The sharp rise in yield on yen bonds, and the sharp drop in yen/$ rate, in recent weeks, has been interpreted in the global markets as a preordained failure of Japan's attempts at monetary 'normalization' - after more than a decade of deflation

Not so fast ...

Because of the massive involvement of foreign borrowers on Japan's money markets, the exchange rate of the yen and the yield on its bonds are everyone's problem

...and more precisely an American problem

In 'Indispensable Yen', published last December, I highlighted the challenge facing the Bank of Japan (BoJ) to simultaneously strengthen the yen, which is necessary to keep a check on inflation, especially on imported energy, and to normalize the interest rate curve to reward the Japanese bondholders

Resurgent inflation which, since Jan. 2022, increased from 0.5% to 3%, compels the BoJ to take action and cautious increases in interest rates signal a regime change, aimed at making yen holdings more attractive

Japan's support of the yen could pivot between success and failure

In the short term, the jury is out - by acting preemptively, the BoJ has shown its determination and has surely prepared the fire power to respond to market turbulence and spikes in yields

In the long term, Japan will face hard budgetary choices to face the country's much diminished demographics but doing so with the backing of sound finances would make all the difference

Counterintuitively, the Bank has signaled that the country could only be worse off ... by doing nothing

To achieve its domestic goals, the Japanese monetary authorities will be intend to convey the strong support of its most essential currency counterparty, the American monetary authorities

Linkage between the two currencies has been a one-way street for years, as American fund managers borrowed in yen (at the lowest rates) to invest (with leverage) in U.S. high return assets, creating a structural, sustained selling pressure on the yen

Called 'carry-trade', linkage between U.S. dollar and yen has been one of the essential global sources of financial liquidity and, in a reversal, the impact of liquidity 'leaking away' from U.S. equity and bond markets could be massive and immediate

However much the U.S. Treasury seeks to give an impression of aloofness, the American authorities could not be more closely involved

Ultimately, the credibility of the Japanese 'regime change' holds the U.S. Treasury hostage - winning together or...failing in unison

Regime change ?

On the Japanese domestic front, doomsayers have a field day focusing on the intractable problems of the country

Collapsing demographics - the number of working-age people (15 to 64 years old) drops by 15% from peak in 1997 - a loss of 13.5 million and a trend set to worsen with the very low birth rate

A very large gross debt-to-GDP ratio, in excess of 200%, with a worsening medium-term outlook - public debt is bound to increase to support people in old age while GDP is expected to be negatively impacted by the fall in working-age population

At approx. $9 trillion, Japanese public debt is over 90% domestically financed - the Central Bank is the dominant holder (45%-50%), followed by domestic insurance companies and banks (30%), and private investors

The savings rate of the aging Japanese household is declining and expected to turn negative by 2030 as more people draw down their savings while government debt keeps growing, making foreign funding inescapable

The debt-to-GDP ratio offers very little leeway

Average interest rate on the debt is still low but debt at low rates will be maturing in the short term, and interest expenses will start to rise

Social security expenditures, linked to an aging population, as births hit a record low in 2023, with a total fertility rate of just 1.20, wil continue to be a key driver of growing public debt

In the national budget, interest and debt redemption accounts for 24% of total budgetary expenditures at past very low rates

- A not improbable 1% increase in rates would add approx. $24 to 26 billion over 3 years (as old debt at lower rates gets replaced)

- In fiscal year 2026, the total budget is projected at an equivalent $785 billion and debt service at $202.3 billion (with forecasts suggesting a 25% increase by 2028)

Introduced by the freshly elected conservative government, a stimulus package of equiv. $135 billion aims to support domestic consumption hard hit by inflation

- By signaling a very gradual trendline in short term interest rate increase, following the benchmark increase by 0.25% to 0.75%, the BoJ hopes to reassert its control over the bond market - with another 0.25% raise penciled in for July '26

- The best possible (and maybe the only good) outcome requires effective BoJ control over the bond market, a sensitive issue with current BoJ ownership (50%), hardly a premise to buy still more public debt...

Key goals will prove decisive

- Will inflation stay in a low 3% bracket

- Will domestic consumption support growth, targeted optimistically at 1.3% in 2026 (most analysts expect 0.8%)

- Will debt-to-GDP stay in a holding pattern, as proof of fiscal soundness

A pervading sense of discomfort about Japanese 'regime change' derives from the feeling that the BoJ has been unwillingly backed into making hard choices

This may be true, but the Bank's monetary strategy is supported by a government budget close to primary balance and a stabilized gross public debt

What is more, the major currency counterparties - the U.S. dollar, the Chinese yuan and the euro - have a vested interest in a controlled yen

For now, traders betting the BoJ's plan is just another false dawn might do so at their peril...

