Batteries account for up to 40% of total cost of an EV, weighing on EV market penetration of the low-to-middle price tier of volume car sales, once subsidies are rolled back

Lithium is one of the key components and lithium-ion batteries are believed to offer the most energy density, lowest self-discharge, and longest useful lifespan

In the three most common battery chemistries, lithium is always present

- in LFP batteries - iron phosphate + lithium

- in NMC811 batteries - nickel, manganese and cobalt + lithium

- in NMC 622 batteries - with less nickel and more manganese and cobalt + lithium

However, while demand for EVs has been surging, lithium supply is lagging

Abundant in nature, mining and processing of lithium brine requires long term commitments

Investments focus on a small number of countries, leaving aside Bolivia, its largest global reserves at 21 million tons (est.) notwithstanding, because of political uncertainty

Chile, Australia and Argentina - in that order - control 75% of 'exploitable' reserves - followed by China, the US and Canada accounting for 13%

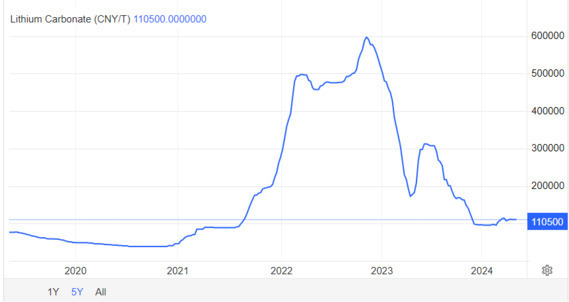

Lithium price volatility since early 2020 has been the market answer at the conjunction of uncertainties

For lithium miners, invested for the long term, current battery demand remains hard to extrapolate

- Demand of electrical vehicles (EVs) has been supercharged on the world's largest market, China, by a mix of regulatory constraints and subsidies - what 2023 will be like as subsidies fall away is uncertain

- Europe is following China's lead but will the consumers be eager to buy significantly more expensive vehicles, if (and when) subsidies drop back?

For car- and battery makers, speedy response to consumer expectations is of the essence

- Speculative buying of the metal, building up inventory - last year and probably in 2021 as well - has been the short-term answer to the carmakers' burning issue, how to protect market share from the onslaught of novel EV brands

With the growing interest in transport electrification only one of two things can occur

- Chinese carmakers, including Tesla

, drive down EV prices, come what may, to gain market share at the expense of margin - at least for the short time to achieve market dominance - Or alternatives to lithium-ion batteries come to market to lower the cost of batteries - and of the cars - dramatically

The future of 'Green Transportation' truly hinges on the cost of batteries

The future of the Western car industry hinges on the ability to compete effectively with Chinese EV imports in the base car pricing tiers

The confidence of the prestigious German car brands may not be as unflappable as it portends to be

Doubts might be creeping in with the decision to import part of the line-up from China, as the luxury brands are buttressed in no small part by the dual pillars of innovation and German thoroughness in manufacturing expertise

While the strengths of German cars are not in dispute, electrification has dramatically lowered the barriers to entry in a globalized car market, and across the entire price range

With much less brand protection, the competitive challenge is building quickly for the mid-tier legacy carmakers, exposed to price wars and with few factors of differentiation

While China-made ICE (internal combustion engine) motorization struggled and never truly convinced, Chinese EVs sold under legacy brands, or striking out on their own, are making their mark

The deeply integrated supply chain, build over the past decade by Chinese miners, battery makers and car manufacturers with active support of the government, has become a defining feature of the 21st century global car market

Recent blogs have reviewed the Chinese car strategy, its success in meeting domestic consumer demand and the exposure of Europe's car makers compelled by European 'Green' regulations to part ways with their ICE moat

January 2023 - China Electrical Vehicles - Logistics prevail - Innovative technologies, mass production and geographical outreach have advanced the ambitions of strong central authorities, followed in lockstep by their tradesmen, times and again in history

February 2023 - EVs in Demand - a Whirlwind - How, with its ability to deliver, the Chinese EV supply chain circling the world has been a model of demand anticipation

April 2023 - Europe Automotive - Treading Water - Arguing how the economics of the legacy car markers call for a balanced approach of motorization, combining electrical and hybrid motorization

When car makers overplay their hand

Legacy car makers have long put their trust in the strength of their brands

The industry was equally confident in its economic weight and influence

By contributing in large measure to employment in the industrial sector and downstream in services, the firms expected support at the national level in their home countries incontrovertible

Electrification might have been slated to become gradually a part of their line-up, probably at the higher end - and Tesla's emergence as 'bit player' strengthened this belief

