The convergence of sharply reduced satellite launch costs, with tough competition by private enterprise, and radical advance in satellite technology is the opening act of a new era in global communications

None of the established players - telco utilities, cable industry and media content providers - can afford to ignore the profound changes in the making

But to gain a clear understanding of the future on our doorstep, a review of the systemic shift gaining speed under our eyes will lend some insights

Are satellite communications about to benefit from the convergence of two unique trends in the short term (2019-2021) ?

This seems to be the case, and the world’s most powerful private investors endeavor to make the vision come true

- The new economics of rocket launchers have send the costs tumbling

- Fleets of satellites are challenging the multi-purpose behemoths which used to rule space communications

The era of hundreds – if not thousands – of low-cost satellites, launched competitively, leaves the legacy players in the rocket business, in satellite fabrication and in satellite communications scrambling

As for the capital expenditures, already committed or lined-up to boost their competitive edge, the wherewithal of Google

Privateers and gate-crashers

Sometimes colored with talk of inter-planetary exploration, the private rocket launch services developed since the mid-2010’s remains essentially a hard-headed, albeit audacious, calculation of the potential riches beckoning above our heads

Until the late 2000’s, the development of rocket launchers relied on national defense programs, with specifications implying high cost structures for US government contractors (Boeing

Since the early 2010’s, rocket launchers by privately financed start-ups, Blue Origin (J. Bezos), Space X (E. Musk) and Virgin Orbit (R. Branson), started to put considerable price pressure on the legacy firms – American United Launch Alliance (ULA), European Arianespace and the Russian International Launch Services

By December 2013, the credibility of the SpaceX pricing strategy became incontrovertible with the successful launch by a Falcon rocket of a satellite in geostationary orbit (at an altitude of about 23 000 miles), dropping the cost of individual launches from the $100 million range to $60 million

Following a successful recovery of a first stage SpaceX rocket (Dec. 2015), SpaceX forecasted an approximately 30 percent launch price reduction from the use of a reused first stage, after accounting for extensive refurbishing of the stage, successfully relaunched in March 2017

While ULA and Arianespace engaged in major restructuring processes, Falcon 9 of Space X has become a significant player. The 2015 certification by the US Air Force ended ULA’s monopoly on US defense satellites and 18 successful launches of the Falcon in 2017 (compared to 11 launches for Arianespace) established SpaceX as a major player

SpaceX followed suit with 21 launches in 2018, ULA just 8 and Arianespace 5 launches (and one partial failure)

Disrupting a well-worn business model, the emergence of significant private players is a game changer for the satellite operators as well as for governmental defense agencies

- Shifting away from deep contractual commitments, the US Defense department has become less of a partner and more of a hard-nosed client, voicing its support for securing a ‘competitive industrial base’ of multiple players including ULA, Blue Origin and Northrop Gruman

(following the 2015 acquisition of Orbital ATK) as well as Space X - Communications by way of satellites on low-earth orbits (LEO), launched by Globalstar, Iridium

and Teledesic in the 1990s, were a technical success brought down by an unmanageable cost structure. Deep cuts in launching costs bring satellite networks within reach

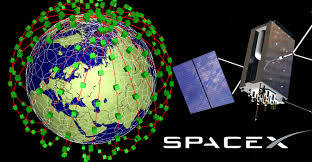

SpaceX has made history with the launch of 64 satellites in one go in December '18, in what was one of the largest satellite ride-sharing missions ever launched

OneWeb, another of the network contenders 40% owned by a Softbank investment fund which committed $1billion in 2016 , launched 6 satellites in February 2019, the first stage of a planned minimum of 650 satellites by 2027 orbiting at 16 000 miles (Intelsat has 59 today and Iridium 66....)

Not to be outdone, Iridium had launched 10 satellites on a SpaceX Falcon in January '19....

A revolution by an order of magnitude, the benefit of much reduced launching cost is compounded by radical innovations in satellite technology

Hi-tech mass production

Any attempt to rank the key factors of technological break-through in satellite construction would be disputable and its conclusions quickly superseded by a new wave of innovation

But in the build-up of a satellite network, some markers might conceivably assist the investor in evaluating the pace of new developments

In terms of technical goals,

- The reduction of latency (maximum signal lag) is critical for real-time, two-way communications and a stumbling block for satellite communications; 5G performance benchmarks of 1 millisecond are way off. Geostationary satellites at 24 000 miles shadow the earth turning on its axis with a signal lag by 500 to 700 milliseconds but, at much lower orbits, a 50 millisecond latency is within reach

- The miniaturization of satellites ensues from the necessity to ‘seed’ any orbit close to earth (LEO between 500 and 1 000 miles and very-low-earth in the 208-215 miles range) with a constellation of satellites spinning beyond the horizon at 16 200 miles per hour, relaying one another in sequence, and within minutes

- Electric satellite propulsion is expected to lead to a reduction in weight by as much as 50% from the conventional chemical propellant

- Capacity to send and receive data depends on the number of radio beams of the satellite, 16 independent beams per satellite in the OneWeb network for instance

The sheer number of satellites in a 'constellation' spinning in low orbits around the earth transformed the production from a sophisticated cottage industry, where every component was made to order, no expense spared, into staged mass production with dedicated workstations for propulsion systems, communication gear, solar panels, etc., relying on standardized semi-conductor components

OneWeb's planned 650 to 900 satellites, dwarfed again by the nearly 12 000 satellites for which SpaceX obtained FCC approval, is indicative of the quantitative shift in the industry

Gateways

The effort is all the more impressive because of compressed timelines; the FCC approval is conditional on 6 000 SpaceX satellites orbiting by 2024

To be economically viable for supportive investors, the last stumbling bloc and perhaps the most decisive stage for satellite constellations is to get data back to earth, within grasp of end users

Past multi-billion efforts led by Globalstar, Iridium and Teledesic in the 1990s failed because, on top of cost, poor access to ground terminals made for haphazard data feeds, compelling the contenders to downsize services to vehicles with their own terminals (ships, planes) and to poorly served land stretches (islands)

The same factors presumably played out for firms such as Gogo

The implication, and our premise, is that who controls the access to ground terminals will dominate the skies ...because the satellite services, in the competitive landscape taking shape, will ultimately be a commodity

Ground terminals tracking satellites racing across the sky on 'very-low-earth-orbits' are preparing to meet challengs of their own : mechanical antennas, of the type in use for 'stationary' satellites are untenable and electronic antennas under development at Kymeta, Phasor and Isotropic Systems are in

Assuming the technical solutions researched by these firms prove successful, the breath of distribution may pit Internet service providers against the constellations over time ...

And sooner rather than later...if the latest authorization requested from FCC in Feb. '19 by SpaceX Services, a subsidiary of SpaceX, of a blanket license to deploy one-million stations is to be considered

As reported by ExtremeTech,

- The SpaceX constellation is set to operate in the Ku-band spectrum, thus the FCC’s involvement. The Earth stations will transmit at 14.0-14.5GHz and receive signals at 10.7-12.7GHz. For comparison, current LTE networks operate at 600MHz to 2.5GHz. SpaceX has said that Starlink could provide gigabit speeds with latency as low as 25ms, putting it on par with terrestrial broadband

One does not need to be impressed by the other ventures of Mr. Musk, which have a lot to do with marketing genius, to ascertain that SpaceX may be the entrepreneur's most visionary disruption

We hope to discuss the many industries impacted by the revolution in satellite communications in our follow-up report