The VIE acronym stands for Variable Interest Entity

The VIE is a business structure, widely used by Chinese companies listed on US markets, to circumvent stringent domestic regulations in certain “sensitive” or “strategic” business sectors

The Chinese regulator is obviously aware of the framework, which appears to be tolerated

Since no legal standing has been given to the VIEs, shareholders of US-listed Chinese companies using the vehicle should be aware of the built-in terms of ownership

Because some of the companies relying on VIEs have become giants in their industry, the regulator is unlikely to backtrack on the current arrangement any time soon

But an investor should certainly take note, as we show for the recently listed Tencent Music Entertainment

A Foreign Investment Industrial Guidance Catalogue – most recently updated in 2017 – lists these “sensitive” or “strategic” business sectors that have either prohibitions or restrictions on foreign investment, such as telecommunications, e-commerce and media in general

According to Bloomberg estimates in 'China's ...door opens, but barely', dated July 1, 2018, based on their own itemized listings, the number of sectors is effectively down to 48 in 2018, from 63 in 2017 and 120 back in 2011

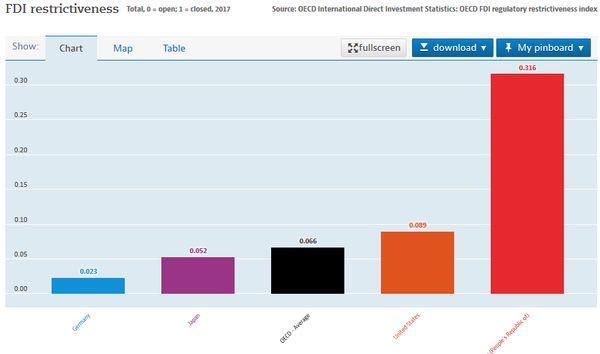

The OECD FDI (Foreign Direct Investment) restrictiveness tells a similar story with the People's Republic of China topping the list

However, the Chinese openness has to be interpreted carefully

Industry segments where foreign companies cannot compete with State conglomerates (such as railways, power or fuel retail) or will not venture (weapons manufacturers...) have been newly made ‘accessible’ since 2017

By abolishing foreign-ownership caps on financial-services companies and automakers, China is making a more significant move…over time as those changes will not apply before 2021 and 2022, respectively

With joint-ventures in the car- (and also the aircraft-) industry, the true impact of the changes remains to be seen

Media and communications are, and remain, the most tightly controlled on the ‘negative list’ of the Guidance Catalogue

VIEs, the Good

The VIEs have been introduced by accounting firm PwC in China to allow Chinese firms to raise the necessary capital for their development, foreign markets while remaining in line with the Chinese regulations, by setting up separate entities, in China and abroad

Simply stated, the firm that is listed on overseas, usually on the US or Hong Kong markets and in which foreigners can buy shares, is an offshore holding company

By way of a ‘wholly foreign owned enterprise' (WFOE) in China, the firm has contracts with one, or more, VIEs which actually own some of the underlying assets, such as intellectual property, of the listed company

By holding the permits and licenses that foreigners aren’t allowed to own but that are required to do business in China, the VIE steps in on behalf of the holding

The VIE is controlled by the firm’s top management or founders and the contracts guarantee the firm’s control over the assets, and the profits, of the firm, by way of the VIE

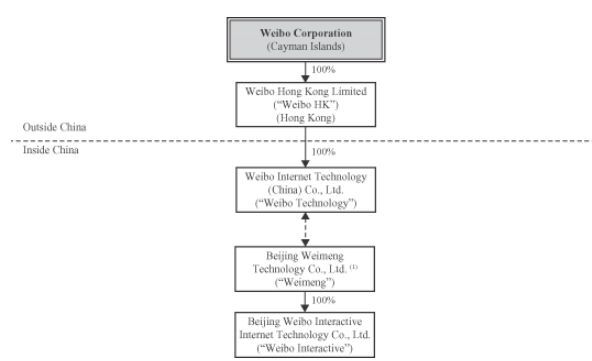

The Weibo accounting structure is the model of this work-around with a holding company, Weibo Corporation

The latter is owned by 4 non-executive Chinese employees of Weibo, in charge of the contractual agreement

