In our 2 recent notes about US international trade we discussed the complex interaction between the current account (recording trade in goods and services) and the capital account (recording financial flows in and out of the country) in the balance of payments

Our purpose was twofold

- To show how the accounts have to balance, a current account deficit has to be financed and a capital surplus flowing into the country has to be allocated

- To demonstrate how the status of a reserve currency reverses the causality relation between the 2 accounts

Making sense of a capital surplus

By definition, a capital surplus in the form of borrowing on foreign markets will balance an excess of imported goods and services over exports. And this can go on for a while, with the unfortunate consequence of building a sizable position in liabilities in foreign currencies in the financial system of the foreign market

And ‘for a while’ does not mean ‘forever’… because at some point the foreign lenders will reclaim their financial stake, whatever the nature of the asset (direct investment in the country, lending to the domestic banking system or to the Treasury), and they will reclaim their due in the original foreign currency

However, the relation from cause (a trade deficit) to effect (‘import’ foreign cash) is not the same for a country endowed with a reserve currency, namely the US dollar

Foreign entities – businesses, banks or State treasuries – will want to hold on to the reserve currency for any number of reasons (to finance imports quoted in US dollars at a later date, to satisfy reserve obligations or to strengthen foreign currency positions as insurance against future balance of payment crises…)

The end result is to push the US capital account into ever larger surpluses, which is not a domestice policy goal if foreign direct investment takes over American business or foreign holdings of US Treasury bonds start to dominate

If the status of reserve currency is a gift that keeps on giving

- because the surplus countries deposit their dollar funds in the American system as a way of clearing their excess holdings, the surplus capital account is an important (and maybe the main) driver in the complicated interaction with the current trade account, private savings and the Government budget

it is a gift with a sting, for polar opposite reasons

- because fund allocation within the US can take any form, essentially out of the scope of the monetary authorities, buying hard assets in long term investment or short maturity T-Bills, at the behest of the foreign entities

- because domestic monetary and fiscal policies can and will have an impact on the liquidity of the US dollar on the international market, reverberating throughout the world economy

Financing the international trade

Partially planned, partially by taking on a life of its own, the US dollar became the single most important vehicle of global finance

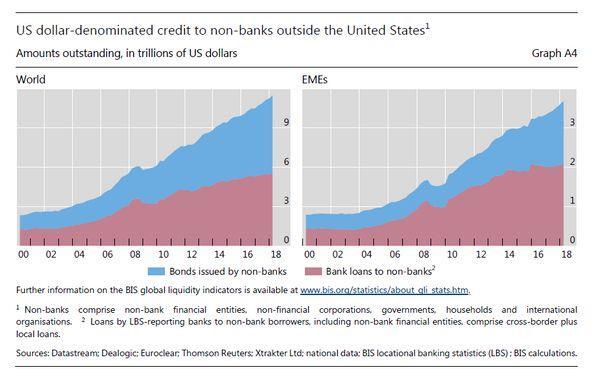

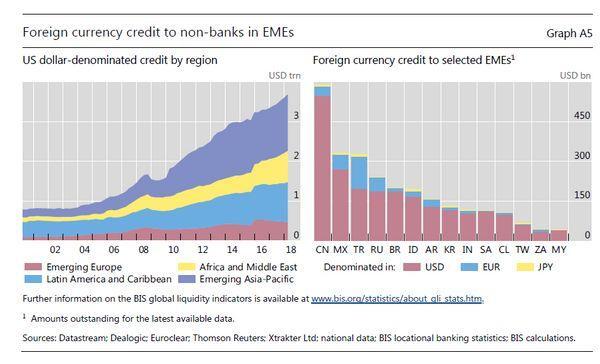

The awesome size of the US-dollar denominated credit to non-banks - estimated by the Bank for Internalonal Settlements at $11.5 trillion (March '18) - overshadows the fact US monetary authorities have little control over the market which exists outside the US boundaries, between non-US lenders and borrowers...

In the old days (of the 1960’s), a ‘euro-dollar’ financial market was initiated to lend and borrow US dollars between non-US residents, outside the US financial system and, at the time, the chronic US deficit related to the Vietnam war flooded the international markets with ever more dollars seeking favorable terms of investment

This wholesale market in money was created at the behest of the international banking system (non-US banks and foreign subsidiaries of US banks) which went on a mission to recycle ‘free floating’ dollars and a major business line was born…bringing together deficit-heavy countries, growing international businesses and banks happy to ‘intermediate’ (borrowing on the international market and lending to the hungry masses…)

In an ideal world, this is how things were expected to unfold

- Countries in deficit address the structural reforms to rebalance their accounts over time

- International banks, backed up by sovereign states as ‘too-big-to-fail’ or as ‘national champions’ (or usually for both reasons), enjoy attractive borrowing rates with a pool of collateral at hand, and lend at attractive terms

- And, importantly, ever more free floating hard currencies (usually dollars) are readily available to keep the merry-go-around recycling business on the road

This is how things might have run, smoothly for a (little) while, as inherent agency dilemmas were superseded by global growth

- Great for politicians of all stripes, vaunting better jobs for their electoral base and more cash to spend on gimmicks, as long as it lasts

- Great for business, launching ever more ambitious projects to partake in a globalized market

As long as it lasts.... because agency dilemmas galore mirror the unfettered access to international finance, without direct central bank interference

- while the international market assumes liquidity to be available, ensuring smooth roll-over of credit lines, US monetary authorities will prioritize domestic policies which may - or may not - constrain international credit

- emerging markets on a credit-fueled growth path have repeatedly neglected the circuit breakers to stabilize finances tethered to US liabilities (the Latin American crisis of the 1990's, the Asian crisis of 1997 and more to come) - creating additional uncertainty in the global market

In our follow-up report, we will discuss how global trade finance might be affected

- by exchange rate sensitivity to US monetary policy changes

- by the significant dollar exposure of some emerging markets, creating a systemic risk