Robotics are closely related with automation processes and, in combination with software applications, some companies dominate niche markets, for instance in healthcare, in consumer markets or in logistics

The present theme is focused on general industrial robotics and should be evaluated in combination with 'Industrial Processes'

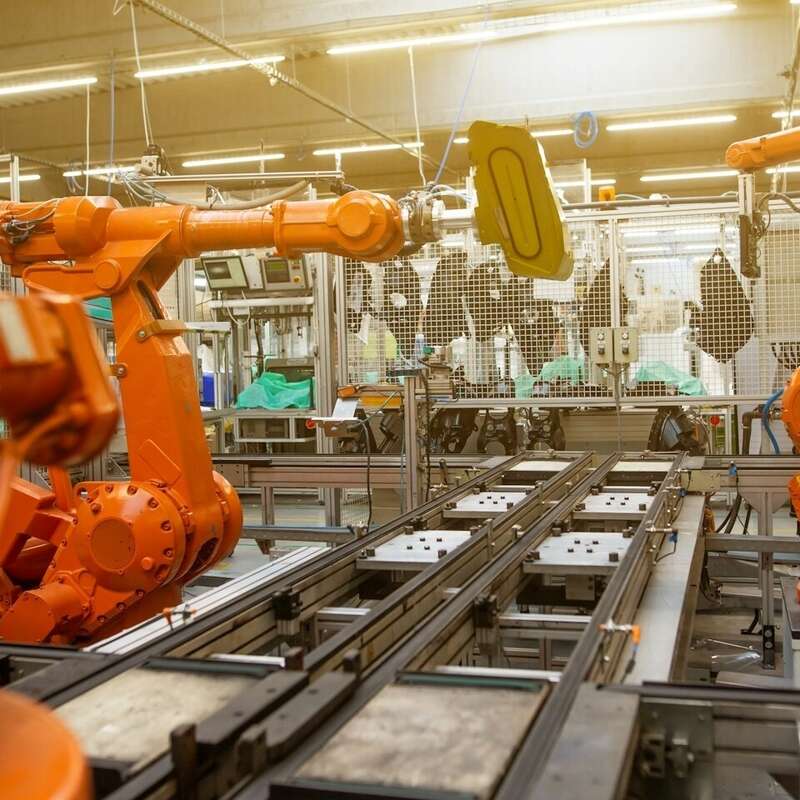

The general industrial robotics manufacturing is concentrated on 4 non-US companies, two of which are Japanese (Fanuc and Yashkawa), one is Chinese-owned German Kuka and one is Swiss-Swedish ABB

To facilitate comparison, industrial conglomerates with leading expertise in robotics and automation are included in the selection

As of 2023 (latest data from the International Federation of Robotics (IFR), 4.28 million robots were in operation worldwide and 541 000 units were installed during the year, a growth rate of 10% year-on-year

70% of the robots were installed in Asia and China has been the region´s largest adopter with 276 288 units shipped in 2023 (51% of the newly installed world total) - The share of Chinese manufacturers in the domestic market has grown considerably since 2022, reaching 47% in 2023. It has fluctuated around 28% over the past decade

Between 2017 and 2022, robot installations in China have increased by 13% each year - in 2024, the People’s Republic of China reached a high robot density of 470 robots per 10,000 employees, compared with 402 units in 2022.

The key industries - according to a previous 2020 IFR report - are Automotive (28% of total stock), Electronics (25%) and Metal industry (10%)

In a broad sense, robotics are integral part of distinct segments : industrial automation, service robotics, automated guided vehicles, collaborative robots (interacting with human workload) and household robots

According to Future Market Insights, the industrial robotics market is projected to grow from $39 billion in 2023 to $96.8 billion by 2025 and to $220 billion by 2033, at an estimated CAGR of 18.9% between 2023 and 2033

East Asia is expected to maintain its dominant market position, accounting for more than 2/3 of global revenue generated in 2023

Niche themes such as 'Medical Robotics', 'Warehouses - Automation of the Supply Chain' or 'ADAS - automated driving' are reviewed as part of this series