Pin-insights

In Apple's 'June Scorecard', we discussed the finally balanced quarterly results, with strong growth in the Services revenue segment a timely offset to sliding iPhone sales

Looking beyond quarter to quarter financial reports, the paramount importance of solid smartphone sales is obvious for many reasons, but essentially because the revenue derived from profitable hardware is the backbone of the company's marketing and distribution prowess

It may be argued that the smartphone market penetration is so vast and technological advances so consistent over the years that the shift from growth to replacement was foretold

The fact remains that the iPhone sliding sales and dropping market shares are worrisome, and it is ultimately for structural - and not cyclical - reasons

Not to put too fine a point on it, smartphone sales are Apple's core business and in a maturing market, the company's potential would be irreversably wounded by the loss of share on its key markets

Priorities are set and iPhone sales in each developed market remain front and center

***

Battening down the hatches

Although sales revenues, supported by the growth of Services, matter very much, two dimensions laying at the very foundation of Apple's

- Apple's supply chain has been a remarkable achievement, but the unique coherence and tight fit of an organization involving hundreds of suppliers may break down if volume orders are being dialed down quarter after quarter. In the stead of often cited Foxconn, listed as Hon Hai

, (about 50% turnover with Apple), many small suppliers may have neither the flexibility nor the profit margins to survive - As the competitive smartphone industry is catching up with the iPhone in terms of perceived value and technological innovation, the remarkable brand recognition of Apple's hardware, which stood out for years as the true driver of the company's market power, may be exposed

We imply that, if diversification in Services relies on the iPhone installed base, smartphone sales remain the fundamental driver

- Apple Services can hardly - in most cases - contribute to 'brand building' - Apple credit cards, after all, are just...credit cards

- the success of Services derives today from the trust of existing Apple clients - as seems to be the case already in China and in Europe where growing Services offset slowing iPhone sales

If the analysis proves correct, Apple's challenge is clearcut

- Stemming the bleeding of iPhone sales is paramount

- In the 'mix', some Services could align - and actually contribute to image building; they should be given priority at any cost

Reversing a lethal sales trend

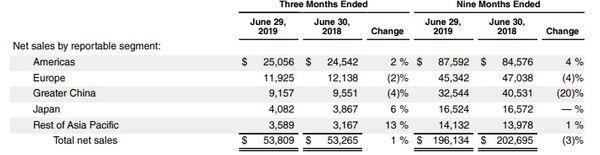

Holding its own in fairly weak markets since 9 months to June 2019, up 4% in sales in the Americas and down 4% in Europe, stable in Japan, the company has been affected by a sharp drop in China (down 20%)

The deadly brew of geopolitics and wild competition of Chinese phone brands portends diminishing sales in China in the months to come, compelling the company to take a stand in its core markets (the US, Europe and Japan)

The sensitivity of the issue is hardly a secret and goes a long way towards explaining Tim Cook's unusual decision to make a deal with Qualcomm

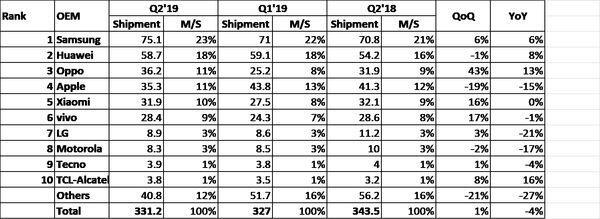

Holding its own in the US, according to Counterpoint research, a market share hovering at 40% is the company's greatest strength

Divergence between US market share and Apple's stake on the world markets against competing smartphone makers is striking

Banking a cumulative 48% for the top 4 Chinese firms and 26% for the top 2 South Koreans in the global market, the strong competitive showing is in no small part due to the limited attraction of Apple pricing on the emerging markets

On European markets, according to StatCounter, Apple is a significant n°2, with a 25% stake behind Samsung, but the presence of Huawei (17%) and Xiaomi (5%) calls for a European pro-active strategy

- There appears to be a significant discrepancy between StatCounter estimates and both IDC Markit and Canalys market analysis

- According to Canalys, Huawei holds a much larger market share at year-end 2018 of 23.6% (and not 17%)

- According to IDC, the 3 top Chinese phone markers (Huawei, Oppo and Transsion which dominates on the African market) reach 36.8% of EMEA region (Europe-Middle East - Africa) by the end of Q1-2019

If the market analysis proves to be correct (we would not know for sure), Apple might have to cast its playbook very differently to respond to the Chinese challenge on European markets

- The Service-focused strategy will extend across all developed markets but, with a focus on strong European themed Services, Apple might manage to reverse market share loss in the region and protect its 'installed' user base

- The iPhone price strategy - with the introduction of phone topping $ 1000 - is overreach, skimming a sliver of the market, which hardly contributes to maintain the user base. The pricing strategy of the forthcoming 5G iPhone series calls for a soul-searching overhaul

- By stretching convenient tax agreements with Ireland (where Apple's European subsidiaries are located) beyond breaking point, Apple's strategy of tax optimisation may prove to carry a high reputational cost (on top of the tax clawback of €13.1 billion plus interest). The company's insistence to be proved right in the European Courts flies in the face of the obvious fact that Apple products are sold across the countries of the Union

Seen through a distant lens in Cupertino, Europe presumably is viewed as an extension of the American market, with affluent consumers and a well-recognized brand name

This assumption might be flawed, considering the 2018 growth in shipments booked in Europe by Huawei (+55.7%) and by Xiaomi (+62%), according to Canalys (Feb. 2019 report)

- imprudent because Europe may be the setting where Chinese global ambitions confront American reputation, with dire consequences

- overbearing because Apple clearly signaled with its low-tax strategy that the company could somehow dispense with governmental rules and regulations across Europe

While growth in China will presumably be difficult for political reasons, and across the emerging markets equally modest because of product pricing, Apple's appeal on developed markets is real and the potential growth of Services in line with company strategy

The Japanese market is 'real-life' proof of Apple's overwhelming marketing power with a 56% market share in Q4-2018 according to Canalys and a 68.6% share (Statcounter globalStats). Interestingly, Huawei holds only a 6.4% share according to MM Research Institute but almost half of SIM-free sales (sold without carrier subscription) according to Japan Times, a venue to keep in focus

In Europe, where the pushback against Chinese market pressure is real and awareness is building, Apple could benefit... provided the company turns away from confrontational public persona to willing governmental associate

About time...

While a solid - and growing - iPhone user base is the key to the successful roll-out of Apple's strategy, Services should contribute to strengthen the perception in their own right - requiring complex arbitrage to engage with the trust setting the brand apart , as we hope to discuss in 'New Global is Local'