Portfolio construction going back to basics, with sector diversification, momentum and beta aligned with total market, is a solid investment approach

By selecting filters, the investor is encouraged to clarify priorities

The selection might focus on a plain market cap segment and momentum or seek a fine-tuned ranking such as by operating income, financial ranking and volatility

With an eye on the total market, any asset list is a framework setting the boundaries of the investor’s own choosing, never a definite ‘answer’ how to invest

Rather than ‘simulations’ of what the future is supposed to portend, filtered lists challenge the investor in exercising judgement based on experience or intuition

How to invest in times of ‘hype’

It is fair to say that only visionary investors are early in really innovative, world-changing technology

What can make a difference for the rest of us are ‘picks and shovels’ strategies (shovel-sellers earned the money, not the gold diggers…)

Case in point: the construction of data centers relies on key suppliers in refrigeration, in electronics and other equipment, offering a range of investment opportunities

This remains true today, just harder to come by…

Whatever exciting capex growth projections are made, share prices along the tech supply chains should be reflecting their expected profitability by now (perhaps over optimistically…)

Single-stock mania is best avoided for those reasons, and a few more

- ‘Mania’ drives retail investors to stand in awe about the potential of the end-product (or consumer service)

- Day-one investments in Google or Facebook IPOs prove nothing about the future performance of SpaceX or OpenAI – Ownership of these stocks is a shot in the dark

- By itself, this is not a reason to stick to the ringside but the “picks and shovels” making the dream come true just sound like a better, and less crowded, bet

If you still insist on SpaceX, the only question of relevance relates to the structure of the portfolio, and its diversification: what stock positions you are willing to sell to make room for SpaceX?

This brings me to my ‘thought exercise’ with this old-school portfolio, created a year ago (and not simulated for the purpose of this presentation)

An old-school equity portfolio construction

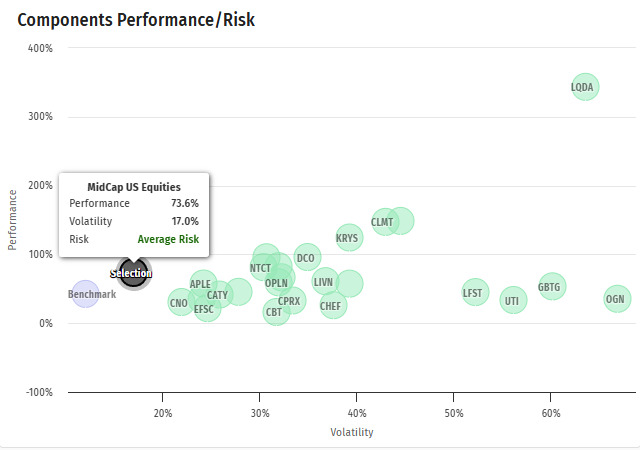

This selection of Mid Cap U.S. equities, tested over more than a year, has been very informative (and profitable) from the start

