The "South-East Asia series" focuses on the region's largest countries - Indonesia - the Philippines - Vietnam - Malaysia - Thailand and Singapore - the SEA-5

- South-East Asia – a Multipolar Challenge

- South-East Asia – China's Geopolitics of Trade

- South-East Asia - US Trade - Rebalancing Blues

With a population of more than 650 million - and growing economic weight - these countries are in a pivotal position between the world's Great Powers, the US, China and India

Tensions in the region between the rival rainmakers, America and China, could harden their posture in head-on confrontations

Because such risks are beyond the control of South-Asian governments, they are compelled to seek balance on a transactional basis

Intent on keeping their options open, one deal and one commitment at a time, these governments might get leverage by virtue of their central location, their outsized population and their economic potential

The best possible outcome, peaceful growth spreading economic well-being across the region, will be a challenge for China as well as for the US. For both super-powers, it might also be an opportunity to project power in a paradigm shift

With SEA-5 countries keen to advance on their own terms, the Great Powers will not gain the influence they crave by throwing their weight around

Appreciation of these countries' fundamental interests, laying the groundwork of partnerships with each ASEAN member, could be a sea-change

A more complex network of relations may feel like a come-down for the US and China, eager to anchor their influence - respectively - on military security and economic overweight

Both contenders, however, may find new venues of influence by embracing flexibility in the exercise of power, set against clear-eyed and transparent structural goals

- fine-tuning public and private investment opportunities in line with each recipient country's interests

- favoring soft power strategies associating third countries best positioned, when and where the opportunity arises

Advocacy for versatility to soften the edges of confident American and Chinese power projections is not straightforward...

Multiple bridges built across South-East Asia will not elevate the clear 'winner' of a bipolar world

But then...a multipolar world never promised as much

Foreign direct investments (FDI) will be received with wariness in developing countries

Under the umbrella of (US) military alliances, the trade-off can be ambiguous, even with unquestionable positive economic fallout - suspicion will hang over investments that the dice are loaded to benefit the American firms...

Chinese supply chains, pushing for deep integration, may barge in on less advanced economies in the region and the tendency to transfer value downstream (in China) is a familiar and cautionary tale

Either way, investments by China and by the US may be too unevenly allocated and rarely balanced to achieve equal partnerships

A restriction for now... but essentially an opportunity for redress

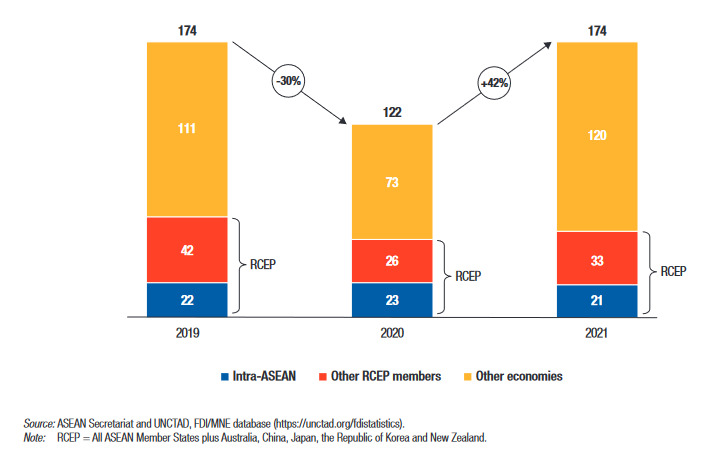

Foreign direct investment in ASEAN

Foreign direct investment (FDI) flows to ASEAN countries surged 42% to $174 billion in 2021, rebounding to the record reached in 2019 before the COVID-19 pandemic dragged down investment

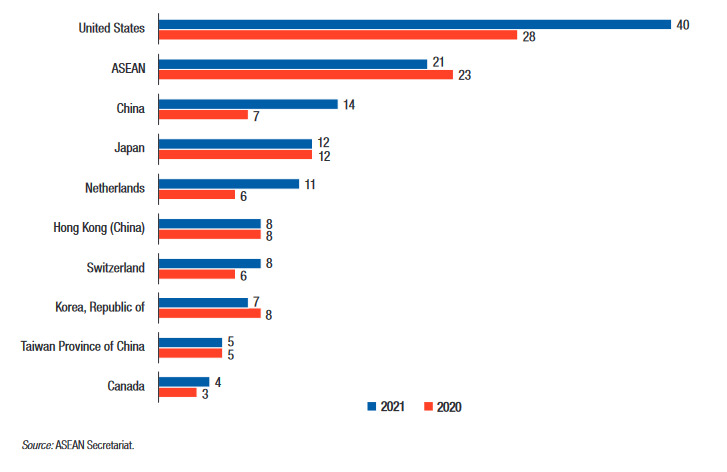

By ranking, the US is ASEAN’s largest source of foreign direct investments with a 23 % share to total inflows, mainly to financial and insurance services, and manufacturing sectors

