China built its emergence as superpower on manufacturing

The strategy 1.0 rolled out in plain sight since the early 2000

- Aiming for production in massive volume, at low cost, for the vast consumer markets of the developed West

- Drawing on the eagerness of Western companies to outsource production of finished goods to the integrated Chinese supply chains

Success has been astounding

China is solidly installed in the driver’s seat as the ultimate assembly factory (and often the ultimate network of factories), fulfilling orders of Western design, engineering or marketing companies, downgrading manufacturing roots of those companies

After 20 years of growth, a pushback, predictable and widely shared across the political spectrum, drives a call for “reindustrialization” in the West

This raises an uncomfortable question:

Is ‘turning back the clock’ wise, assuming it would be possible…

I will argue that ‘onshoring’, the political ambition to relocate supply chains closer to home, needs to confront hard realities

- A 21st century plant will thrive on automation, supported by a mix of job profiles to operate robotic assembly lines

- China’s export engine is broadening its export push to the production of intermediate goods and machinery

On-shoring promoted in the West is an answer to yesterday’s trade wars while the China export strategy 2.0 is already on a roll

Taking a long view of the 21st century manufacturing business of ‘making things’, a 'reinvention' of Western production centers needs to be a work-in-progress for new technologies, new factory size and new locations

Relocation in the old industrial grounds is an uncertain, one-size-fits-all proposition which will not do

Aiming to secure large job opportunities, the current ‘reinvention’ of a manufacturing base in developed countries is likely to fall short of expectations

The Industrial Robot and Me

A 21st century production site might be eerily empty of human workers on the assembly lines

That is because robots have sent the workers, actually engineers and software experts, to the control rooms, away from the factory floors

The automotive industry may be the most extreme case of robotization but not its end station, far from it

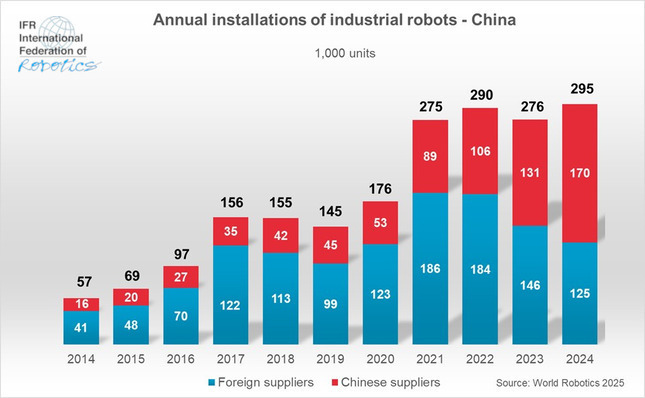

According to the International Federation of Robotics, 550 000 industrial robots have been installed globally in 2024 (74% of which in Asia)

A silent manufacturing revolution is on the march, with the 4.7 million robots actively used on factory floors globally (2024 data)

To make sense of this trend, comparatively costly labor in developed countries may just be one factor supporting robotization and hardly the most significant one

Actual labor costs surely do not square with the size of industrial investments in China, which leads with 54% of robots deployed in 2024

China is the front runner with 295 000 robots installed that year and 2 million robots in operation

Japan and South Korea come next with 44 500 and 30 600 robots

In the Western world, only Germany (with 27 000 robots) and the U.S. (with 34 000 robots) stand out, with European countries in the lower tier (from 4000 to 9000 robots installed)

The gap is hair-raising – with Germany, a premier industrial exporter committing to less than 10% of China’s industrial robots, while the U.S. investment sits at just 11.5% of the Chinese annual robot deployment in 2024

Domestic capacity build-up in China in advanced manufacturing segments eschewed many of the 20th century methods in operation across factories in the Western world

Direct adoption of software driven technologies, on fully automated state-of-the-art production lines, is attested by the large investment in robotics

And this is just a snapshot in the upward trend, with robotics installations expected to grow in China at an estimated 10% annually until 2028 (IFR data)

Self-sufficiency, a mantra

The industrial segments prioritized by the Chinese 5-year plan responded to political guidelines set by the central government

Encouraging national self-reliance, the policies ignited an investment race, industry by industry, across the country, with red-hot support of local governments eager to be first in line

In highly productive factories, geared towards volume, on sharply competitive domestic markets, those public policies set the stage perfectly for overproduction all along the supply chains

Predictably, in China heavy losses and potential bankruptcies beckon, although companies and their financial backers (often local governments themselves or by way of their financial vehicles) have been doubling down on the effort to break into their assigned domestic market segment

Exports, the answers to all ailing

With looming losses of great magnitude, the companies leading the fight for domestic market share have turned to the export markets for profitable sales

