Russia’s influence over European energy policies has been shaped by 50 years of close engagement between German energy conglomerates and Gazprom, the Russian gas exporter

This has been the fruit of German Chancellor Willy Brandt’s Ostpolitik in the 1970’s, a political gambit to draw the USSR out of economic isolation and, by raising the Iron Curtain of the Cold War, to put Germany back at the center of the European landmass, stretching from the Atlantic to the Ural Mountains

Overcoming much vocal criticism from the U.S. for pandering with the enemy, and reluctance of the old Communist guard at the Kremlin, the strategy was quite successful and mutually very beneficial

Europe, and foremost Germany, gained access to a nearly bottomless supply of energy to power its industries and to heat European homes

Russia benefitted to a considerable extent from Western gas extraction and compression technologies, pipeline tubbing equipment, and the financing of the whole enterprise

Built on trust tying professional relationships between the German energy majors and Gazprom, energy became, one step at a time, a unique model of East-West collaboration, well before the fall of communism and dissolution of the USSR

Stretching over half a century, the trust – and the long-term contracts defining the commercial relation – were bound to be challenged over time

Technological advance, liberal economic thought and the rise of new potent energy markets in the East chipped away at original certainties

However, confidence in an energy policy which had become a standing partner of the European consensus was hard to shake, further strengthened by the vast network of pipes crisscrossing the borders from East to West

Ultimately, it turned out, the grid was tethered to evolving geopolitical interests like any other international construct, which is only as strong as mutually shared benefits

With the war in Ukraine, alignment came to a screeching halt

To make sense of the upheaval on the European gas market, the immensity of the enterprise engaged by visionary leaders in the energy sector of the USSR needs to be recounted

In a top-down command system, a few individuals could advance – or push back for a generation – energy policies which, as it turned out, provided the country with the hard currencies needed for its modernization, on a scale that only became clear over time

Men like Aleksey Kortunov, as founder of the Soviet gas industry and Sabit Ataevich Orudzhev at the Ministry of Gas (which was to become Gazprom) took on out-worldly challenges in Western Siberia, at the heart of the gas fields

Keeping energy politics apart from Cold War aggression...

Mr. Weiss, Austrian minister of transportation, and Russia's energy czar take a first tentative step in a promising partnership, just 10 days after the invasion of Czechoslovakia by the Warsaw Pact (Aug. 1968)

Lacking the 1420-millimeter piping required for gas transportation, the compressors to push the gas along over thousands of kilometers, the technology and the finance, Mr. Kortunov started out with a vision...and a blueprint

Every piece of equipment was to be delivered by Germany and the cost of these vast investments repayed over time ...in gas, indexed on the existing European price structure - a barter agreement opening lofty vistas for the partners

Building six trunk lines to Eastern Europe, employing 20 000 kilometers of pipe, confronted inexperienced pipe layers with one set of problems upon another…

As recounted in Thane Gustafson's history of natural gas, swampy soil required delivery by barges in summertime, special tractors to pull the piping through deep snow over roads made of ice in winter, refrigeration as the gas comes up hot from the wells before flowing through pipes running above ground, to prevent melting the permafrost and on and on…

Ties that bind

From very modest yearly exports of natural gas in 1970 (3.3 bcm - billion cubic meters) meeting explosive demand in Western Europe – 25.7 bcm in 1975 – to 155 bcm in 2020 (part of 227 bcm global exports) from Russian fields alone (not counting Central Asian producers), energy politics quickly became central to Soviet government, as it remains to Russia today

The future cannot be very different...for now

Grandstanding – on the Western side to gain ‘independence’ from Russian energy – and on the Russian side to curtail energy deliveries to ‘unfriendly’ countries – misses fundamental complexities and the central issue, time to implement alternatives

In the short term, neither party can do without the other

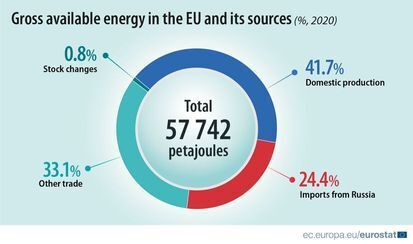

Energy sourced from Russia is predominantly natural gas (155 bcm represent 46% of its gas imports), followed at a distance by oil (26% of EU oil imports) and by solid fossil fuels (such as coal) for 19%

