[March 1, 2021 update]

Rocket Lab, one of the promising new satellite launching companies described in this note, announced its decision to go public through a merger with a blank-check firm (SPAC) backed by private equity firm Vector Capital, in a deal that values the combined entity at an enterprise value of $4.1 billion

With a proven record over delivering 97 satellites on orbit and plans to launch a satellite to the lunar orbit for NASA this year as a precursor to its Gateway program, Rocket Lab is following the example of Richard Branson’s Virgin Galactic

According to Reuters, satellite data company Spire Global also agreed to list through a merger with blank-check acquisition firm NavSight Holdings

To fuel some more white-hot excitement in the space industry, Rocket Lab announced a new rocket, Neutron, much larger and powerful than the company's current 'Electron' rocket, which will be designed to carry 8 metric tons (around 18,000 lbs) to orbit (about 27 times the payload of 'Electron' at 660 lbs)

From the existing launchpad on Wallops Island (Viriginia) and starting in 2024, Rocket Lab expects to service increased demand from customers launching large multi-satellite constellations, as discussed in this note

[end of update]

Space conquest remains shrouded in ambiguity about what is to be conquered and how...and human reach beyond Earth retains a dreamy sense of wonder

At the risk of shattering illusions, space enterprises today - either in the manufacturing of satellites, in rocket launch or in communications and data collection from outer space (and back to Earth) - are made possible by progress in technologies relying on semiconductor miniaturization, on 3D manufacturing processes or on AI software analytics, often developed and implemented in everyday products

In the effort to put this expertise to work, a trip to Mars may be a great cover story, but the somewhat more pedestrian reality should be sought in the start-ups which manage to integrate the latest technological advance - almost on-the-fly - in space enterprise

...which is why SpaceX, with its spectacular rocket launches (and blasts) and its space-travel plans, should be beter known - and admired - for its audacious attempt to reinvent broadband connectivity

E. Musk's SpaceX ventures focused broad investor awareness in private space initiative, loosening the dominance of public funding which determined the options of space authorities almost forever

However, the firm's strategic shift towards experimentation on a grand scale to harness space access in the resolution of communication problems may be even more consequential

Seeding the near-above (at an altitude of 350 km or even less...) with ten's ot thousands satellites may, or may not, prove relevant....

But the experiment is unleashing an array of novel issues, from technical feasiblity of SpaceX's large fleet to quality of the feed (latency of signal transfer) and actual cost to the consumer - a competition set against the background of growing specialized data demand which may be the true prize

SpaceX and its large challengers may be the best known ventures, presented in this note, but a multitude of satellites orbiting in constellations are likely to open very novel perspectives in their own right

In an attempt to foretell the future, however, truly radical transformations might be found elsewhere, in the data cloud the satellites will support....

...a computational shell of sorts and, very probably, a promise of data applications yet to be invented...as we hope to show in forthcoming reports

