on-year to 39.4 bcm in 2019; LNG however remains marginal compared to Russian pipeline deliveries on European markets (more than 200 bcm per year)

The US LNG exports increased by 63% in 2019 and is on track to have the biggest global LNG export capacity by 2024, according to Reuters, expected to surpass the capacity of Qatar, the largest exporter in 2019, by 40% and the capacity of Australia by approx. 20%

The other major exporters are not expected to increase shipping capacity over the same period

The table sets out where the major LNG exporters shipped liquefied gas in 2019, with destinations concentrated in the northern hemisphere (98% of global LNG consumption)

- Exports from the majors are shown by importing region and total volume shipped globally by each exporter is in million tons (Mt)

| Importers | Qatar | Australia | U.S. | Russia |

|---|---|---|---|---|

| Asia (1) | 39,1% | 44,6% | 8,9% | 16,4% |

| Asia-Pacific (2) | 28,1% | 55,4% | 28,1% | 30,0% |

| Europe | 30,2% | 37,6% | 51,5% | |

| Other (3) | 2,6% | 25,40% | 2% | |

| LPG in Mt | 77,8 | 75,4 | 33,8 | 29,3 |

| (1)China-China-Taipei-India-Pakistan | ||||

| (2)Japan - South Korea - Others | ||||

| (3) Other export destinations | ||||

| 2019 data - source World LNG 2020 | ||||

Considering market shares and relative production, 2019 exports were setting the scene for brutal confrontation on a market where supply in over-capacity chases weak and fickle, weather dependent, demand

- Qatar may feel secure with vast reserves, balanced distribution and the benefit of proximity to large and potentially growing demand in Asia where LNG is an alternative of coal-fired power plants

- Australia, by geographical fate, is entirely dependent on Asia and foremost Japan (40% of total exports) and China (37%), a factor of uncertainty if competition for a stake in the world's only growth region heats up (as it will)

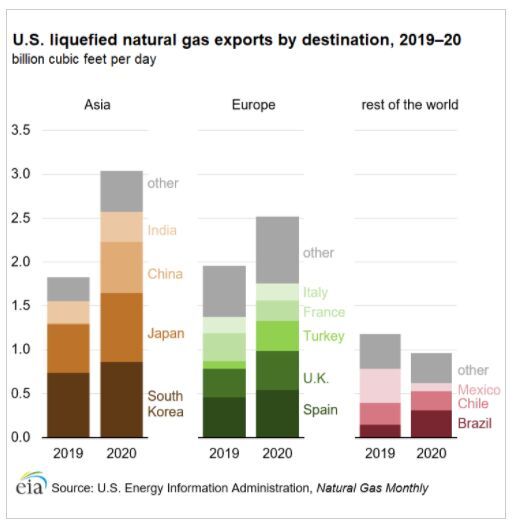

On Asian markets, the US exporters had been relying exclusively on geopolitical allies in 2019 - South Korea and Japan

In 2020, US shipments grew by approx. 60%, making the region the top destination of US LNG exports (45%) because China entered the fray

- South Korea and Japan took in approx. 12% of total US exports

- On the regions' large markets, India's LNG imports from the US remained modest (approx. 6.5%)

- Exports to China, negligible in 2019, grew strongly to approx. 9% of total US shipments following easing of the long-standing trade war in which China had raised tariffs on LNG imports from the United States to 25% - now reduced to 10%

Nevertheless, the Chinese market will continue to be evaluated with caution - because the priority given to domestic gas production is well-publicized, piped gas whenever available is competitively priced and LNG is likely to remain marginal on cost basis alone (PetroChina is said to report losses on its pipeline and LNG imports)

American progress in India seems doubtful because of Qatar's geographical advantage and India's continued dependence on coal while exports to China are likely to remain hostage of geopolitical tensions

With the large capacity build-up planned in the US through 2024, and Asian uncertainties, the attention paid to European markets by the American energy exporters, and by US governmental entities, is not likely to abate

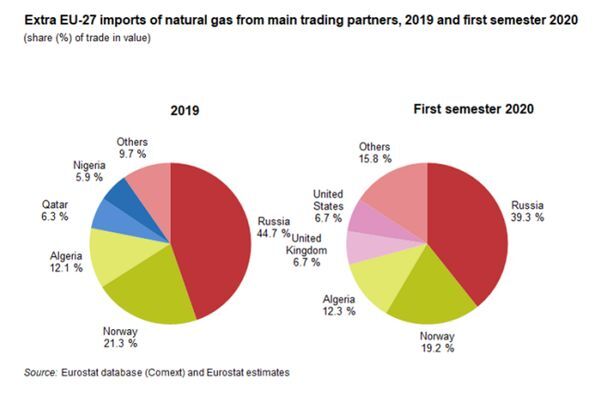

Gas is mainly sourced by European markets over Russia's Gazprom

- According to S&P Global, Germany remained Gazprom's biggest market by far, though 2020 saw a sharp fall in sales of 14.3% to 45.8 Bcm on lower demand and increased imports from Norway

Hungry exporter sizing up European markets

The US are expected to lead the charge for natural gas production, adding nearly 200 billion cubic meters (bcm) by 2025 to global production through shale and tight gas reserves before leveling off in the later part of the decade

America's forecasted growth in gas extraction is a driver for vastly increased shipping capacity of LNG, which in turn will build up pressure with urgency for market share in every region across the northern hemisphere

