Pin-insights

For lack of a 'pro-active' competitive response by American industry to Chinese global expansion, a ‘trade war’ with China has in fact become unavoidable for the US Administration

To make the conflict more intractable, the real achievements of China's tech industry are forcing the US to adopt a defensive strategy of containment, regulating access to American know-how

With semi-conductors the cornerstone of tech advances, the equipment manufacturers of semi-conductors are in the line of sight of the trade negotiators

The small number of highly specialized firms - mostly US-based - qualified the industry as 'foundational'

How the leverage will play out remains an open question, but certainly one to be considered

****

As China and the US temper their trade differences, it remains difficult to evaluate the fall-out for the semiconductor industry and their equipment providers

There is no credible ground for resolving the fundamental differences between the two great world powers

In truth, the current trade differences hardly have the make-up of a ‘war’ – they are just skirmishes in a drawn-out conflict

To take what the country believes to be its rightful place at the head of the table, China is asserting its domination in world-class industries

For lack of a 'pro-active' competitive response by American industry, the ‘trade war’ has in fact become unavoidable for the US Administration

And to make the conflict more intractable, the real achievements of China's tech industry are forcing the US to adopt a defensive strategy of containment, regulating access to American know-how

Equipment manufacturers for semiconductors (selling to the chip makers, not the chip makers themselves), front and center of this line of defense, should be in a bind…

A barricade, really ?

In the Making of Semi-conductors, we observed that the equipment manufacturers find themselves at the forefront of a sanctions-driven policy, bringing to a head the contradictions between governmental policy and commercial sales growth targets

In terms of a US policy of containment

- the number of competing companies is small and, with few exceptions, US-based, facilitating regulatory implementation

- the number of production lines is well known, and new annual sales is effectively small as well, a guarantee of effective control

- the technological input, necessary training on the production line and follow-up services are barriers to entry, protective of IP theft

Geopolitical realities proved to have some teeths in late 2018

The installation of manufacturing equipment on site at Fujian Jinhua, a semi-conductor company established in 2016, was called off by the US authorities following the indictment of Jinhua’s Taiwan partners, commanding the departure within 24 hours of all the key providers US-based Applied Materials

However, the stock market will have none of it...

After hitting a low point along with the wider market by late December '18, share prices performed in line with the market - and beyond - in a range of +35% (ASML) and + 50% (LAM Research) as of this writing (April '19)

Are export controls flaming out ?

Full-year 2018 regional sales for semi-conductor manufacturing equipment, recently published by PR Newswire (April '19), surged 14% over 2017, on the back of very strong sales in China (+59%)

Presumably, China sales include equipment installed at the foreign subsidaries of major semi-conductor firms - Samsung, Intel, TSMC and others - but the run-up since 2017, when the same subsidiaries were present in China, points toward the fast expanding Chinese semi-conductor industry

| Region (in $bn) | 2018 | 2017 | % Change |

|---|---|---|---|

| South Korea | 17.71 | 17.95 | -1% |

| China | 13.11 | 8.23 | 59% |

| Taiwan | 10.17 | 11.49 | -12 |

| Japan | 9.47 | 6.49 | 46% |

| North America | 5.83 | 5.59 | 4% |

| Europe | 4.22 | 3.67 | 15% |

| Rest of World | 4.04 | 3.20 | 26% |

| Total | 64.53 | 56.62 | 14% |

| Source: SEMI (www.semi.org) and SEAJ, April 2019 | |||

China’s ambition to lead in advanced technologies (5G telecommunications networks, artificial intelligence, robotics, quantum computing….) are frankly and openly stated as a national cause

Vast investments have been pledged by central Chinese government and – according to The Information Network - by close to 2000 "government guidance funds”. In the semiconductor sector, 20 local governments have set up guidance funds with investment plans worth a combined $90 billion

The most advanced generations of semi-conductors are a pre-requisite for the ambitious ‘Made in China 2025’ program and domestic production capacity of the chips tops undoubtedly the agenda

In outfitting or upgrading their existing foundries, the Chinese semi-conductor manufacturers have no other options but to rely on the group of specialized equipment providers, led by Lam Research, Applied Materials and Tokyo Electron for deposition and etch equipment, by ASML for lithography and KLA Tencor for inspection

This uniquely small number of complementary foreign firms, enabling the development of a broad range of sectors relying on the global semi-conductor industry, are the indispensable partners of China’s technological ambition – a choke point or – as US trade strategists choose to rename the segment - ‘foundational technologies’

Going head to head

The confrontation of China's quest for self-reliance in all things and America's angst has singularly turned the tables in very few years

China is very aware of the fact that semi-conductors are the key to unlock expansion in yet-to-be-discovered fields and to establish the preeminence which the governing authorities hope to achieve in their life time

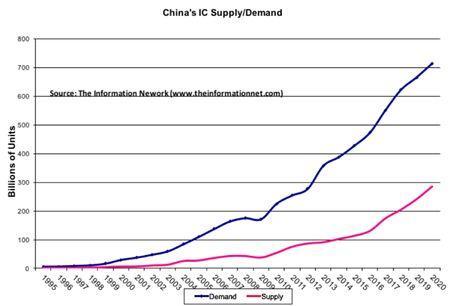

Imports of 417.57 billion integrated circuits at an import value of $312.06 billion (+19.8%) in 2018 concentrates the minds in China as the chart sourced from 'The Information Network' demonstrates, for 2018 and possibly for years to come

For the US negotiators, the temptation to slam on the breaks with export controls is probably a real option to align trade policy with national interests as the American awareness of China's outsized competition grows

From a laser-like focus on national security to the time lag needed to put American competitiveness back in order, the case could be easy to make

But the more profound issue raised by American efforts at containment of Chinese technology is likely to be the apparent inability of American – and more generally Western technology – to live up to the challenge, in terms of performance and price

Round after round, the trade negotiation between the US and China seems to be dead-locked on principles - effective protection of Intellectual Property (IP) and open market access for US firms - issues difficult to frame and more difficult still to control

But semi-conductor manufacturing equipment providers, as 'foundational' as they come, would have good reasons to dampen investor enthousiasm for over-the-top growth in China in 2019

It just may not happen that way