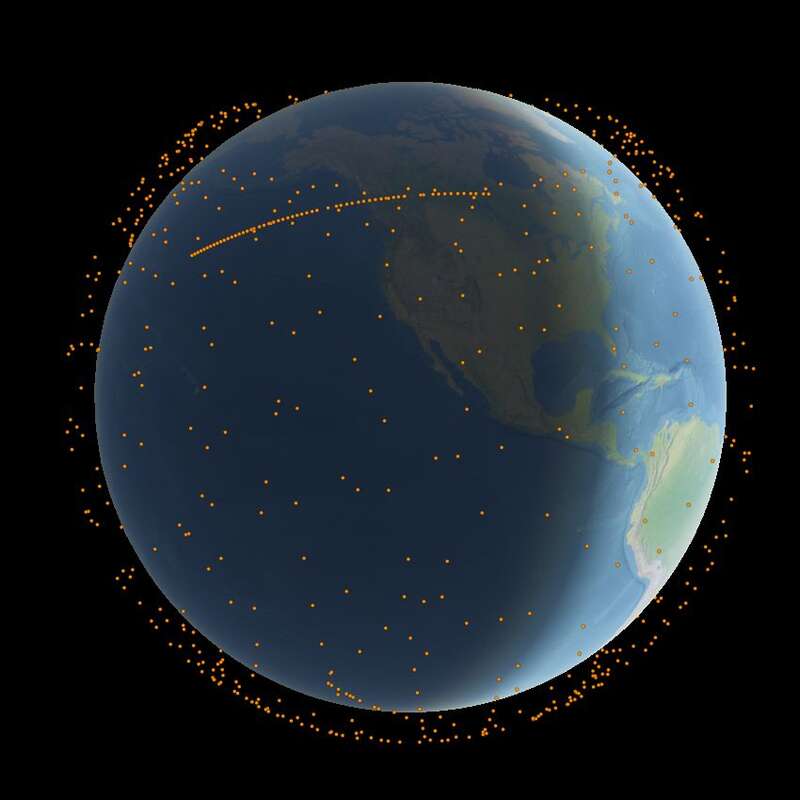

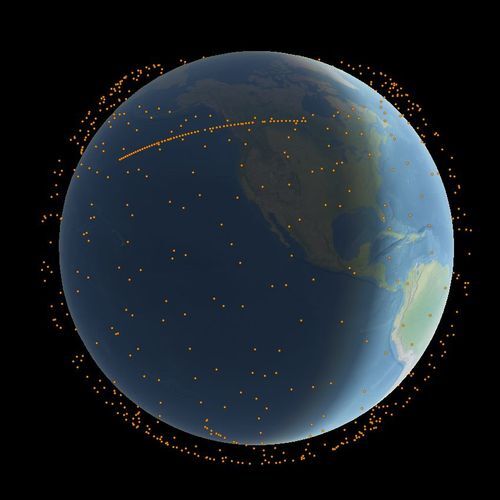

LEO revolutions

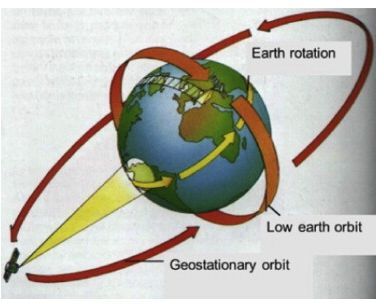

LEOs, the Low Earth Orbiting satellite networks, are a technological wonder

Circling the earth at much lower altitude than the geosynchronous satellites which hover above Earth at 22,236 miles in perfect alignment with the planet’s rotation, LEO networks form a constellation of small satellites

Orbiting close to Earth and passing over the horizon in a matter of minutes because the satellites move so much faster, completing a full circuit of the planet in 90 to 120 minutes (at approx. 27 000 km - 17 000 mile - per hour), any one receiving satellite will need to bounce the signal across the constellation before reaching the right destination back down

For the same reason, ground stations communicating with constellation satellites will be tracking satellites of the constellation as they move across the horizon quickly, and begin communicating with new satellites as they come into their field of view

In forward looking fashion, connection to the constellation will be either by cell tower to transfer data to and from a mobile phone network (substituting for fiber optic or cable), or by individual ground antennas (in homes, businesses or even cars)

On the way back from the constellation, data will find its way to destination over the Internet by large ground based ‘gateways’

No part of the enterprise has proven easy

The rise and fall of Iridium

Iridium filed for Chapter 11 bankruptcy in 1999...; bankruptcies and downsizing since the 1990’s tell the same story forTeledesic, collapsing in 2002, and Globalstar, restructured in 2002

In a dramatic reset, technology miniaturization and economies of scale achieved by manufacturing satellite in large numbers with off-the-shelf commercial components reduced unit costs of satellites orbiting in a constellation

Compared to customized geostationary satellites, years in the manufacturing, weighing up to 6.5 tons for legacy satellites (such as the Intelsat Epic NG) Invalid tag asset, at costs into the tens of millions and required to last a decade (or much more), the new satellites units come cheap, and the smallest at prices as low as a few hundred thousand dollars and expendable (with a life span of 3-5 years) - supporting a cottage industry of companies focused on imagining, data analysis and security