The generation of a return on their industrial investment with a sales mix on domestic and export markets has been a guide to survival, not always the result of well-thought-out plans

This is how China’s advanced tech firms, which are the 5-year plan priorities, have started to build massive export stakes, challenging established brands with innovative product ranges,

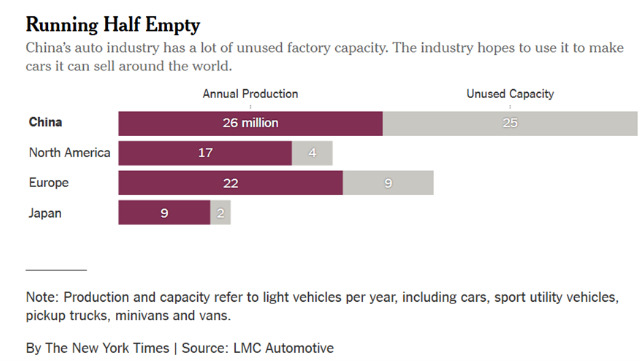

The Chinese automotive industry is a case in point

Production capacity of ICE (internal combustion) cars is vastly oversupplied at 40 million vehicles to cover domestic demand of just 11.5 million cars

Even after accounting for plant closures and bankruptcies, where would all the ‘left-over’ ICE cars go, except to export markets at cutthroat prices, displacing legacy brands globally

As for EVs (electrical vehicles and hybrids), 16.5 to 20 million are in production annually, representing 75% of world manufacture – estimates vary – with exports of 2.5 million cars in 2025

Booming demand (+100% to +190% in Germany, South Korea or Australia for instance), tarifs notwithstanding, is hurting legacy car makers in their home market, on the Chinese market and in their traditional exports worldwide

To sum up the wild, wild west of car manufacturing is here

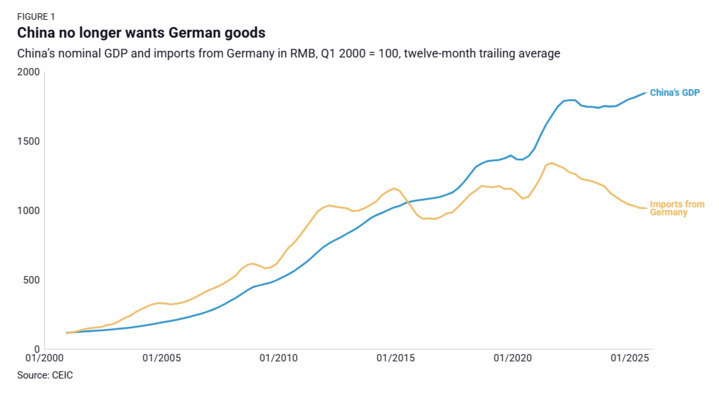

Aiming at self-sufficiency across the board, the Chinese strategies have contributed to boost exports of higher end product categories which Western manufacturers used to dominate

As intended, the policy impacted Chinese imports, resulting in market share loss for traditional exporters to China such as Germany

The export-import data for Germany, impacting German cars but also Chemicals, Electrical Equipment or Manufactured Goods, feeds a year-on-year increasing trade surplus between the two countries

Over the past five years, since 2018 / 2020, the reversal of what used to be a mutually beneficial relationship is striking

The differential between urgent exports (to keep the Chinese economy rolling) and weak demand for manufactured imports will only widen

The train has left the station

The good and great Western companies are not on board

Europe does not have much of a choice and the European Union does not have a plan B

In summary

China 2.0 may appear to prioritize Europe with its 450 million reasonably well-to-do consumers

However, a more daunting pivot is underway targeting less well-served emerging markets

The focus on more technologically advanced exports, anchored in its flagship Made in China 2025 industrial policy plan, is a double-edged sword

- Massive investments in domestic production achieved the primary goal by improving self-sufficiency

- Oversupply of goods turns out to be equally massive and price wars create a deflationary downdraft in China

Predictably, Chinese manufacturers are turning to export markets to balance their domestic losses on profitable foreign markets

Trade surplus reached an all-times high in 2025 at $1.2 trillion, according official Chinese data, but is estimated to be higher

Future trends of the trade surplus will make headlines because structurally, Chinese manufacturers must seek out new markets to survive

Western markets are just an important part of the story and loss of domestic market share is hurting

There is worse to come for global exports of the Western legacy firms as the less well-served emerging markets become prime targets for the Chinese export machine

By geographical proximity, South-East Asia will model China's trade policy by combining a commercial push with an active promotion of the yuan as payment currency

I will discuss how the growing stake of Chinese exports in the country's "near-beyond" is foundational in the yuan's recognition as international currency in my follow-up report 'The Yuan also rises...'