Natural gas is here to stay, environmental concerns notwithstanding

In the short term, the case of natural gas indispensability as energy source has been made by its sudden deprivation, courtesy of Gazprom, Russia's energy export giant

The infrastructures put in place to access liquid natural gas (LNG) delivered by sea, in replacement of pipelines linked to Russian gas fields, are medium-term investments, with 20-to-30 year horizons

By virtue of their cost and their ease of access, infrastructures will determine in part the future balance of energy sources around the world

Europe, where some of the strongest commitments to a "zero-carbon" future had been made, is in for a hard landing

Every member of the Union is already scrambling - investing in regaseification stations where needed (Germany, France, UK) and in new pipelines - and hoping to negotiate contracts, expected to be long-term, for delivery from a small band of providers (Qatar, US, Norway)

Because of the cooling process (to -160°) and the transport over long distance by ship, the LNG footprint is markedly higher than for piped gas (although average estimates are largely irrelevant because of the variability of the environmental performance of different technological solutions)

Over the medium-term, the argument for an energy mix, balancing renewables ( a source destined to grow over time), nuclear power and gas powered stations, seems to gain in credibility

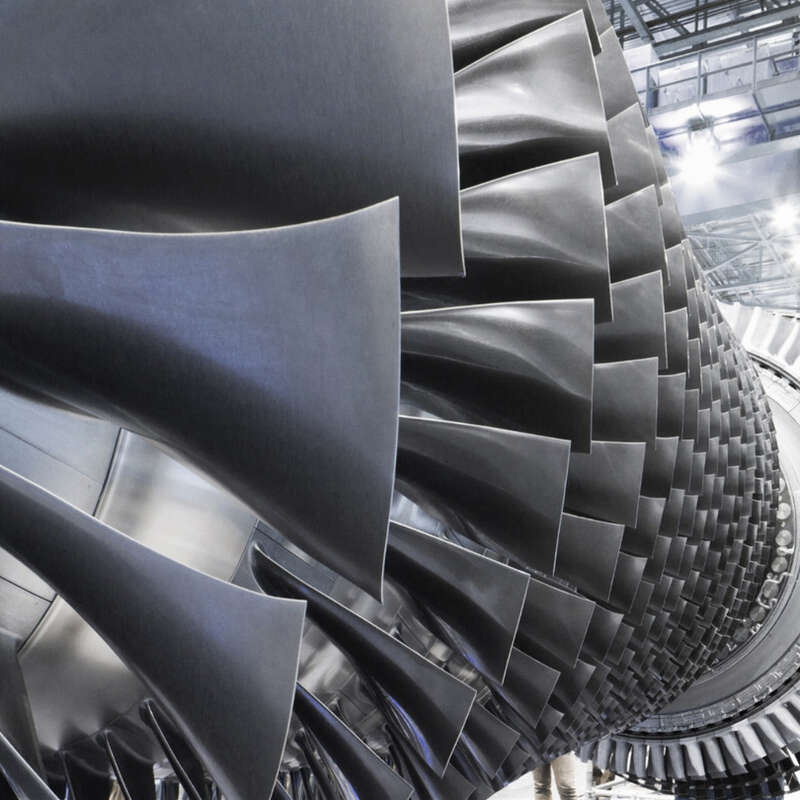

And one industry is decidedly convinced already, the manufacturers of heavy duty natural gas turbines, of large capacity (150-300 Mw), used in the power generation industry

The replacement of coal-driven turbines, the largest contributors to air pollution, by gas turbines might mitigate the necessary reliance on LNG by reducing greenhouse effects overall

In 2019, more than 2000 Gw capacity of coal-fired plants were in operation around the world, approx. 50% of which in China, according to Fortune Business Insights, a market ripe for replacements

And the trend for access to electricity is on the rise

The giant power companies - included in this selection - will benefit and in fact, already have

Check performance over very short time frames (2 weeks and 1 month)

Note -

Caterpillar is included on behalf of the firm's subsidiary - Solar Turbines

Doosan Heavy Industries (South Korea) and Bharat Heavy (India) are not listed in the US

Shanghai Elelctric is included as part-owner of Ansaldo Energia (Italy)