Whichever way we read the comments made by Mark Carney, the Governor of Bank of England on 23 May ’18 at the Society of Professional Economists, London, the findings are dire

- Sterling remains some 15% below its late-2015 peak

- Inflation rose well above the 2% target, peaking at 3.1% late last year (2017)

- UK growth has dropped from the fastest to the slowest in the G7 and decelerating despite support from a much stronger-than-anticipated euro-area and global growth

All of which nails

- Potential BOE growth rate [estimate] to around 1.5%, about 60% of its pre-crisis average

And

- That diminished rate of supply growth reflects the climate of the past few years, with the shallowest investment recovery in over half a century, lower growth in labour supply and modest productivity growth

We take this to be a train wreck and the BOE’s carefully worded implications for the British economy should be of the deepest concern

- Referring to the diminishing rate of supply growth these ‘past few years’, Mr. Carney signals a structural weakness, possibly aggravated by Brexit but not caused by the decision to depart the Union

- Shallow investment recovery has been a noted feature of the drawn-out worldwide and financially engineered recovery muddle, leaving the UK a bit more exposed to the highly unfavorable consequences of a future recession

- If low growth in labor supply is a long term trend, the antagonistic stance focused on immigration as the source of all evils will make a bad situation worse

- Modest productivity growth, mentioned in passing in Mr. Carney’s speech, is in our view the nexus of today’s – tomorrow’s - Troubles

We will argue that productivity growth is indeed a long-term trend, beyond and before Brexit, and, though productivity growth may have been modestly encouraging in the second half of 2017, the broader picture is dismal

What makes these statistical observations most worrying is the lack of shared explanations of the lagging British performance. …Without a clear understanding, public policies are stumbling in the shadows….

Weak productivity growth seems to have become a lasting feature of the British landscape for so long – since 2007 to be specific – that its lasting impact on the economic health and wellbeing of businesses and consumers is taken for granted

This is quite wrong

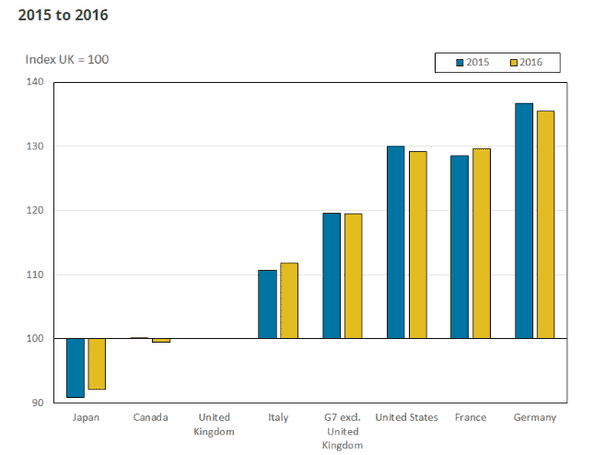

Of course, statisticians and economists are laser-focused on productivity measures and the chart published by the Office for National Statistics (last update April 2018) comparing 2015/2016 labor productivity across the G7 nations is worth a thousand words

In no uncertain terms, Great Britain is clinging to the bottom rung in terms of levels of and growth in gross domestic product (GDP) per hour worked and GDP per worker Only Japan's aging society is doing worse...

Quoting David Marsden, Deputy Governor (23 Feb. 2018 speech at Babraham Hall, Cambridge)

- Since 2008, business investment has been far below the recoveries the UK experienced after the 1979 and 1990 recessions

- Around ten years after the global financial crisis, cumulative growth in business investment is still around 50 and 30 percentage points below where it was at the equivalent stage of the recoveries seen in the decades after the 1979 and 1990 recessions respectively

- The weakness of and uncertainty around the path of UK productivity is a key driver of these unusual developments, and is therefore a key consideration for monetary policy

Troubling as it is, the lack of clear causality is the real puzzle

In the view of Mr Marsden, global trends come first

Source : Chart 1.3 Inflation Report BOE February 2018

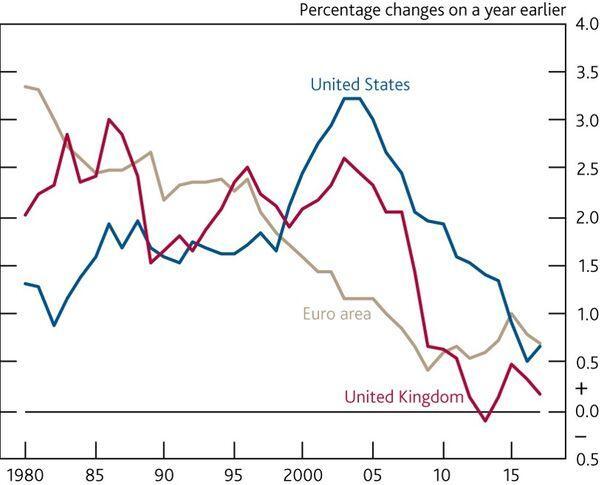

While indeed the slowdown in productivity is not unique to the UK but shared amongst advance economies, the brutal collapse observed since 2008 is extraordinary and the economy has not recovered since

