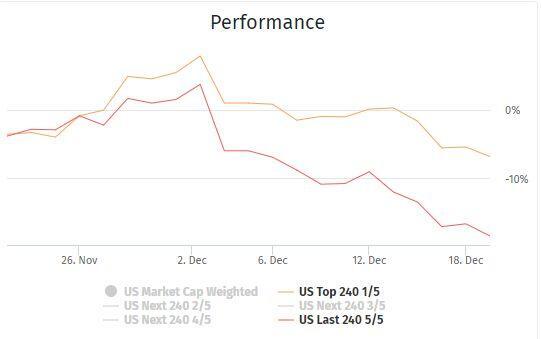

In our occasional series about small-cap market trends, Market indices in times of doubt and Downturns & Small-Caps, we have been highlighting the disturbing trend of 240 small caps of our Total Market index (including 1 200 shares)

We noted the second sharp drop in small cap performance as of Dec. 4 (following the initial sell-off from Sept. 17, anticipating the October Total Market pull-back by approx. two weeks )

A widening gap

Tracking the negative performance gap with the top 240 large-cap shares, the Dec. 13 differential of approx. 8% - over a 1-month period – has been growing to 11.5% as of Dec. 20, in 5 trading days

Our readers may reset the pinindices charts on a daily basis for preferred time frames (1 month or 3 months are recommended) to confront performance charts with volatility – to either confirm or dismiss the trend which appears to be taking hold

Our Downturns & Small-Caps comment provides further information on the constituents of the small-cap segment – highlighting some outstanding asset performances as well as broader industry trends

But, considering the negativity in current market trends, it is advisable to cross-check the observations with sector analysis of the total market

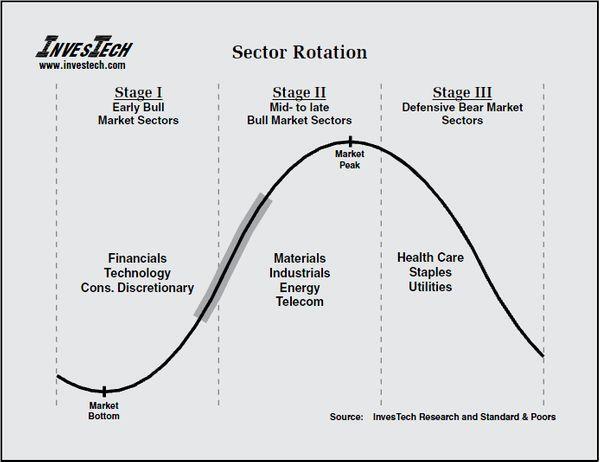

Sector rotation

Sector analysis is based on the straightforward assumption all sectors are not equally exposed to the broad economic cycle

By rotating a portfolio between sectors, an investor hopes to anticipate broad cycle reversals – picking industries that will benefit most from expected future growth – or – on the contrary, rooting for industries best protected against probable economic weakness

- Growth forecasts can be expected to favor technology, materials, and heavy equipment, construction and other industrial goods benefiting from the investment upswing

- Protection against economic downturns will on the contrary be found in consumer industries and services most likely to weather the storm, defensive sectors such as healthcare, consumer staples (non-durables) or healthcare

Obviously, while all business cycles follow the same predictable phases from recovery, followed by expansion, to contraction, the timing is usually difficult to anticipate

On average, business cycles since 1945 have lasted a little less than 6 years, according to the NBER, with one-year duration of recessions, but this has not turned out to be true in the current cycle, seemingly stuck in late-stage expansion, supported by accommodative credit conditions

To further complicate a sector-driven analysis, sectors such as energy, technology or industrial goods are impacted not only by the economic cycle, but also by structural developments (expanding domestic energy resources), by transformative R&D (in technology) or by global trade (of most industrial goods) - the interplay of multiple drivers creates further uncertainty

The poor performance since September 2018 of the sector rotation ETFs, listed in our 'smart-beta' funds category, signals the complexity of momentum-based investment strategies today

Sector performance and volatility are valuable indicators of broad market trends, not investment recommendations

Draw your own conclusions

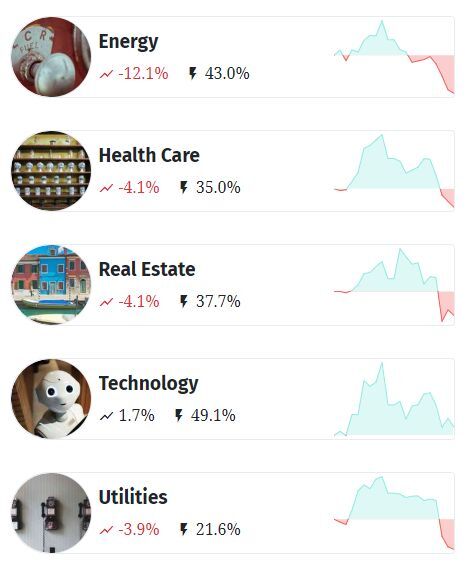

To facilitate comparisons, the pinindices sector dashboard offers an overview of all 14 sectors of our Total Market 1 200 Index, and is updated daily on basis of end-of-day prices of the constituents

- look at several time frames (1 month, 3 – 6 months and full year)

- confront sector performance with risk exposure (volatility)

Note that performance data are based on daily observations while volatility data are averages of daily observations over time – signifying a trend

In brief

We will highlight a few personal observations

Until a month ago,

- defensive sectors had been holding out – this benefitted consumer non-durables, services, healthcare, real estate and utilities

- all the other sectors were, sometimes substantially, in the red

This is not true today (as of the Dec. 19 end-of-day market)

- Over a 3-months period, all sectors are either routed or marking a negative reversal from a defensive position (non-durables, services …)

- Over the past month, Services (+2.1%) and Technology (+1.7%) are the sole sectors which did not finish the reference period negatively

Weekly review of the data calculations on the pininvest sector dashboard is warranted to track the current trends

Definite conclusions can wait another day...