Occurring concurrently, a breakthrough in rocketry, lowering the cost of getting satellites into orbit, has brought the vision of entrepreneurial ‘constellation builders’ within reach

By carrying multiple ‘feather-light’ satellite payloads on a single rocket – from 60 up to a recent record 143 satellites on a single SpaceX rocket (January ’21) – and with reusable rocket boosters (recovered a record eight times for one Falcon 9 SpaceX rocket, also in January ‘21), launch costs also tumbled

SpaceX’s innovative launching services and satellite technology opened the way and experimentation with recovery of ‘Starship’ rockets in their entirety would, if successful, reinforce their competitive advantage in the launch of heavy loads (up to 100 tons)

The next stage in space access was no less predictable with purpose-built rockets to carry loads of light-weight and single purpose satellites into orbit, at low cost and with high frequency launches

Rocket Lab, which has flown its Electron rockets 18 times with 16 successes and 2 failures, is a competitor in this segment at $6 million per flight (2018 list price), compared to SpaceX current costs of $62 million to $90 million (depending on the rocket) – a price SpaceX hopes to drop to $2 million with Starship spaceship, according to E. Musk, and carry up to 400 satellites at a time

One of the most valuable rocket specialists after SpaceX, at $2.3 billion (Dec. ’20), Relativity Space is developing the first aerospace platform to integrate machine learning, software, and robotics with metal 3D printing technology to build and launch rockets and other aerospace products in days instead of years

Launch deals with Telesat and MU Space that could validate Relativity’s innovative approach

Because many of the constellations being built today have individual satellites weighing in excess of 500 kg (1,100 lbs.), satellite launching companies are planning for more powerful launchers - Terran R at Relativity with a payload capacity of over 20 000 kg (more than 44 000 lbs.) is expected to be 16 times more powerful than current rocket Terran 1 - and Rocket Lab's new 'Neutron' rocket at 18 000 lbs is also in a different category at 27 times the pay load of its 'Electron' (660 lbs)

Mars may remain a dream …but the race to conquer the low earth orbit is on and SpaceX is throwing down the gauntlet

Constellations – SpaceX arbitrage

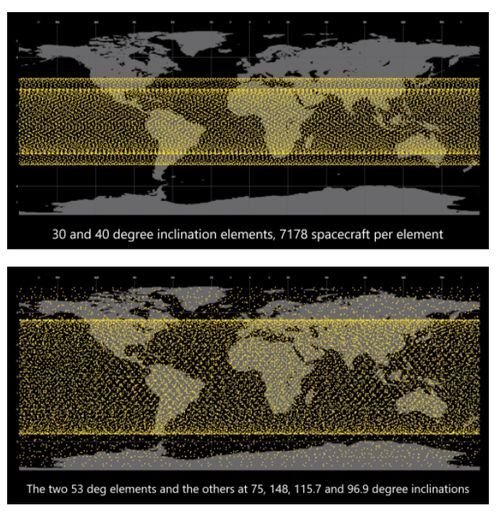

With the ambition to build a ‘mega-constellation’, SpaceX secured approval in 2018 for the launch of 12 000 satellites by FCC (Federal Communications Commission) in two ‘orbital shells’

- 4 425 satellites of the LEO constellation at altitudes of 1 110 km (690 miles) to 1 325 km (823 miles)

- and on a new VLEO (very low earth orbit) for 7 518 satellites operating at altitudes from 335 km (208 miles) to 346 km (215 miles)

In April 2019, following a new request by SpaceX, FCC approved a third orbital shell, to be seeded by 1 600 satellites, at an intermediate altitude of 550 km (340 miles), transferred from the envisioned LEO constellation at 1 110 km altitude (reduced to 2 800 satellites)

Still another May ’20 request for an additional 30 000 ‘second-generation’ satellites,

- almost quintupling coverage at very low altitude (VLEO) with an additional 25 000 satellites

- and close to quadrupling the intermediate orbital shell (+ 4 000 satellites),

strongly points towards the experimental approach of as yet unsolved technological challenges at very low orbit

The concern about latency (response time in satellite connection) and frequency spectrum stands out in Starlink’s trade-off between the constraints of very low altitude transmission and the ambition of direct consumer coverage

According to SpaceX’s FCC request, as reported by Professor L. Press

- Low altitudes "will enable smaller spot beams and greater satellite diversity, achieving the intensive frequency reuse needed to heighten capacity available anywhere in the world"

- Low altitudes will allow SpaceX to use high E-band frequencies for communication with ground stations.

