Pin-insights

Tripling from 6.76 million cars in 2008 to an est. 21.48 million in 2018, China car sales - and production - are a major driving force of the country's economy and represent 30% of the world market

With the radical shift in market shares around the world, the traditional export model - especially from Germany and Japan - is under fire

New alliances between unusual partners are brought forward by the technological tsunami of electrical mobility

Away with the old - and the weaker players ... it will not be easy

******

OICA, the International Organization of Motor Vehicle Association estimates that

- worldwide, more than eight million people are directly required in making the vehicles and the parts that go into them (5% of total manufacturing employment)

- about five times more are employed indirectly in related manufacturing and service provision,

- such that an estimated more than 50 million people earn their living from cars, trucks, buses and coaches

Although the OICA 2005 jobs data would need to be updated, the size of the workforce is keeping the industry at the center of national industrial attention

But worldwide expansion of the industry has been reducing national interests to local cogs of integrated supply chains

Globalization is bound to come to a head with country policies

- strong exporters (Japan, Germany) are confronted by importers looking for ways to maintain their industrial base, foremost in the United States

- in even starker contrast, trade within a broad economic zone will fall in line with national country policies - trade between zones, such as Europe and America, could easily flame out

This tense context is building up and the US skirmishes with the German - and possibly the Japanese - car exporters foreshadow harsher realities

Trade policies negating decade-old industrial strategies create uncertainty and a clear-eyed view of the changing landscape for both mature markets and emerging challengers seems to be the way to go

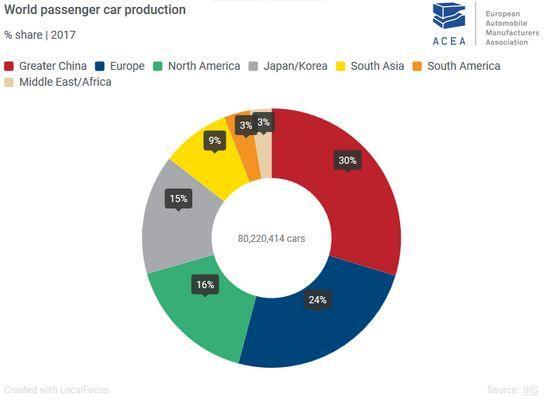

The fast lane - passenger cars worldwide

Over 12 months 2017, world production of passenger cars slighthly exceeded 80 million units

China’s share was 30%, compared to the European Union (22%), global Europe incl. non EU countries (24% ), the US and Japan (both around 10%) and India and South Korea (around 5%) – all rounded numbers

As of June 2018, global production has been 40.5 million passenger cars (over 6 months) - growing at 2.2%

Annual production is expected to remain unchanged in 2018, slightly above 80 million units

Market shares in global production shifted in the first half of 2018 (ACEA - EU Automotive Industry - Quarter 2 - 2018 page 12, published in October '18)

- Europe solid - at 25.4% (registrations 24.5%)

- North America - stable - at 16.7% (registrations 20.6%)

- Asia - dropping to 51.9% (against 53% in 2017)

- China, still growing in volume, fell to 28% in global market share (registrations 28.4%)

- India grew to 5.1% (registrations 4.5%), Japan remained stable in volume (down to 10.1% in share) and South Korea lost ground (4.6%)

The trend will need to be confirmed with full year data

The comparison of production and registrations is informative

- Europe maintains its position of global exporter (450 000 units through June '18)

- Germany, unsurprisingly, leads with production exceeding registration by 900 000 units (32% of 6-months production)

- North America remains the world's main import engine with a gap of close to 1.6 milion units between registrations and production

- Import by the United States draw an even starker contrast, since both Canada and Mexico are car exporters - with registrations surpasssing production by 2.8 million cars between Jan. and June '18

- China is not a factor on the export market, with registration exceeding production by 116 000 units - on balance, China's vast car market is self-sufficient, by itself a huge achievement

- The Japan car industry relies vastly on exports, with production exceeding registration by 1.8 million units (and 45% of 6-months '18 production of 4.1 million cars)

- India is positioned to export (although registrations are growing very fast)

These comments will be reevaluated over time, with complete 2018 data

Partnerships to meet the global challenge

We assert that factory locations and global strategies of the car manufacturers are setting the stage for a reckoning, a few years down the road

- The US car market has been restructured over time - relocating production for part in Mexico and part in China. The recent plant closures announced by GM

(moth-balling 5 factories, employing 15 000 personnel or about 15 % of total work force) and Ford (considering similar measures, laying off at least 20 000 people, representing 12% of its workforce) are brutal by any standard - China, for reasons we will discuss in our follow-up report on the country, has a production capacity estimated at 43 million, according to consulting firm PwC quoted by WSJ (paywall) for actual production and sales of 28 million, a looming threat for overbuilt Europe

- Europe, with 15% of world manufacturing capacity (not actual production), is expected to loose 2/3 of its market share by 2030, reducing production to 6.1 million units (from close to 18 million today) according to a 2018 study by KPMG (page 15)

As KPMG is careful to point out, the projections rely on current forecasts, presumably based on China's growing potential in export markets, and on Europe's mature consumer market and reluctance to restructure in the face of substantial unemployment in France, Spain and Italy

The magnitude of the risks tearing at the fabric of European societies will call - urgently - for alternative solutions; with bombast, the US trade strategies may actually show the way by inciting their domestic firms to regain a competitive edge

We will argue in our follow-up notes, that the technological revolutions, which challenge all legacy car manufacturers, may actually point the way

- with new technology, the break-up of the traditional manufacturing supply chain is pushed to extremes - part vehicle, part battery, part connected data base

- development costs, and the meshing of software with the familiar car assembly, is conducive to unusual partnerships, both with direct competitors to share the expense and with software start-ups

- the technological choices are not as assured as the media would like to assume - environmental-friendly mobility will remain a diverse menu, inducive to more collaboration in research between car competitors

- upstream data connectivity remains familiar, providing more and more reliable information on car performance and pitfalls, favoring the mass car producers by the numbers

- downstream data connections are expected to open a trove of the additional services, many of which still wait to be invented ...

Self-driving, a popular meme of the Silicon Valley crowd, is not as central to close partnerships within the industry, at least not in the medium term

The technologies remain to be proven and while the solutions may turn out to be relevant for mass transit in reserved lanes, their roll-out on the existing road system appears in doubt, and improbable in the near future

The forceful push towards cooperation is more likely to come from shared electrical vehicles assembly lines, battery research and production facilities, alternative new-energy solutions and significantly, partnerships with the software industry

Technology is transforming the product, the car delivered to the consumer's specifications, the everyday driving experience and the services attached to mobility and renews the challenge of building brand awareness

How the legacy firms will tackle these very novel opportunities will be discussed in our follow-up reports on the US market, on European car manufacturers and... on China