- Contractual arrangements including loan agreements, share transfer agreements, loan repayment agreements, agreements on authorization to exercise shareholder’s voting power, share pledge agreements, exclusive technical services agreement, exclusive sales agency agreement and trademark license agreement

VIEs also made sense for the foreign company listed in Hong Kong or New York because FASB in 2003 (in the aftermath of the Enron debacle) adopted a specific regulation FIN 46(R) to guide the consolidation of entities for which control is unclear – implying effectively consolidation of the Chinese VIEs under GAAP

Specifically, consolidation of the entity (here the VIE) is required if the listed company “absorbs a majority of the entity’s expected losses, or receives a majority of its expected residual returns…” which is of course the case on the basis of the contracts between the WFOE (controlled by the listed company) and the VIE

72 companies, listed on US markets, are relying on the accounting structure, according to a recent study by Frederik Oqvist, 36 on Nasdaq (out of a sample of 39) and 36 on NYSE (out of a sample of 56)

The strong showing on NASDAQ should not surprise; the internet, e-commerce, education, and fintech developments are of most interest to investors and also the most prominent sectors on China’s ‘negative list’

But Mr. Oqvist highlights vast differences in the contractual arrangements; both the percentage of assets controlled by the VIEs (from 24% to 73%) and of the revenues transiting through the structure vary over wide ranges – essentially from 0 to 100%

Mr Oqvist argues that, because of such vast differences, even within a single business segment, VIEs have to be evaluated case by case by the investor

Dominated by two players, PWC and Deloitte, who together audit 60% of the companies, the VIEs of the major companies can be expected to facilitate such in-depth analysis, provided – a big if – that set standards to report financial information about the VIE could be finalized

VIEs, the Bad

VIEs, painted with a broad brush, have been criticized wholesale, and it is true the contractual arrangement creates legal uncertainty for the investor in the holding

But the paradox, in our view, is that both the foreign investors, attracted by firms in high growth technology sectors and the Chinese authorities, tolerating much flexibility in the regulatory framework, are committed

The investors, acting as responsibly as Mr Oqvist suggests, should evaluate the exact nature of the contractual arrangement with the firm’s VIE and the identity of its legal owners to forge an opinion

- The VIE contractual agreements, in their diversity, appear often to have been viewed as part of a listing’s obligatory paperwork, to be forgotten about quickly… Not only may the contractual content cover distinct obligations but physical ownership may be poorly monitored, as the representative Chinese employees enter retirement

- The identity of the auditors and of the legal advisors has additional relevance with the two key players, PWC and Deloitte, representing almost 90% of the VIEs cumulative market according to Professor Gillis, of Peking University's Guanghua School of Management

- The situation is much the same for the legal advisors, with 4 out of 19 law firms representing the companies for an approx. 80% market cap

China’s regulators may have their doubts about the free hand given to firms which so vastly outgrew their origins to become, in effect, systematically important to the Chinese economy

Dutifully, the accounts of the foreign listed companies carry a warning which would appear to be a no-go if the implications were not assumed to be innocuous

Standard warnings tell it all ….page 25 of Weibo Annual Report 2017 – Form 20-F

- If the PRC government finds that the agreements that establish the structure for operating our businesses in China do not comply with PRC regulations on foreign investment in internet and other related businesses, or if these regulations or their interpretation change in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations

Taken at face value, the warning is dire and the board seems to be stacked in favor of the Chinese regulator, whatever future developments may entail

This may have been true in 2014 when the US – China Economic and Security Review Commission drafted a report on the risks of China’s Internet Companies on US markets

But today, the hand of Chinese authorities is probably weak and has become weaker as some of the Chinese technological upstarts have grown into vast conglomerates, extending their reach beyond e-commerce (for Alibaba

To question these companies’ legal structure would throw key sectors of the Chinese economy in disarray, to begin with payment processing and fund management

Confronted with this new reality, Chinese regulators will continue to issue guidelines constraining future developments, as happens in fund management (targeting Ant Financial) and in games (involving Tencent)

But it is fair to imply VIEs are on safe ground, which throws another spanner in the works…

China has to confront the fact that some of its most successful companies are off limits for mainland Chinese investors

An attempt by smartphone manufacturer Xiaomi, listed in Hong Kong in June ’18 (ticker 1810)

