Over the centuries, countries with the most sophisticated economies have been projecting power, expanding their influence by means of trade or war, and often in tandem

To achieve the exalted status of ‘superpower’, city-states in the late Middle Ages (and even before) set the trend, followed by the Dutch in the 17th century, the French for part of the 18th and the British in the 19th century

Innovative technologies, mass production (by the standards of the time) and geographical outreach advanced the ambitions of strong central authorities, backed by their armies and navies, and followed in lockstep by their tradesmen

The dynamics of power put logistics at the service of "super-states"

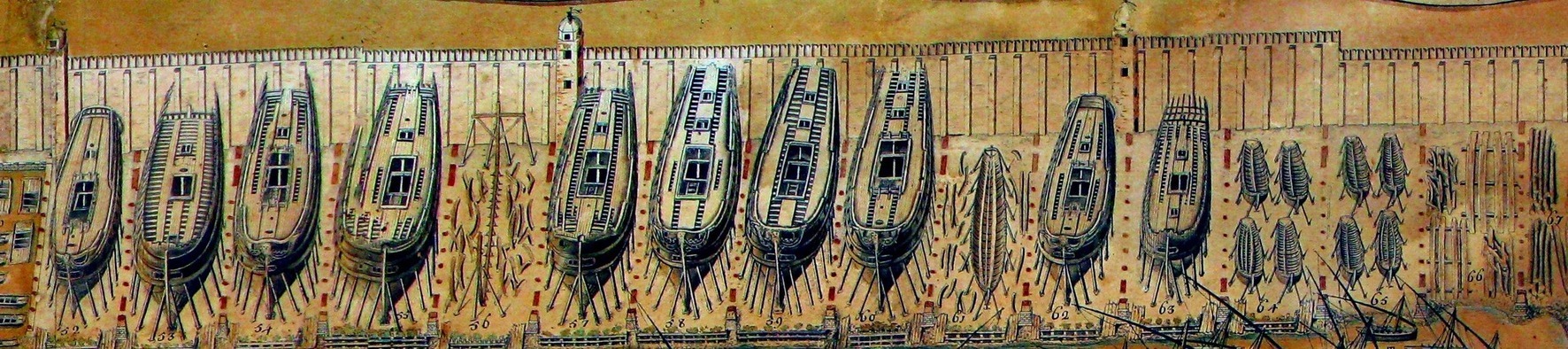

The grip Venice held on the East - Mediterranean basin, in competition with the Ottoman empire, rested in no small measure on the Arsenal which, at the apex of the city's influence in the late 16th century, could deliver 100 galleys within two months, with 16 000 workmen

The full 1797 map of the Arsenal, stitched together by Christoph Roser, of allaboutlean.com, is worth exploring (12Mb with a 8388 x 6020 pixel resolution)

World War II may have been the ultimate case of industrial dominance with American production rising from less than 2 000 combat aircraft in 1940 to close to 75 000 in the year 1944

Transport aircraft went from 164 to 10 000 over the same war period

And the America’s far-flung influence in military and commercial terms has been the success story of the Post-War period, riding the wave of leading-edge logistics networks

If the 21st century is a singular experiment in putting the mastery of logistics at the center of state power, it might be because China – in a reversal of history – relied primarily on trade as vehicle of dominance, leaving rarely used military power marooned in ambiguity

An electrifying future, published four years ago (November 2, 2018), made the case : because of the sheer size of the domestic market, Chinese regulations were leading the way for the car industry worldwide, by accelerating the transition to electrical power

The Chinese car industry, admirable in times of great danger for Western car makers, is about logistics before all else

This is why the industry is a case study of China's structured approach to industrial dominance

Tactics and strategy

Sun Tzu (born in 545 BC) reminds his readers that what appears to be a tactical choice is in fact unfolding in a strategy, part of a grand plan not yet fathomed...