Even after including Hong Kong's FDI in China sourced investments - $15 billion in 2020 and $22 billion in 2021 - inflows originated by US firms stand out, at almost double Chinese FDI

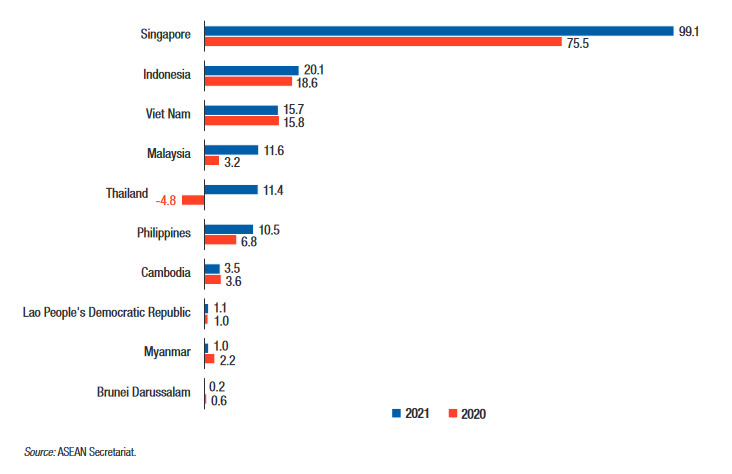

Countries receiving FDI inflows offer a mixed picture

Setting apart Singapore which, as advanced financial hub, is a uniquely positioned beneficiary of FDIs, investments inflows for Indonesia, Vietnam, Malaysia and Thailand look promising

Indonesia is ASEAN's largest recipient of FDI ($20.1 billion) which might redress the country's modest exports - either to China ($37 billion and 3.4% of GDP) or to the US ($20.2 billion and 1.9% of GDP)

However, the absence of the US amongst the Indonesia's FDI contributors is perplexing

- $7.1 billion (35% of Indonesia's FDI) originates with ASEAN countries - essentially Singapore ($5 billion) and Thailand ($2 billion in mining interests)

- $11 billion (55% of 2021 FDI) are invested by non-ASEAN Asian countries : China (battery maker CATL), Taiwan (Foxconn), Japan (Toyota

with plans to invest $2 billion over the next 5 years in EV manufacturing, followed by Honda , Mitsubishi and Suzuki ) and South-Korea (Hyundai and battery maker LG Chem) initiated investments amounting to $7 billion - the balance - $2 billion - was invested by 'other countries' - including the US

Indonesia's mineral wealth is central to the country's policy supporting value adding (and job creating) downstream industries by banning exports of raw materials (in defiance of WTO rulings)

Mining reserves include 22% of global nickel reserves, on par with Australia's 21% - fourth largest coal exporter - 4% of the world reserves in bauxite - tin and cobalt) but contributed only 5% to Indonesia’s GDP in 2019, according to the Extractive Industries Transparency Initiatives

The 2019 ban on nickel exports has moved the country to the forefront of electric battery production, financed by Chinese firms (notably CATL) and others

The Indonesian EV (electrical vehicles) value chain - from mining and smelting to production of batteries and assembly of EVs - represents more than 50% of total FDI 2021 - with more to come, attested by the line-up of Asian carmakers

The December 2022 announcement that bauxite exports would be banned from June 2023 signals the deepening of the country's industrial ambitions to favor refining capacity (instead of importing finished aluminium at a cost of $2 billion as of 2021)

The lack of substantial American commitment in the country is striking - data centers by AWS

By requiring environmentally 'clean' energy to operate the refinery capacity needed, Western foreign banks might be constrained in a country running mainly on its abundant coal reserves....

Asian financial supporters do not appear to have such reservations....highlighting unintentional consequences of sound principles and raising hard questions about their implementation

Vietnam FDI - significant but stable at $15.7 billion - is sourced essentially from Asian countries (80%)

- The lack of US investments is (again) noteworthy, in the light of the country's growing exports to America - $119 billion, as of Nov. 2022 - generating a trade of goods deficit of $108 billion

Thailand benefits from strong manufacturing investment in the electrical and electronics industry and the automotive industry

Malaysia also benefits from robust manufacturing investment

- FDIs bolster the semi-conductor supply chains in the countries with established expertise (Thailand, the Philippines and Singapore, next to Malaysia)

- Multi-year investments are committed by Intel ($7.1 billion semiconductor packaging plant)