The carry-trade - everyone's problem

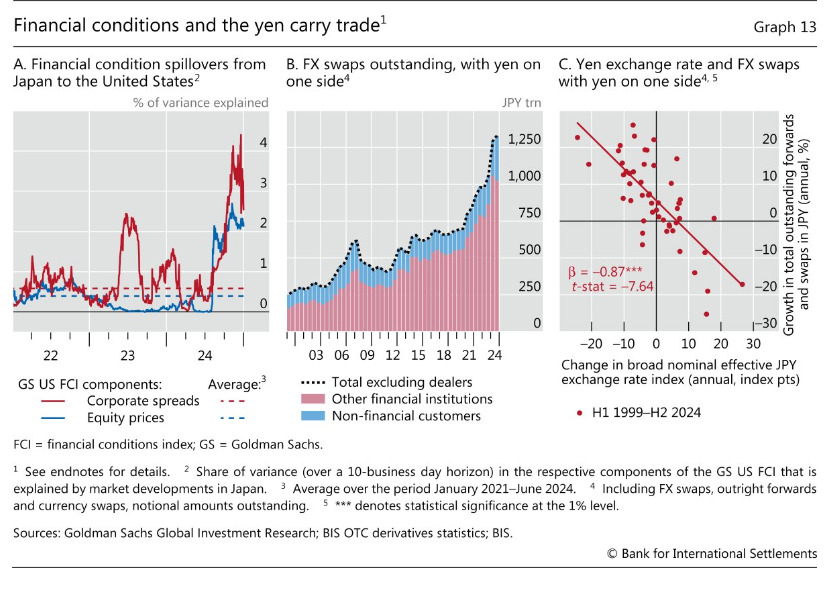

With a remarkable sense of understatement, the July 2025 report of the Bank for International Settlements (BIS) noted that :

"Despite the post-Covid tightening of US monetary policy, financial conditions in the country had remained fairly loose. This was in part due to the transmission of easier financial conditions from Japan to the United States"

So much for endless criticism of the U.S. Federal Reserve for 'holding interest rates too high for too long' to constrain financial conditions...

This is all about the 'carry trade' whereby cheap loans in yen (at close to zero interest rate) are converted in U.S. dollars for - often leveraged - investments in U.S. assets ( such as Treasuries or equities) - a one-way street paved with financial profits as long as the differential between cost of loans in yen (including FX swaps to hedge the currency risk) and return on the assets is positive

The magnitude of such carry-trades is hard to estimate - size and volatility are notoriously fickle...

The BIS based a rough evaluation on the dynamics of the hedges - FX swaps in yen (graph 13-B&C) - at $1 to $2 trillion (other analysts suggest estimates as high as $4 trillion)

With an August 2024 partial but sudden unwinding of yen carry trades triggering spillovers of external financial conditions into the United States, the BIS "underscores the highly connected nature of global financial markets and highlights how domestic financial conditions can be significantly shaped by foreign developments"

My note on "Indispensable Yen" referred to the Japanese currency as a fount of great riches...until the source of liquidity dries up, as I showed with the negative correlation between Nvidia share prices and 10-year Japanese notes

Because of the magnitude of potential currency risk, exposing investors in yen to losses even if the interest earned on government debt rises, support of the BoJ's approach remains lukewarm (at best...)

Much remains to be proven in the regime change promised by Japan's budgetary and monetary authorities to cement trust

However, the domestic fundamentals viewed from a Japanese perspective are strongly incentivized

- The yen carry trade significantly contributes to the weakness of the yen because investors borrow in low-yielding yen to invest in higher-yielding currencies, creating a structural, sustained selling pressure on the yen

- Resulting inflationary pressures on the imports (especially energy) shatters the consensus supporting Japanese low yield debt with the savings of Japanese households

- Public gross debt (the usually quoted percentage of GDP ...netted with public assets, the percentage is much smaller) is immense but slowly trending down - and owned nationally for now, unconstrained by international investors

Putting "House Japan" in order in the short term will allow the government to tackle medium-term structural constraints from a strong position

...as all Central Banks surely realize and support

It is never advisable to bet against one Central Bank ... or two ...or three