Pin-indices

The semi-conductor equipment industry is of special interest for the deep bench of technological expertise of companies which accompanied - and anticipated - the requirements for ever more powerful chips

But the balance between the equipment makers and the semi-conductor industry is exposed to deep changes with technological shifts in lithography, a key constituent for chip miniaturization, and because of unpredictable governmental interference commanded by national interests

An unusual disruption, making possibly some equipment manufacturers more valuable, but the exposure to potential losses in Chinese market share would impact the mainly US-based industry negatively

****

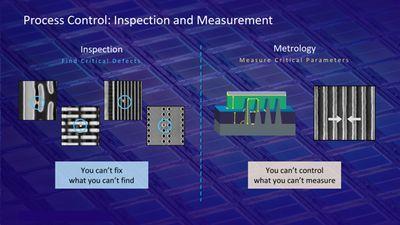

The semiconductor production process is divided into front-end production, in which circuits are formed on wafers and inspected, and back-end production, in which the wafers are cut into chips, assembled and inspected again

Wafer fab equipment (WFE), used in front-end production, refers to the deposition and etch equipment and to the more advanced extreme ultraviolet (EUV) lithography, a promising next-generation lithography technique

With improved lithography processes, chip designs can be made more complex and more – and smaller – transistors fitted on the chips, a miniaturization for more powerful chips and for increased memory capacity

Metrology & inspection equipment systems control the manufacturing process from front to back

To maximize yield and quality, process systems have been relying on

- sampling wafers for statistical control

- design rules which are geometric and connectivity restrictions in chip-design, specifying sufficient margins to account for variability in semiconductor manufacturing

Standard controls have remained quite effective down to a 28nm process technology but with further miniaturization, and innovative design architectures (such as 3D finFET transistors, 3D NAND, advanced self-aligned multiple patterning), the complexity of inter-connections deprives design rules of the built-in margin of flexibility

With more restrictive design rules, allowing for less manufacturing flexibility, yield becomes more sensitive to the size and density of defect, with potential consequences on manufacturing cost

A large act and a small number of players

The manufacturing process and the inspections have led the equipment makers to compete for the entire sequence of production, from fabrication to testing and packaging

But the unique structure of the semi-conductor market, with a very small number of equipment manufacturers and an equally limited number of clients, the sizable semi-conductor producers, has been a factor of specialization of the equipment manufacturers

- the production lines of semi-conductor companies have tended to favor ‘best-of-breed’ well established specialists, at every step

Chip miniaturization and complexity of design architecture further raise barriers to entry, effectively forcing the equipment providers and their clients, the semi-conductor manufacturers

- to specialize

- to interact closely in advancing R&D, with the partnership in EUV lithography a case in point

In effect, 4 wafer fab equipment manufacturers have a 70% market share

- Applied Materials

(approx. 18%) - ASML

(approx. 18%) - Lam Research

(approx. 16.5%) - Tokyo Electron

(approx. 16.5%)

For metrology and inspection, specialization is even more marked with 70% for 2 companies

- KLA Tencor

(approx. 50%) - Applied Materials

(approx. 20%) - Followed by Hitachi HiTech (10%) and ASML/HMI

A Nash equilibrium exposed ?

From Wikipedia, in terms of game theory, if each player has chosen a strategy, and no player can benefit by changing strategies while the other players keep theirs unchanged, then the current set of strategy choices and their corresponding payoffs constitutes a Nash equilibrium

A convincing case can be made for providers of semi-conductor manufacturing equipment because the demand of the end products – memory and logic chips – grows unabated, with the Internet of Things and automotive demand the latest frontiers …

In sync with equipment manufacturers, the strategy of equipment buyers – the semi-conductor industry – is reliably predictable

- to keep in step with the end-user demand

- to stay abreast of technological challenges

The interaction of these factors does not preclude volatility because end-user demand is highly sensitive to technological advance and anticipation of new applications

Semi-conductor producers – especially in the memory segment, as discussed in our dedicated series – have been keen to manage volume output, as has been the case since mid-2018 with slowing sales of smartphones and excessive stock built-up by data center clients

More predictable capex projections by the industry will, to a large extent, carry demand volatility over to the equipment manufacturers

But, while the swings in global orders are certainly very large, the actual sales of the leading equipment manufacturers, possibly smoothing sizable orders over time, do not reflect a similar volatiliy

With a clear path marked out from equipment manufacturer to end-user demand, the current set of strategies suggests a stable equilibrium

The investor might consider the factors that could eventually upset the balance

Nash spoilers - technology and geopolitics

Miniaturization of transistors (shrinking technology nodes) as Moore's Law progresses and applications for ever more powerful chips have always been incentives to invest in R&D

