Russia holds the largest known natural gas reserves (24% of world reserves) and was also the largest exporter in 2021 with 227.1 billion cubic meters (bcm), shipped mostly by pipeline (83%) and Europe has been the indispensable customer for the past 50 years

Before the Ukraine war, 70% of Russian gas was exported to Europe by pipeline and an additional 7% by LNG transport

European gas reserves - said to be 85% and even up to 95% topped up - are expected to cover most of the winter months of 22/23, assuming weather remains fairly mild and demand subdued by high prices

However, concerns for 2023 are, as it should be, front and center

Russia may be fine with a large drop in gas volume sold at much higher prices

Europe is not - a large volume loss is simply impossible to manage

Natural gas pipeline shipments from Russia to Europe will be compromised for the foreseeable future

Volume export can be expected to drop substantially and a 100 bcm reduction in shipments incl. LNG to Europe (30% of total imports) could well turn out to be a base case (and hardly worse case) scenario for 2023

For Russia, there appears to be no way to compensate the 45% loss in total gas volume exports this base case implies…but sky-high prices will secure revenue in 2023, just as it does today

Diverting Russian gas

Alternative shipping routes do not measure up for Russia - at least in the short to medium term

The sole Power of Siberia pipeline to China will transport 16 bcm this year, increasing to 38 bcm by 2025 and a new pipeline to China – under discussion – 3000 kms (1 900 miles) long – will not be ready before 2030

China, Russia's preferred gas export market, remains keen for alternatives, LNG contracts with Qatar and negotiations with Turkmenistan for a Central Asia pipeline (bypassing Russia) for 25 bcm per year

In any case, Russian LNG shipments to Asia, to Japan and China, Taiwan and South Korea – a diversification President Putin has been favoring for years – cannot realistically go from 22.5bcm (in 2020) to double or triple the volume in the near future – for lack of infrastructure

A loss of exports of the order of 85 bcm assuming some additional LNG exports and increased Power of Siberia deliveries to China will be – seen from Moscow – the least bad outcome in the short term – a loss of approx. a third of total pre-war exports - well compensated in USD dollar or Russian Ruble terms

For Russia, the existential risk, however, is around the corner if its natural gas is marginalized on the world markets in the medium term, as a highly unreliable source of energy

It is safe to assume that global gas exporters will aim to gain market share

However, Central Asian gas exporters such as Turkmenistan and Kazakhstan are dependent on Russian pipeline delivery…as long as the purported Trans Caspian, circumventing Russia remains a pipedream – another potential loss for Europe if current exports are halted altogether

Qatar, Australia and the US remain geography-bound to the bottlenecks of LNG transport availability - while large fleets of LNG ships have been redirected from Asia to Europe in 2022, economic revival in China and South-East Asia might weigh on shipping allocations next year

Constrained in the short term, diversification by the major energy importers - Europe, China and other Asian countries - will drive energy markets for decades to come - away from Russia

European High-Wire Act

Balancing supply and demand with a 100bcm fall in Russian natural gas imports on European markets - 30% of total European imports and 55% of imports from Russia - is a high-wire act

Curtailing European gas consumption by 15% - in a combination of high prices and a degree of rationing would save 50bcm

- The Brussels-based research institute Bruegel showed big differences in the effort required of EU countries under this assumption

Pipeline deliveries in Europe from alternative sources are severely constrained by resource and production capacity limitations – a 20% increase in deliveries from Algeria (adding 7bcm to the 35bcm 2020 exports) and a 10% increase from Norway (adding 10 bcm to the 111 bcm 2020 exports) - are ambitious targets to deliver only an extra 17 bcm on European markets at best...

LNG shipments are dependent on re-gasification capacities (currently used at 75%) and transport by ship

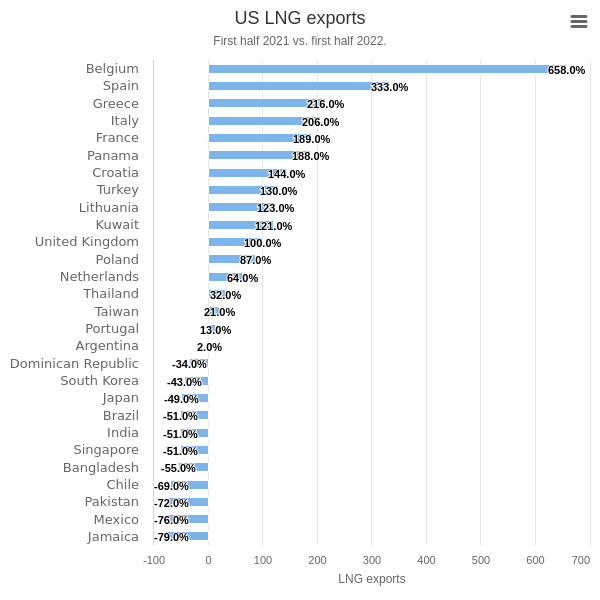

- US LNG proves to be an outlier - on track for volume increases of 100% over 2021, shipping 39 bcm to Europe in the first half of 2022 (from 34bcm for the entire year 2021), driven by benchmark prices at approx. 6 times the US benchmark - which could add 45bcm to Europe's gas imports for the year

- Because the dramatic increase comes at the cost of contractual deliveries to emerging markets, reliance on increased US LNG is not sustainable - rising prices in Asia, energy shortages and contractual obligations are expected to weigh on US deliveries in 2023

Consequences, dire consequences...for emerging markets, deprived of key energy resources

- Qatar is a key provider for Europe in LNG (24%) behind the US (26%) but its ability to increase exports from 30 bcm (2020) appears limited

- Asia remains Qatar's primary market (70% of its LNG exports) and firm commitment to its long-term contracts cements its reputation of reliable provider

- The lack of spare capacity constrains any short-term significant increase in gas deliveries - before new capacity investment could allow a potential contribution to European diversification by 2024 / 2025

Conclusion

Under current natural gas delivery estimates in Europe – it appears impossible to balance a partial embargo on Russian natural gas in 2023 in a base scenario of a 100bcm

- The US LNG export may - or, more probably, may not - maintain in coming years the exceptional level of exports to Europe, expected to reach 75 bcm in 2022, over the previous baseline of 34bcm. If anything, volume exported to Europe is likely to fall back substantially

- Norway - Europe's second most important gas resource - has limited spare capacity - export increase is optimistically estimated at just10bcm

- Algeria may not rise much beyond its traditional markets (Spain and Italy) for lack of investments in production capacity, with export increase (if any) coming at the detriment of domestic needs

There is little doubt that current gas reserves, supported by current LNG imports, will cover consumption during the 2022-2023 winter

However, little additional flexibility in LNG deliveries should be expected from any non-Russian provider going into 2023

In 2023 and for later years, the only real variable is a reduction in European gas consumption, a little advertised fact

....and a driver in the scramble of every European government seeking contractual commitments from Qatar (Germany), Algeria (Italy, France) or Egypt (Italy, Turkey)

As long as prices stay high (and they will) and gas availability ex-Russia constrained, President Putin will keep running the clock…in 2023 and beyond

This analysis relies mainly on data prepared by the BP Statistical Review of World Energy 2021