Possibly amused initially by the wild trust investors were putting in the American firm, feelings turning bittersweet as its share price kept rising well beyond any sensible measure, the car makers in Europe may well have misjudged the political weight of environmental concern

EU members never shared love for the car industry on an equal footing

Foundational in Germany's enduring economic dominance and export strategy, still strong in France and in Italy for old times' sake, that love was very cool indeed in the Northern membership

At odds, or just distracted from probable social and economic consequences of the transition away from classic motorization, EU governments were drawn by the alluring attraction of EV modernity

Never missing a beat, environmental activism around the world has been as vocal in its advocacy for transport electrification as their cost-benefit analysis has remained vague

Laid down in absolute terms, wagering the planet had to be 'saved' at any cost, environmental goals have wrong-footed governmental policies times and again

Legitimate efforts to account for Green priorities in government kept drawing streams of condemnations, for being below the mark and 'never absolute enough'

In an awkward partnership with lukewarm European governments, the car industry has to make a stand on policies which might be understood by the ultimate arbiter, the general public, quite a mountain to climb

The ball is in the industry's court

The complexity of classic motorization used to constitute insuperable barriers to competition

By leveling the playing field in the near future, electrification confronts the car industry, and the all-important parts suppliers, with an existential risk

Transitory measures, sought in the short term by the European car makers, hinge by necessity on revamped existing ICE line-ups

Germany negotiated an exemption to the 2035 ban in Europe of CO2 emitting cars for vehicles running on e-fuel, a synthetic version of fossil fuel

The carbon-neutral e-fuels are generated from a mixture of hydrogen and carbon monoxide by applying renewable energy sources

On industrial scale, the process has not yet been proven sustainable and the conversion ratio from renewable energy (mainly solar) to fuel has yet to reach a target set at 20% efficiency

Stellantis

Requested by Fiat, the Italian car maker part of the Stellantis Group, an attempt to include bio-fuels in the German regime of exemption failed

And a push to include hybrid motorization in the post-2035 regime of cars approved for sale in Europe does not appear to be gaining traction either

The car industry is in a fight for its own survival and answers are not forthcoming

Retreat is not an option for legacy car makers

Or is it ?

Options are uncomfortably constrained and increasingly out of step with fast spreading adoption of fully electrical vehicles

Going down to the wire, the end game in the not-so-distant future will decide who - and where - electrical vehicles will be manufactured

In terms of range and innovation of the Chinese cars at the biennial Shanghai International Automobile Industry Exhibition which ended last Thursday April 27, 2023, conclusions are reported to be foregone

Quoting an April 27 report by MERICS

"European automakers faced a rude awakening ... as China’s EV champions displayed cutting edge models, from budget to luxury, while Chinese suppliers unveiled breakthrough technologies in EV batteries and more,” said Jacob Gunter, MERICS Senior Analyst. “With sizeable investments in China and shrinking market share, European automakers are under pressure to find new ways to compete in China and, increasingly, in their home markets against Chinese competitors.”

"Stand-out Chinese-made products on display in Shanghai pushed the envelope in terms of range, power and technology:

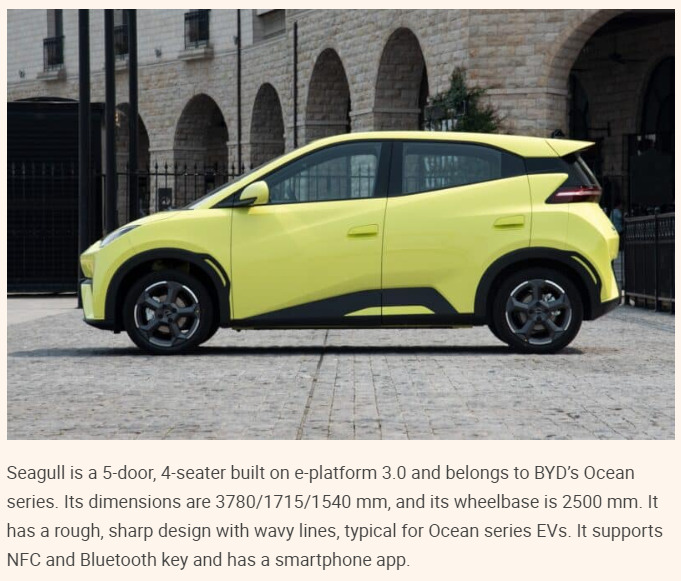

..the BYD Seagull, a full-sized sedan EV with a battery range of around 300 kilometers and a price tag of only USD 10,700; the luxury SUV EV U8 by Yangwang, a luxury brand developed by BYD, with independent motors allowing it to ‘tank turn’ and rotate on a dime; a sodium-ion EV battery by CATL, a cheaper alternative to lithium-ion, which is slated for use by EV maker Chery"