All men can see the tactics whereby I conquer but what none can see is the strategy out of which victory evolves

The familiar stages of China’s expansion in the car industry, one of the top action plans singled-out in ‘Made in China 2025’, need to be viewed in a broader context and on a much longer horizon

What appear to be well-financed and mostly successful business initiatives are better understood as tactics, part of a grand scheme

Because they have been deployed very openly and rationally, the "tactics" to initiate a market for electrical vehicles could be defined as best practice in the automotive industry

- Stimulate demand by all available regulatory tools (city access, free or fast car plate attribution, subsidies)

- Force a realignment of car prices by dictating a minimum % of electric vehicles stepwise

- Establish a domestic battery industry with temporary protectionist measures, by subsidizing lithium iron phosphate (LFP) batteries that are produced locally and not the NMC/NCA batteries (which require nickel and cobalt) of foreign competitors

- Encourage the Chinese battery manufacturers to sign long term contracts with the car manufacturers, local as well as foreign, which is facilitated by the dictated % of EVs in car sales, and which also secures bank finance for the battery manufacturers

- Rely on a competitive market to sharpen the expertise of Chinese EV manufacturing, either in partnership with foreign manufacturers or on their own strength

Since 2015, these measures, mixing regulations, market competition and multiple subsidy schemes, must – with some envy – have been qualified by outsiders as a truly remarkable industrial success

Success in numbers

China has established its home market as the benchmark of electrification in transportation

- by making a strategic bet on the unexpected - a novel approach to car motorization -

- by planning every nook and cranny of the supply chain

In 2015, China's global passenger EV sales of 220 000 cars represented 26% of global sales - and electrical vehicles weighed just 0.7% of all car sales in China

From January to November '22, the cumulative production reached 6 million EVs and sales 5.25 million, 30% of all cars sold in the country

Subject to economic headwinds and poor November sales, forecasts for 2022 in China target sales of 6.4 million passenger plug-in electric cars might be overtaken - 30% of total passenger car sales of 21 million

EV exports qualifies as the next step, fast-tracked by economies of scale : domestic volume manufacturing, technological expertise and priority access to the basic resources in battery-build

China might command 60% of global EV sales for the full year 2022 if the growth trends keep up

From January to October 2022, China exported globally

- a total of 2.46 million vehicles, non-electric and electric, rising 54% from the previous year and surpassing Germany's exports to take second place behind Japan for the first time this year

- 499,000 battery driven vehicles (EVs) - year-on-year +97%

2022 total car exports (projected) - 3 million units - compare to 2019 exports of 1 million

The European Union is a key target region

With sales growing from approx. $1 billion in 2019 to $7 billion in 2021, exports are still a small fraction of the approx. $400 billion European passenger car revenue (2022 estimate)

Chinese exports could be no more than a 'warm-up' just waiting for 2022 full year numbers, expected to be large...

Trading Economics - Imports of cars from China (in millions US dollars)

source: tradingeconomics.com

Vehicle sales were just a tiny (1.3%) part of the $557 billion EU imports from China in 2021 dominated by

- Electrical, electronic equipment ($169 billion - 30% of total imports)

- Machinery, nuclear reactors, boilers ($118 billion - 21%)

- Furniture, lighting signs, prefabricated buildings ($25 billion - 4.5%)

From the perspective of Chinese trade officials, what is not to like ?

Europe will be the most attractive EV market, after China itself, in scale, limited import duties (10%), levels of income aligned with mid-range vehicles' pricing and unstinting public support of electrification

Grand schemes at scale

Implemented across China's market, scale has been the defining feature to establish a powerful domestic base for electrical vehicles

Control over global reserves of basic materials and their refining capacity has been serving domestic demand growth

With dominance in the resources to manufacture batteries, Chinese industries gains a valuable advantage in allocation - prioritizing China-made EVs by domestic as well as foreign brands - a boost to exports in the short to medium term

Graphite mining - Chinese market dominance (60%) over natural graphite (a form of elemental carbon and a constituent of Li-ion batteries) still stands, though chipped away by a large number of advanced development projects attracted by booming prices

Cobalt mining - cobalt is another battery component and Chinese miners have secured a very strong position in cobalt extraction (70%) by moving early on in Africa

Lithium mining - an abundant resource worldwide, the basic metal has not been prioritized by Chinese miners - China's interests in extraction have been dropping from 13% (2019 estimate) to 7.9% according to a BP 2021 review

By prioritizing treatment of the raw materials over the mining ventures themselves, China's industry took advantage of lower labor costs, suitable environmental regulations and supply chain integration - late-coming competitors might catch-up over time, with delay