- Low altitudes will reduce latency.

While the LEO satellites, at altitudes of 1 100 km, will broadcast in spectral bands, which are typical for communications satellites (Ku and Ka bands), the ‘very low’ VLEO satellites will make use of the V-band, a higher frequency band ranging from 40 to 75 GHz and, according to the latest FCC request, also of the E-band (at a still higher frequency from 60 to 90 GHz)

Because the higher frequencies do not penetrate walls and becauses signals are further dampened by moisture in the atmosphere (subject to ‘rain fade’), these bands are only useful for line-of-sight applications - which is consistent with a direct-to-consumer model, such as Starlink's VSATs (very small aperture terminal ground stations)

On the positive side, the higher the frequency the less widely it will be used, resulting in less overall interference for the V- and E-bands

The dense network planned by SpaceX at very low altitude targets reduced latency and seeks to compensate poor signal transfer by multiple overlapping satellite orbits layered a few kilometers apart at low altitude

In beta-launch of its broadband service (Oct. ’20), SpaceX “expected to see data speeds vary from 50Mbps to 150Mbps and latency from 20ms to 40ms over the next several months as we enhance the Starlink system….”

With further improvement in sight, and if demonstrated, performance will be judged quite acceptable for underserved rural areas and for Arctic (military) coverage, for which SpaceX benefits from federal support ($1billion over years)

However, the density of coverage at very low altitude raises concerns from all parties, from astronomers fearing for degraded space observations and from environmental lobbies pointing ‘burn-up’ rate of aluminum satellites in the atmosphere and to ‘orbital debris’ mitigation

Push-back from established networks (such as Telesat, ViaSat

An array of novel issues, from technical feasiblity of SpaceX's large fleet to quality of the feed (latency of signal transfer) and actual cost to the consumer - a competition set against the background of growing specialized data demand which may be the true prize

Constellations – a race in space

Undisputed frontrunner with 951 satellites in orbit as of end of January ’21, SpaceX could be expected to contend with competition

The challenge is not without its ambiguities because Starlink’s consumer services do not necessarily align with the business services of established (or novel) satellite services

Amongst key contenders

Amazon

J. Bezos’ Blue Origin initially proposed a constellation of 140 satellites operating in the Ku band (frequencies in the 12 to 18 GHz range), to offer, according to FCC ‘Nov.15, 2018 approval, global connectivity for the Internet of Things, especially sensors and other intelligent devices

Not to be outdone by Starlink, Amazon

FCC filings in April 2019 lay out a plan to put 3,236 satellites in low Earth orbit — including 784 satellites at an altitude of 367 miles (590 km); 1,296 satellites at a height of 379 miles (610 km); and 1,156 satellites in 391-miles (630-km) orbits

Not altogether different from the Starlink project at the time (April ’19), it is not unlikely that ‘Project Kuiper’ will encounter the technical challenges which led its competitor to plan for a coverage density multiplied by a factor of 5 in the May ’20 request

How many of these dense orbits at very low altitude could operate without incident is unknown

Neither has Amazon yet publicly acknowledged its business purposes

Telesat Canada

Telesat of Canada, supported by a CAD 600 million grant (Nov. ’20) to deliver broadband in Canada’s rural areas, already provides Internet-connectivity to its customers via its fleet of 16 geostationary satellites and announced Feb. 2021 that Thales Alenia Space was selected to manufacture 298 satellites for a broadband network in low-Earth orbit (with a non-exclusive agreement to rely on Blue Origin’s launch services)

Notably, Telesat positioned its target markets as network operators, internet service providers, the maritime industry and governments, as a business to business provider, and not consumer broadband