, Germany's Infineon ($2.6 billion plant expansion) and Micron Technology - Semiconductors for the automotive industry attracted Japan's Denso

and Germany's Bosch

The Philippines hit the highest level of FDI ever, with a 54% increase to $10.5 billion, sourced mainly from Singapore, Japan, the United States and Netherlands

- Political support is highlighted by the amendments to the “Foreign Investments Act of 1991” (Republic Act No.11647) which allow investors to fully own investment projects, including in micro and small enterprisesw

FDI - America's strength and America's weakness

By size (23% of total FDI ASEAN inflows), dominance by its currency and strength of its international banking system, the US are in a unique position to channel support to the industrial goals of ASEAN countries

However, the diversification of supply chains, seeking to redress unique dependency on China's powerful manufacturing engine, appears to remain more haphazard than its potential could imply

Self-imposed constraints in allocating American finance mirror ambivalence about globalization itself

Despite the potential to channel efficiency and profitability of US firms, global strategies risk incuring a storm of principled oppositions on the home market

Side-stepping the EV supply chain in Indonesia may just be one of the more significant lost opportunities

Left in doubt...

Selective US investments - favoring a few ASEAN countries - and concentrated on industries with an established record - constrain the deployment of the full potential of American firms

- US investment in ASEAN semiconductor manufacturing, R&D and Sales dominates the industry locally (followed by EU countries) with presence in Malaysia, the Philippines and Singapore

- Large Asian firms - TSMC (Taiwan)

, Samsung and SK Hynix (South Korea) have no presence - except in planning stage (Samsung in Vietnam) - Electrical vehicle supply chains remain (mostly) outside the scope of US investors, dwarfed by their Asian counterparts

- Relatively small FDI commitments by American firms to Indonesia and Vietnam (the later an important export market to the US) stand out and remain hard to explain

BRI - How steady is China's grip in South-East Asia ?

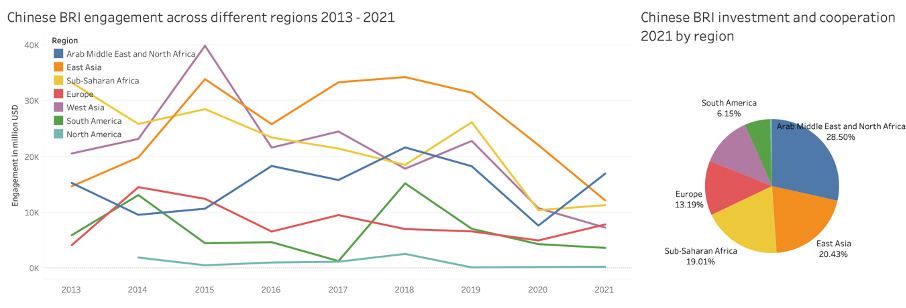

BRI - as the Chinese Belt and Road Initiative is known - has been launched in 2013

A sweeping plan to promote infrastructure development across Africa, Asia, and Europe with Chinese financing, BRI has allocated $120 billion in loans during its peak lending years (from 2014 to 2017)

As discussed in "China's Geopolitics of Trade', infrastructure priorities in South-East Asia (13 railroad projects and 5 ports) reflect China's strategic security concerns (access to open seas) and controling interests in regional supply chains

As the program evolved since 2017, priorities shifted to Arab and African countries

Out of Chinese engagement through financial investments and contractual cooperation for the year 2021 of $59.5 billion, East Asian share fell to $12 billion (from $30 billion in 2019) and West Asian projects from $22 billion to$7.5 billion)

Skewed by investment priorities advancing China's energy security and trade concerns, economic benefits, though significant, remain hard to ascertain

In terms of impact on the local South-East Asian economies, arguably, the current BRI programs share the merits and the limitations of US private initiatives - positive contributions to economic productivity but usually weighed down by the backer's interests

- China's focus on energy benefits Iraq with more than 50% of total energy projects. South-East Asia's scope is limited - except for renewable energy projects in Indonesia, Vietnam and Thailand

- Transportation commitments in the region are extension of familiar Chinese priorities in the region (railroads and ports)

Though investment terms do not make for easy comparison,

- US sourced FDI raised $40 billion in 2021

- China and Hong Kong FDI sourced FDI raised $22 billion and the BRI (East Asia) allocated $12 billion

In the magnetic field of South-East Asia trade and development policies, investment decisions, untethererd from narrowly defined foreign - American or Chinese - policies, would contribute to more credible partnerships

In this respect, American trading venues and investment driven by private industry could upend BRI strategies in nimbleness and reach

Difficult but not impossible to achieve, an open-handed American investment commitment would fit the South-East Asian balancing act between the super-powers...

...by another name, the Virtues of Soft Power, discussed in a follow-up report