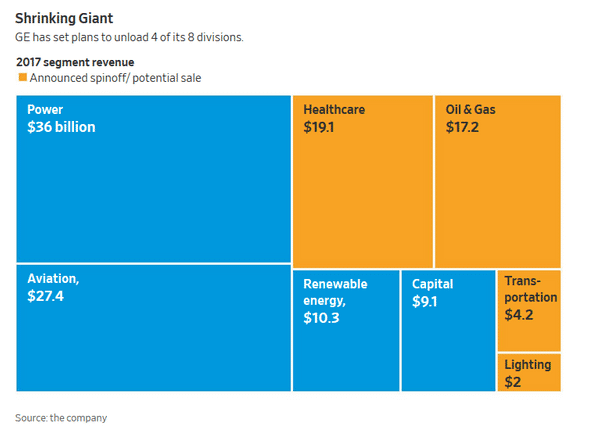

The June 26 ‘18 announced break-up plan of General Electric

Targeting a debt/EBITDA ratio below 2.5 times, as recommended in a April 25th Moody’s note in view of a potential ratings upgrade, may well have constrained the options GE management held under consideration

The harsh implication, not only for General Electric but for all indebted industrial groups, is that financing of capital-heavy cyclical business with low-cost debt is off the table in the years to come

In a sense, GE’s strategic choices anticipate a world of rising interest rates and will be discussed more extensively in pininfos analytics

Baker Hughes – General Electric

The Feb 21 ’18 GE announcement that its $20bn stake in the oil services and technology partnership would not be sold before 2019 has been followed in the June 26 break-up plan by GE's decision to withdraw from the partnership , in which the company holds a 62.5% share

In retrospect, both the strategic reasoning and the execution of the merger of the oil service company with GE energy assets come under unforgiving light

Strategy announcements were initially well received

Committed to technology investment, even through cyclical downturns, Baker Hughes' main focus has been on complex projects in international markets (representing around 80% of revenue).

In pressure pumping (fracking), investments are expected to grow at 15-20% in 2018 in the US but, with the business becoming a more commoditized service, the company maintained a conservative 3d place, behind Halliburton (n°1)

The strategy devised by General Electric could well have upended the competitive landscape with a ‘full stream’ capability defined as such on the company website :

“Our fullstream portfolio of products and services enables us to deliver unparalleled levels of industrial yield through technology, service, integrated offerings and commercial models”

This should be understood as a full-fledged integration according to the company presentation - from upstream (drilling, evaluation, production & subsea) to midstream (LNG, pipeline & storage) to downstream (refining, petrochemical & fertilizer) and even industrial (power & renewables, control & sensing

Our follow-up note will discuss to the industrial reality of this approach but, in preparation of this discussion, the segment information of BHGE provided on Form 10-K (2017) highlights revenue and profitability distribution in the partnership

BHGE - Segment Information

Segments are identified as Oilfield Services (OFS), Oilfield Equipment (OFE), Turbomachinery & Process Solutions (TPS) and Digital Solutions (DS)

TPS is of special importance for downstream chemical applications, including processing, water treatment and finished product quality challenges in petroleum refining; the division also provides turnkey power solutions and equipment for mechanical-drive, compression and power-generation applications

TPS is unquestionably at the heart of BHGE as a unique oil services and equipment company

The numbers bear this out – although, for lack of segment information on still alone-standing Baker Hughes (BHI) for the 1st semester 2017, we assigned all of BHI revenue and operational income for the period to the Oil Services segment (which may unintentionally inflate its weight)

| (in millions USD) | BHI in OFS Sem.1/17 | BHGE segments 2017 | |||||

| Revenue | OFS | 4662 | 5851 | 10513 | 48% | ||

| OFE | 2637 | 12% | |||||

| TPS | 6463 | 29% | |||||

| DS | 2309 | 11% | |||||

| 21922 | |||||||

| (in millions USD) | BHI in OFS Sem.1/17 | BHGE segments 2017 | before costs and corporate | ||||

| Op.Income | OFS | 111 | 71 | 182 | 13% | ||

| (non GAAP) | OFE | 38 | 3% | ||||

| TPS | 853 | 61% | |||||

| DS | 333 | 24% | |||||

| 1406 | |||||||

| Costs relate to impairment of inventory & restructuring and merger costs | |||||||

Source - pininvest analysis based on BHGE form 10-K (2017) - note 15 and reconciliation GAAP measures

Segment analysis for 2017 could support the argument in favor of an industrial portfolio strategy as turbomachinery and digital services balances poor oil field services in the down cycle

Alternatively, the point could be that BHGE is basically an oilfield service company (Baker Hughes) with equipment companies (GE divisions) bolted on but not really integrated

Our follow-up report will discuss the complexities of splitting oil services from the conglomerate