Relying on optical inter-satellite link technology in orbit to rout traffic all over the world, the Telesat network intends to mesh with networks in low-Earth orbit, such as U.S. DARPA and the Space Development Agency

Telesat’s merger with Loral Space & Communications Invalid tag asset, announced in November ’20 and subject to review, offers valuable insights about the business services, currently delivered or still on the drawing board, delivered by satellite broadband – a rich seam discussed in a forthcoming report

OneWeb

OneWeb had its ambitions curtailed when Softbank

The company exited bankruptcy in Nov. ’20 under new ownership lead by the UK and Indian telecom Bharti Globlal, each contributing $500 million to the acquisition

As reported on nasaspaceflight.com, “the U.K. Space Agency (UKSA) reviewed the technical aspects of the deal prior to investment and stated it had “substantial technical and operational hurdles,” with additional concerns raised that the large risks in the project meant it did not meet the government’s criteria for return on investment. In particular, the different interests between Bharti Enterprises and the U.K. government were noted”

Overriding concerns expressed by the Agency, the acquisition by the British government has been questioned for heightening expectations of irreconcilable goals

The replacement of the Galileo System, the European GPS seemed to confuse national independence with technological realities

- the European global navigation satellite system went live in 2016 and was fully deployed with 30 satellites in 2020 – over-budget (€7.2 billion), well behind schedule (with initial target date 2008) and with operational costs of €3 billion

- with its departure from the Union, the UK was excluded from large parts of the system, notably the resilient secure communications aspects as well as defense (the encrypted part designed to guide missiles and plan military operations)

With the UK space industry at odds, the project was quickly shelved in September ’20, under the - apparently meaningless - assumption that “companies were to put forward “innovative” solutions that give the U.K. additional resilience to that of Galileo and GPS, the U.S. satellite navigation system”

The second goal of securing broadband coverage in underserved areas that lack the infrastructure for Internet connections is essentially what OneWeb was conceived for and, presumably, what attracted the interest of the UK’s co-investor, India's Bharti

Whether an additional LEO or VLEO constellation would be a valuable addition to the networks planned by Starlink, by Amazon and by other broadband providers, or more probably a competitive alternative to US dominance is unclear

OneWeb resumed operations, launching 36 satellites in Dec. ’20, using a Soyuz rocket launched from the Vostochny Cosmodrome in eastern Russia – bringing total satellites in operation to 110 – intent on implementing the current FCC allocation of 648 satellites by 2022

Priorities will probably be clarified over time as OneWeb reviews its FCC filings

- In late May 2020, OneWeb filed an application to the Federal Communications Commission (FCC) to increase the number of satellites to 48,000 in a ‘Phase Two’, despite the bankruptcy process (presumably because its prospective future owners, the UK and Bharti Enterprises wanted to vastly increase the constellation from the 648 satellites authorized in the initial round)

- The FCC response in August 2020 granted an application up to 1,280 satellites adding strong reservations regarding orbital debris mitigation

- In January ’21, in a filing with the Federal Communications Commission (FCC), OneWeb modified its ‘Phase Two’ approach, resetting its request to 6,372 satellites at the FCC which still has authority over the system after the change of ownership as the satellites are built in the U.S. and in which the constellation’s frequencies will be used

The firms discussed in our note, OneWeb, SpaceX, Telesat and Amazon are preparing thousands of small satellites bound for low Earth orbit in the hope of delivering high-speed, low-latency internet; underserved parts of the planet are likely to benefit but the ability to stream huge quantities of data will be a real game changer if - and when - new data-hungry applications emerge

Operators, like Echostar-owned Hughes

Banking on the scale and power of very high throughput satellites (HTS) to drive down the cost to deliver each megabit and betting on flexibility of technological advance in smaller geostationay satellites, these legacy operators are very much in the competitive game

Our follow-up notes will discuss the strategies of geostationary operators, the fast-evolving technologies of base stations and antennas and the way data needs to be understood in the computational shell to which we referred in the intrduction to this report