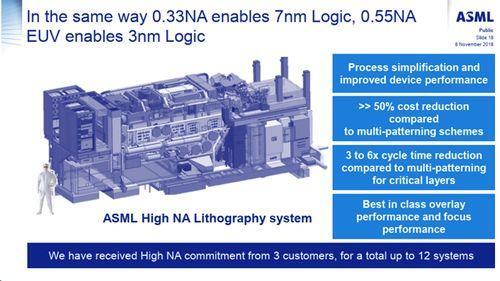

With lithography a key part of the chip manufacturing process, EUV lithography (extended ultraviolet), developed by ASML

- Samsung Electronics, TSMC

and Intel (together representing about 50% of total semi-conductor sales) have committed around €1.38 billion in cash to ASML's R&D in the framework of the Customer Co-Investment Program (CCIP) in July 2012 and continue to invest in the entire ecosystem involved in building the EUV infrastructure - In 2018, 18 EUV systems were shipped by ASML and shipments are expected to be of 30 systems in 2019, 33 in 2020, 45 in 2021 and 50 in 2022

Speed and rate of EUV adoption remains uncertain but will be critical, both for potential clients and for providers of current lithography tools

All in all, technology is a game-changer : with strategies of competing equipment providers out of balance from 2019 on, a dimension on instability must be reckoned with...

If technological advance remains a gambit, the geopolitics of trade could become another game-changer with still unforeseeable implications

From the difficult negotiations around intellectual property between the US and China, the concept of foundational technology has emerged a guiding principle

As discussed in R&D – an elusive genie, technology will continue to spread and the benefits of any break-through can at best be protected for a time by controlling dissemination

In the all-important sector of semi-conductors, the largest Chinese import segment dominated by US firms, the concept of foundational technologies has found favor with US negotiators as choking points, establishing the incontrovertible position of American companies in foreign - especially Chinese - supply chains

With the semi-conductor equipment manufacturers, the contradictions between governmental policy and commercial sales growth targets are coming to a head

In terms of US policy, the equipment manufacturers find themselves at the forefront of a sanctions-driven policy as we will discuss in our forthcoming semi-conductor note ‘Unpacking foundational tech’

- The number of competing companies is small and, with few exceptions, US-based, facilitating regulatory implementation

- The number of production lines is well known, and new annual sales is effectively small as well, a guarantee of effective control

- The technological input, necessary training on the production line and follow-up services are barriers to entry, protective of IP theft

In terms of company strategies, aiming for growth, China has become a key market since 2016, the year multiple plans for domestic semi-conductor production came to fruition, and the equipment makers all emphasize how China is emerging as a major region for chip manufacturing

The sales jump of 2016 bears this out (all numbers excerpted from 2017 annual reports)

- Applied Material + 39% (2016/2015) and + 22% (2017/2016) - 19% of total sales in 2017

- Lam Research +57% (2016/2015) and stable from 2016 to 2017 - 13% of total sales in 2017

- ASML +43% (2016/2015) and +18% (2017/2016) - 10% of total sales in 2017

- KLA-Tencor – 4% (2016/2015) and + 56% (2017/2016) – 16% of total sales in 2017 – the time lag in metrology and inspection equipment pointing to the fact production lines bought in 2016 were installed the next year

As Lam Research states in the 2017 annual report (p.91), ‘there is inherent risk, based on the complex relationships among China, Japan, Korea, Taiwan, and the United States, that political and diplomatic influences might lead to trade disruptions’

Indeed… and the equipment manufacturers have been confronted with geopolitical realities in late 2018 when the installation on site at Fujian Jinhua, a semi-conductor company established in 2016 for the manufacturing of memory chips – at a cost estimated at $6 billion – was called off by the US authorities following the indictment of Jinhua’s Taiwan partners, a case we will discuss in detail in our note ‘Tackling the Chinese offensive’

With pro-active interference of the US Trade Representative following indictments by the US Department of Justice of Jinhua partners, the decision signals how sales opportunities in China may be at risk

In this context,

- actual sales growth potential of US companies in China should probably be discounted because of geopolitical constraints

- ASML, a Dutch company with a large footprint in the US, might be similarly exposed, as we discuss in our forthcoming note 'ASML's ultra violet future'

- Tokyo Electron

a Japanese provider, might need to weigh its options – and possibly reconsider its May ‘18 optimistic projection of 30% WFE sales in China by 2020, based on the planning of 10 to 15 new semi-conductor plants in the country

Next to technological shifts, national interest will not simply be a potential risk to sales targets but an active component of business strategies, with stakes no company can ignore

It is not obvious that the equity market has recognized how trade tensions have become a reality in the long haul, impacting with immediacy the foundational technologies as we have seen

A Nash equilibrium belongs truly to the past and share prices will need to adjust