Taking it all in, VIEs are ‘bad’, in an awkward sort of way, caught between contradictory demands in China and an irritant for the Chinese regulator, but secure in their very importance, both economic and social, today

VIEs, the ugly

Ugliness earmarked the VIE construct in China early on, when in 2011 Mr. Ma, founder and CEO of Alibaba, lifted Alipay, the payment application developed by the company, secretly out of the assets of the VIE to create what was to become Ant Financial

Yahoo , which at the time owned 40% of not-yet listed Alibaba, had every reason to be deeply offended

Ultimately the matter was resolved by a transaction – Alibaba securing a pre-tax payment of 49.9% of Alipay profit, later turned into a 37.5% royalty payment from Ant Financial (with a pre-set pay-out cap of $6 billion per year)

Further down the road, and quite recently, the royalties have been converted into a 33% shareholding in hugely successful Ant Financial

Ultimately resolved by Yahoo’s – and Mr. Ma’s – climb-down, the bumbling exercise of VIE’s legal rights demonstrated much that was wrong with the work-around

Maybe the ugly mark left on Alibaba explains the extra attention dedicated by the company to demonstrate exemplary practice today

In sync with the announcement of Mr. Ma’s retirement in 2019, Alibaba has announcement a restructuring of their 5 VIEs, not to be owned by Mr. Ma and other co-founders, but by holding companies with ownership spread between a wide group of senior Chinese staff

The internal reform, probably fine-tuned with the Chinese regulator (albeit informally), addresses the issues of

- ‘key-man’ risk, concentrating the power on a founder whose retirement or passing is not accounted for

- the possible abuse of legal rights attached to the VIE by a very small coterie of executives, ultimately in control of the company’s key assets

Rather than ponder on the VIEs’ shaky origin, Alibaba’s reform could be part of regulatory efforts to streamline the practice, ultimately conducive to more transparency and more security for the foreign investor...

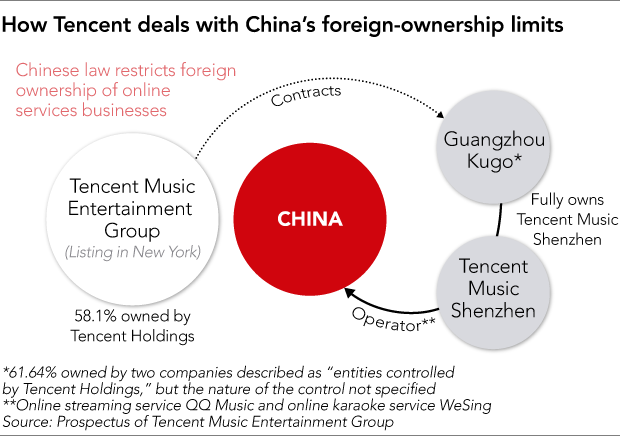

but also tighter regulatory control as the forthcoming Tencent Music IPO might suggest...

The widely advertised flotation of Tencent Music

But – as pointedly stated in the TME filings (though less commented) – Tencent Music Shenzhen (TMS), the VIE standing in for TME, operating its platforms (QQ Music and WeSing), has not yet applied to obtain the appropriate license for the business

Bluntly stated "We cannot assure you that it can successfully obtain these licenses in a timely manner, or at all"

With the IPO finally going through in early December '18, the issues appear to have been resolved and the deal has been effectively greenlighted by the Chinese regulators, although the terms of the agreement remain unknown

The structure of the interlocking foreign and Chinese shareholdings does however offer some guidance about the future of VIEs as Tencent Music Shenzhen, holder of the licenses and the Music platforms appears to be majority controlled by Chinese interests – and not by the foreign listed TME entity

...and open new questions as consolidation under GAAP " is required if the listed company “absorbs a majority of the entity’s expected losses, or receives a majority of its expected residual returns…", majority ownership by the US-listed entity which may need to be clarified

Possibly a policy going forward – a regulation in line with VIE amendments previously discussed in 2015 (paywall) and commented by Professor Gillis, leaving some Chinese tech firms left of center, such as Tencent, part-owned by South-African Naspers or CTRIP Invalid tag asset but not others, such as Baidu