In construction of the portfolio, the rules were straightforward

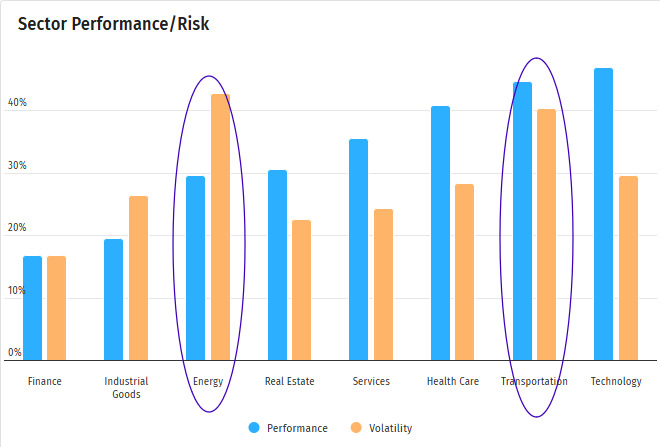

- Diversification across sectors, but deliberately underweight in technology

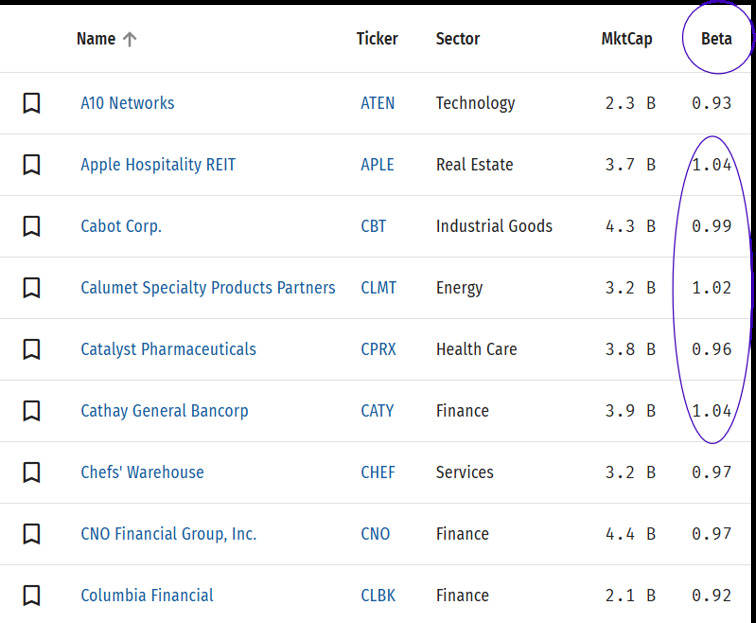

- Asset volatility moving in sync with the total market (beta ratio close to 1)

- Strong momentum, defined as duration of a weekly price average trend outpacing a one-month trend

The actual portfolio distributes performance and risk (measured by stock price volatility) fairly well, with a few outliers

For ‘housekeeping’, one or more positions might need to be sold either to take profit, to rebalance or to exclude outliers (such as highly volatile Transportation or geopolitically sensitive Energy)

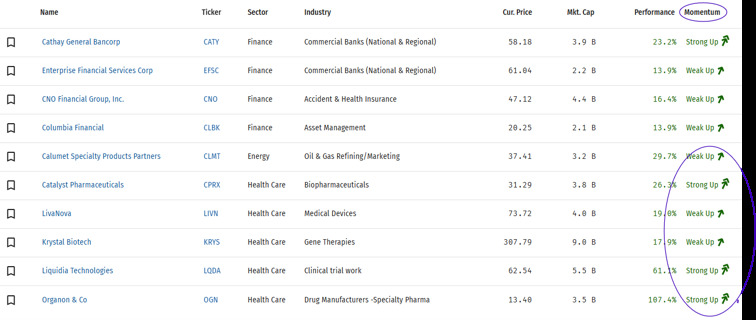

The selection follows the rules I set out from the start

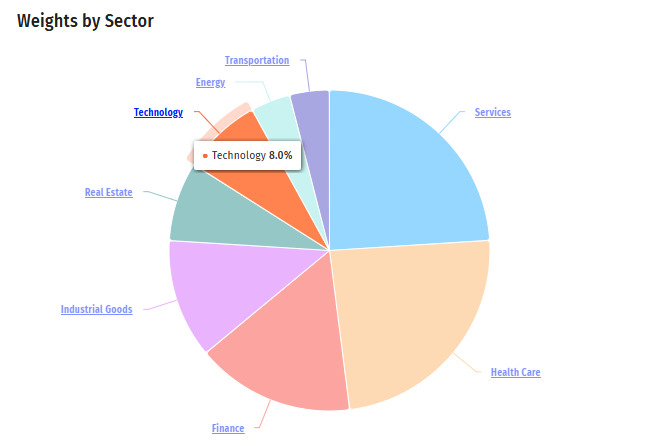

Diversified across 8 sectors

Dominated by Services, Healthcare, Finance and Industrial Goods – Technology is underweight (just 8% of total)

Beta sits between 0.9 and 1.04

Momentum

In the top quintiles from ‘weak up’ to ‘strong up’

Momentum is counterintuitive in a portfolio held for months, not days but as explained on the platform I have been using, it is the duration of the actual short-term momentum which is ranked – Strong momentum implies a build-up of weekly averages overpowering monthly averages

Performance has been very good on a stable growth trend

- +66% over past 12 months

- +44% over past 6 months

- +32% over past 3 months

What to conclude from this experiment

1°

It is easy to overthink a portfolio construction because of the massive data you can access

The “Equity Explorer” screen I am using posts 16 parameters and 6 filters (accounting ratios, profitability, momentum, etc.)

In a disciplined approach, I believe two, or maybe three, parameters should be good enough in portfolio construction

Refining a selection is always a temptation but the cost of ‘overfitting’ is high: you lose clarity of investment intent

2°

My focus on Mid Cap equities with an underweighted Technology segment is just prudent; inclusion of overhyped “mega cap’ equities and concentration on the technology sector would not reflect ‘investment intent’

I am not out to prove anything or recommend any special strategy in portfolio construction

Many cases can be made for alternative investment strategies, such as trend reversal of software companies, currently under pressure of AI

I will post alternative strategies soon