Amongst preferred US gas destinations, Europe stands out as the LNG market where traditional exporters are most likely to be curtailed drastically - impacting Qatar's LNG shipments to Turkey, Spain and Italy (14.5 bcm in 2019 total) but taking aim foremost at Russia's global gas deliveries of more than 200 bcm annually

From an American perspective, uptake from the European markets offers the potential to balance the significant increase in energy volumes brought to market

- demand in Europe may be maturing but domestic supply is falling with the large Dutch gas field of Groningen close to depletion

- even if the push for renewables in Europe will curtail fossil energy demand, buid-up of alternative energy sources will be slow which leaves a critical opportunity for American LNG in the early years to mop up its over-production

- with natural gas a relatively high-cost fuel and related investment in liquefaction, transportation and regasification, affluent European consumers offer more prospects than the still precarious demand of emerging markets

From Russia to Europe, LNG deliveries in 2019 were approx. 20.5 bcm (billion cubic meter), and 228 bcm delivered by pipeline

From the US to Europe, LNG deliveries in 2019 were approx. 17.3 bcm

Because LNG comes at a premium derived from extraction and infrastructure costs, European take-up will be more of a geopolitical consideration (spreading exposure away from Russian gas deliveries) than a choice on price alone, especially with competitively priced gas delivered over one of Europe's numerous pipelines connected to Russian gas fields

The stage is set for...

False flags

Simply stated, the 690-mile pipeline on the Baltic seabed, Nord Stream 2, with a yearly capacity of 50 bcm (billion cubic meter), is expected to add 20% in capacity to record 2018 Russian exports of 251 bcm

The increased gas delivery capacity from Russian fields will further reduce market opportunities for American energy suppliers, reduced to a marginal position and exposed to the vagaries of the spot market

In a fight against such an unenviable prospect, the US gas industry is caught between realities shaped by strategic choices made 50 years ago and its own ambitions for the future

History has been shaped over half a century by Germany's 1970 Ostpolitik which led to a close engagement of the former USSR as energy supplier to European markets and an expanding network of gas pipelines across Europe

US gas exporters have entered global markets over the past 3 years by becoming a net exporter since 2017 with great ambition, large production capacities from shale formations but significant cost constraints

This is not to suggest that the relentless pressure on its European allies, and mainly on Germany, to abandon Nord Stream 2 does not retain a geopolitical dimension, next to simple commercial interests

American rejection of the pipeline project has been tardy - since 2019 with a pipeline almost 90% finished at a cost of approx. $1.9 billion - but insistent

The arguments have been discussed extensively in the Nord Stream reports, published on this blog from the early Russia's Rattenfänger - Dec. 2019 - to the recent Nord Stream 2 - Cause célèbre ? - Feb. '21

As is often the case, true geopolitical considerations, based on shared security interests of the NATO allies, lose some of their edge by tangling with commercial interests

Pushed to excess, worthy concerns are twisted in haste and their potential consequences mostly ignored

- The American veto of Nord Stream comes under the guise of a defense of Ukrainian interests (since current gas delivery by pipelines through the country and related transit fees would be reduced) - except for the fact Ukraine has signed an agreement with Russia in Dec. '19, agreeable to both sides

- Much is made of Europe's dependence of Russian energy, which could expose American allies to undue pressure - the concern might be valid, were it not that Russian gas has been delivered for decades on strict commercial terms (with a single exception much to today's Russian embarrassment)

- In fact, while Russian gas deliveries represent approx. 40% of European consumption, dependence should probably be read in reverse, because energy exports represent approx. 63% of Russia's foreign trade and 40% of the country's budget revenue

Legislation, voted by Congress on a bipartisan base, might have been motivated by a mix of commercial lobbying - the leading force seems to be Sr. Cruz, of Texas - and of real concern for international security

As of March '21, Congress is going for broke

- pressing the Biden administration by putting a hold on final confirmation of President Biden’s CIA director nominee William Burns

- insisting on the legislative mandate to identify and sanction any and all entities involved in the pipeline’s construction, which would include not only Russian pipe laying ships but German entities and officials

Nevertheless, the confusion between commercial - mostly unstated - goals and genuine military risks has undesirable consequences in foreign relations

- The fact that congressmen are ignorant of the EU regulatory energy framework, set out by the groundbreaking legislation of the 2009 EU Third Internal Energy Market Package, prescribed and accepted by Russia's Gazprom, is a minor irritation

- Disregard of the interests and policies of an ally which is also one of the world's most powerful countries, Germany, is controversial

History looms large over the heart of Europe, and the very fortunate turn of events, following the two German attempts to dominate Western Europe at the cost of two world wars, resulted directly from enlightened American leadership after 1945, the launch of the Marshall plan to set Europe on the road of economic recovery and the military Atlantic Alliance guaranteeing Europe's security

Decade-old American engagement has done much to establish a steadfast alliance with Germany, but the end of the Cold War and the reunification between East- and West-Germany has not only reestablished the country's undisputed dominance in Central Europe...

Pulled eastward, Germany has grown more powerful, but the country is also drawn to foreign engagements balancing its security interests between western alliances and eastern enticements

Engagement with Germany has become a two-way street of shared interests, never to be tested because it is Germany which provides ballast to the European Union, the beacon of democratic countries on Eurasia's seaboard

America's essential partner will probably not be thrown off track, but marginal shifts might sustain distinct perceptions of the same strategic concerns

America, out of eagerness for a short-term 'win' on the gas export markets, could end-up trading trust for dubious economic advantages

"Fools rush in where angels fear to tread" - Alexander Pope, An essay on criticism (1711)

"Russia - Novatek's icebreakers" will consider Russia's strategic options on the global energy markets