BYD

While innovative features will be met by legacy car makers, measure for measure, given the time..., competition has moved to price in the last few months, upending strategies the world over

Tesla

Whether the tactics will be enough is uncertain as the grip of Chinese car makers tightens on their home market (from 36% in 2020 to 50% in 2022), powered by the surge in sales of domestic EVs and hybrids, nearing a third of China's total new vehicle sales

Playing catch-up with their Chinese EV competitors, legacy car makers could be stopped in their tracks by the disruptive price strategies

EV prices are compelled to realign globally, closing the gap for Tesla cars which were up to 40% cheaper than in the US before adjustment.... and Europe's EV pricing will not be far behind

Disruption followed by more disruption ?

With EV competition pivoting on price in China, cost structures come in focus - again...

Competitiveness of Chinese manufacturers is a familiar trope and Tesla never missed an opportunity to vaunt the performance of its Shanghai plant, the firm's largest

However, in EV production costs, batteries used to be the elephant in the room, the defining component dragging the entire price structure along, at approx. 40% total cost

High battery cost was expected to put EVs out of range of the base car tier - the more affordable volume segment which remains critical to the legacy ICE manufacturers

Such assumptions may still hold true, but doubt is creeping in with the launch of sodium - ion batteries in Shanghai

Of perennial interest for battery makers, with a very large cost advantage over lithium, sodium-ion batteries - and sodium-lithium combinations - will, if the first mass produced cars announced in Shanghai prove successful, boost EV prospects across the entire price structure and turn ICE exposure upside down

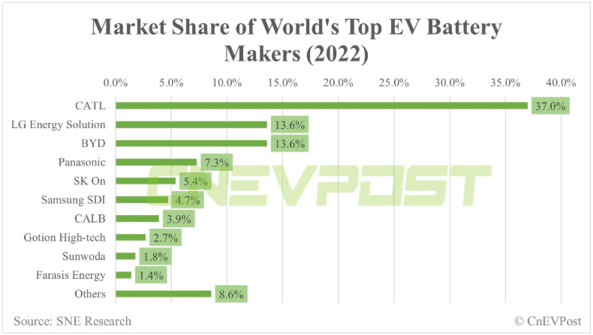

CATL, the world's largest battery supplier (with a 37% market share), experimented sodium-ion batteries since 2021 and announced the first large-scale assembly line in Ningde (south-eastern Fujian) in late 2022

Other pioneers in the field include Farasis Energy, HiNa Battery Technology and Sihao - New Energy who debuted their first vehicle installed with a sodium battery pack based on cellular battery technology in February

While causality should be interpreted with caution, the sharp reversal of lithium price run-up in November 2022 closely correlates with the announcements of industrial production of the new batteries for cars (and of the launch in December of the world's biggest factory for sodium-ion batteries for industrial purposes, with an annual capacity of one gigawatt-hour built by affiliates of Three Gorges in Fuyang - central China)

....no more than a coincidence if the reassuring statements by the mining industry - linking the sharp price drop to excess inventory of the metal and a slowdown in Chinese EV sales - are true

....but a sea-change, pressing the legacy car makers to take on fully electrified transportation much earlier than anyone could fathom

Compared to the lithium per ton prices - from a high of $84 400 last November 2022 to $23 000 mid-April 2023 - the price of sodium carbonate is just a percentile at $290 a ton

It is still early days - the durability of sodium batteries, the merits of mixed lithium-sodium - ion batteries and the repricing of lithium under pressure of such alternatives all need to be explored

However, an inflexion point in EV market penetration might be in sight...

What is more, in a singular reversal of fortune, the US has the largest reserves of sodium carbonate (soda ash) in deposits under the southwestern Wyoming desert, amounting to 23 billion metric tons (90% of world total of 25 billion)

As noted by the US Geological Survey, "relatively low production costs and lower environmental impacts provide natural soda ash producers some advantage over producers of synthetic soda ash"

Dampening expectations, CATL declared production on a large scale remained unlikely until 2024 or 2025 "due to a lack of raw material suppliers" - according to China's Yicai Global

As noted in the New York Times - April 12, 2023

With minimal natural reserves of soda ash and a reluctance to rely on imports from the United States, China instead produces synthetic soda ash at chemical plants fueled by coal. China’s synthetic soda ash industry has a record of hazardous water pollution....

Returning with a vengeance, geopolitical implications will be discussed in a follow-up note if - and when - the competitive advantage of sodium-ion batteries becomes demonstrably true