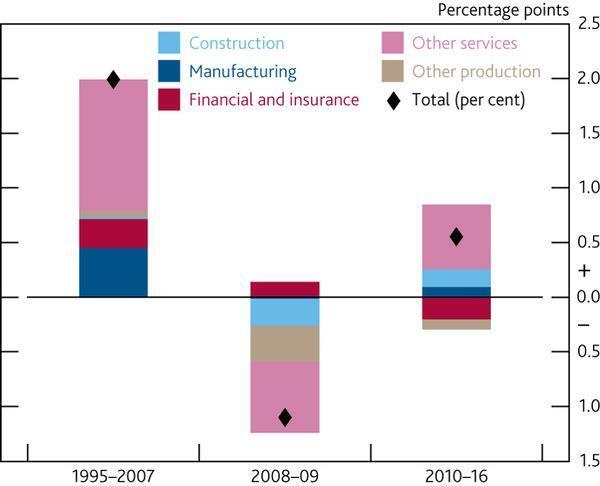

The second observation of Mr Marsden assigns productivity loss to key sectors

- The manufacturing and finance & insurance sectors made no contribution to average annual productivity growth in 2010-16. Pre-crisis, these sectors contributed around 0.75% to annual average productivity growth. So combined, they accounted for over half of the growth puzzle to 2016, despite employing only 11% of the workforce

Referring to chart 3.9 Inflation Report BOE February 2018, it does not appear satisfactory to combine two sectors with very different drivers since 2008

Source : Chart 3.9 Inflation Report BOE February 2018

Finance & Insurance has been the sole contributor to productivity growth (at about 50% of past contributions) in 2008-2009 while the contribution of manufacturing has been 0

However, over 2010-2016, finance has been a negative contributor to productivity growth, taking back about 80% of pre-crisis contributions, year after year…. Manufacturing has been a smallish contributor, at about 20% of the pre-crisis heyday

Mr Marsden cautions about pre-crisis comparisons, making an example of the finance sector

- Increased leverage and risk-taking with financial firms prior to the crisis is likely to have boosted measured productivity, beyond what was sustainable

We share the observation but we believe the comparison with pre-crisis data is in fact quite relevant because of clear causality – leverage and risk-taking, unsustainable profits and remunerations, and booming property boosted productivity measures but the fact is the good times will not come back – productivity contribution was a bubble, contribution of the finance sector was a mirage which dissolved before the eyes of Gordon Brown, shortly after his Comprehensive Spending Review of 2007

Thirdly, Mr Marsden singles out slow growth in capital per hour worked (known as capital deepening) seen as widespread across all sectors of the economy

Uncertainty (incl. post-Brexit) may indeed be a factor but to assume that because poor capital deepening is widespread, the cause – uncertainty – has to be shared across sectors sounds unconvincing

We call for expert contributions (we are not) in considered evaluations, sector by sector, reversing in some cases vague political mandates and laissez-faire with targeted industrial policies – attractive propositions with or without Brexit

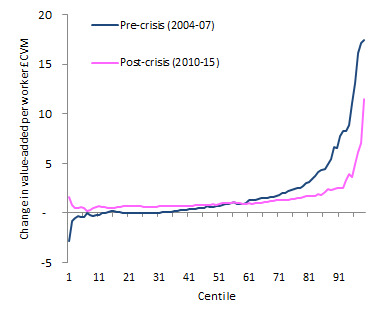

The fourth – and last – factor affecting UK productivity since the crisis is primarily related to slower growth of high-productivity companies

In a chart, published on the BOE / Underground blog (expressing views of the staff but not necessarily of the Bank itself), Patrick Schneider makes the case

Linking aggregate productivity to its distribution across workers, Mr. Schneider shows how the slowdown in productivity growth is isolated in the top tail

Comparing pre- and post-crisis productivity distribution, the charts highlight

- how one (or more) sectors at the top just fell away over the 2010-2015 period, leaving a much smaller segment of great productivity performers to ‘pull the truck’

- how at the bottom end of the productivity scheme, firms have been inching ahead, possibly small contributions but spread over the bottom 40% - numbers do – and could – add up over time

And Mr Schneider concludes

As with any statistical decomposition, we’re brought no closer to the why of the issue, but the where is a little clearer

This is true but, putting it all together, we believe there is a case to be made to assign to the finance & insurance sector, and to real estate, the sharp and enduring drop in productivity gross

If indeed the finance sector is inching towards a smaller – but more durable – contribution to the UK economy, this assumption confronts the Government (and the Opposition) with opportunities

- how to favor productive investment at the bottom 40 to 50% contributors

- how to identify and target effectively the very top contributors, whose importance has only grown as Finance takes a step back

Unwinding of Brexit is adding urgency to the issues, although Brexit is not the original driver