Shortfalls and dependency - a mixed lot

Based on 2020 data, statistics provided by energy major bp record the shortfall, in billion cubic meters of gas (bcm)

The large gas consuming nations have good cause - the UK, the Netherlands and Ukraine nurtured industrial and household addiction to their domestic gas production - and Germany along with Italy were the most preeminent beneficiaries as founding partners of the vast Russian energy export effort

The 50% contribution of Norway to European production stands out

| in bcm '20 | Production | Consumption | Shortfall |

|---|---|---|---|

| Europe | 218,6 | 541,1 | -322,5 |

| Norway | 111,5 | 4,4 | 107,1 |

| UK | 39,5 | 72,5 | -33 |

| Netherlands | 20 | 36,6 | -16,6 |

| Ukraine | 19 | 29,5 | -10,5 |

| Germany | 4,5 | 86,5 | -82 |

| France | 0 | 40,7 | -40,7 |

| Italy | 3,9 | 67,7 | -63,8 |

| Spain | 0 | 32,4 | -32,4 |

| Turkey | 0 | 46,4 | -46,4 |

| bp Statistical Review of World Energy (ed. 2021) | |||

About two-thirds of natural gas imports are delivered to Europe by pipeline (211 bcm) and one third by LNG transport (114 bcm) - Russia delivered 155 bcm in total

Dominance of the Russian stake in European gas imports (46%) is weighed down according to Statista by

- three large gas-importing countries - Germany (49% of its supply), Italy (46%) and Poland (40%)

- highly dependent countries : the Baltics (incl. Finland) and the Balkan States - in the 90-100% range

With low dependency rates, the UK (3-5% Russian imports) and the Netherlands (11%) benefit from significant (albeit dwindling) domestic gas production, as is also the case for gas producing Romania (10% dependency) and Ukraine

France (24% Russian-dependency rate) relies on nuclear energy and Algerian gas

Russian gas imports are also small and declining in countries with attractive alternatives - Ireland (0%) served by UK interconnexion delivering North Sea and Norwegian gas, the Netherlands and Spain with access to LNG deliveries from Qatar and the U.S.

Ambiguities of gas dependency

On average, across the European Union, the residential sector accounts for most gas demand (40%), followed by industry and gas use for power generation

Industry consumption, at 28% of gas demand by our approximation, has declined by 20% since 2000

In the same period, gas use for power generation has been rising, accounting for 26% of gas demand, also by our approximation

Driven by environmental targets, the EU’s economic transition from industry to energy services, and the structural changes in the energy-intensive industry, have been weighing on industrial priorities, consumer demands and governmental arbitrage

Under market stress, these trends will - in all likelihood - play out very differently from one country to another

Concern - or reassurance - voiced by European governments about their respective dependency rates omits the flexibility of interconnected gas pipelines, rebalancing access to gas by reverse flow across the networks between countries and diversifying the origins of supply

Depriving Gazprom of its bargaining power with individual countries, grid integration is part and parcel of the single European energy market

Ukraine has relied on European reverse flows since 2015, bringing direct shipments from Russia to 0

However, In case of brutal supply curbs, reverse flows, potentially a redistribution of gas supplied to the network, cannot be expected to rely on market forces

The gap between constrained and volatile gas supplies on the one hand and pressing demand priorities on the other will simply be too wide for market pricing to reset allocations

...derived from sky-high prices, such allocations will benefit no one, except the Russian supplier of course

The hard choices to align supply and demand of energy have not really filtered through in public awareness

Environmentally friendly schedules of disengagement from fossil fuels and from nuclear energy have to be reset on the supply side, to compensate for much constrained gas shipments, and demand of energy needs to be contained

...to be discussed in a forthcoming 'Test of Wills'

Countering aggression on the European borders has a price

Willingness in Europe to shoulder the pain will be heard loud and clear...in Moscow