By refining of the metals for battery manufacturing - worldwide Chinese dominance has been achieved in rare earth (87%), cobalt (65%) and lithium (57%) - minority capacity in nickel (35%)

Battery production

Undisputed leader, CATL delivered 170,39 GWh in 2021 - from 2,19 GWh in 2015 and aims for 670 GWh in 2025

- A capacity gap of 390 GWh is projected by CATL on basis of future domestic Chinese and foreign markets demand

- CATL has launched manufacturing plants, in operation in Germany or in planning stages (Hungary, potentially North America)

BYD battery production, closely integrated its powerful range of EVs, is following suit

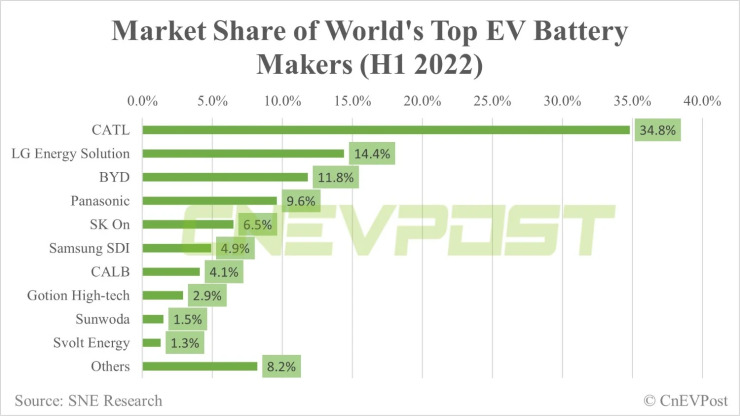

The Chinese battery makers increased their global market share to 56.4%

Market share growth in the first half of 2022 signals the first mover advantage detained by the industry, riding the wave of high-growth EV demand - and the barrier confronting Western late-starters

CATL's stake increased from 28.6% to 34.8%, BYD's from 6.8% to 11.8% and smaller Chinese firms are entering the top 10 - CALB (4.1%), Gotion High-tech (2.9%), Sunwoda (1.5%) and Svolt Energy (1.3%)

EV manufacturing

Actively supported at the provincial level, multiple car makers, drawn by accessible expertise, a strong supply chain and significant state support, have attempted to gain consumer recognition

Following a shake-up in the industry, dominant EV makers stand out on the domestic Chinese market (based on Jan-Nov 2022 estimate of plug-in electrical vehicles sales)

BYD stands out with 6 models in the top 10 sold in China - and 4 times the stake held by Tesla (7.6% - an outstanding achievement in its own right)

- source - insdiseevs.com

- BYD: 30.7% - with 6 models in the top 10 (November '22 ranking)

- SAIC: 10.8% including the joint venture with GM and Wuling

- Tesla: 7.6% - ranked n°4 with model Y and n°9 with Model 3 (November '22)

- Geely-Volvo: 5.5%

- GAC: 4.9%

- Chery: 4.2%

- Volkswagen Group: 3.8%

- Dongfeng: 3.8%

Riding a tiger

Production of electrical vehicles in China has expanded from humble beginnings (sales of 220 000 EVs in 2015) into a colossus (est. 6.4 million vehicles in 2022), all in less than a decade

Tight management over the supply chain and control over the bottlenecks are commanding the actual production capacity of electrical vehicles

- Majority stakes in basic materials and - even more significantly - in metal refineries insure swift response to downstream demand

- Battery production - key to added value of electrical vehicles, contributing approx. 40% to cost - holds a grip on EV market dominance...

...if Chinese industry can maintain its controlling share of a fast-moving market

.... a success warranted by solid dominance over metal refineries

.... buttressed by investments in battery manufacturing, staying ahead of demand and increasing global market share

.... with proven ability to deliver electrical car line-ups that are attractive, affordable and top-rated security credentials

Secured on the supply side, the challenges confronting the Chinese EV industry are likely to rise from competing demands

Red-hot growth of demand in China, powered in part by favorable subsidies, is a blessing, consolidating the industry's global dominance and generating potent economies of scale

Overwhelming in size, the growth of domestic demand could just as easily constrain China's priorities, crowding out EV exports, at a time of maximum opportunity as foreign demand catches up

How China is preparing to consolidate in the global market for electrification will be discussed in EVs Whirlwind