In Target2, the cross border settlement system, we explained how imbalances are inherent to an imperfect, and decentralized, monetary union and how extraordinary action by the European Central Bank (ECB) compounded the distortion

Broadening our perspective, underlying factors of Target2 imbalance in the Eurozone are indicative of systemic vulnerability, superseding the frailties of a decentralized monetary union

The most likely actions the ECB will deploy over time can be construed from the analysis

The systemic vulnerability of Target2 balances

Intra-system balances – such as Target2 – are inherent to the Eurozone decentralized monetary union, where banks may and often do have central bank accounts spread across different central banks

Until 2008, a decline in client deposits at a bank confronted with more cross-border payments than deposits usually relied on interbank borrowing, with little recourse to Target2 refinancing by way of the Central Banks

Losing access to the interbank markets in a climate of insecurity and mistrust during the financial crisis, the banks turned to the financing made available at the ECB

However, the recourse to the Target2 window to refinance cross-border banking transactions had a cumulative effect, resulting in considerable imbalances in the accounts of the ECB

In practical terms, a bank or subsidiary of a bank located in the Eurozone (outside Italy) will sell an Italian government bond and prefer to deposit the receipt in one of the 3 countries above, but not in Italy …effectively increasing the liability of the Banca d’Italia and the assets of the beneficiary National Central Bank (NCB)

As noted by the ECB, in the Sept. 17 bulletin on Target balances (p.18/49)

the market for financial services in Europe is integrated such that securities holdings and transactions are not limited by national borders. As a result, the securities purchased by NCBs are, more often than not, sourced from counterparties located in another jurisdiction

The systemic vulnerability in cross-border settlements – and the determinant of the imbalances – can be subsumed in the choices of multitudes of individual investors, who simply prefer to hold their Euro accounts in Germany, the Netherlands or Luxemburg (all 3 with positive Target2 balances) and not in Italy or Spain (both with largely negative accounts)

Build-up of Italian and Spanish liabilities

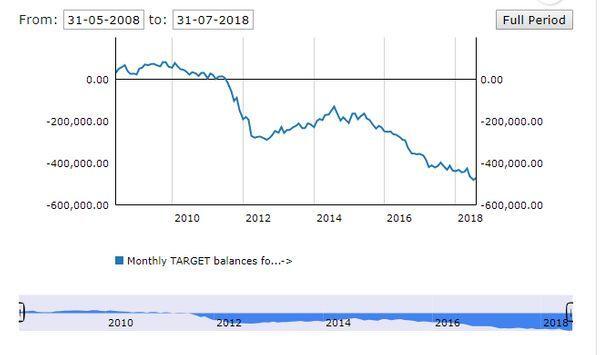

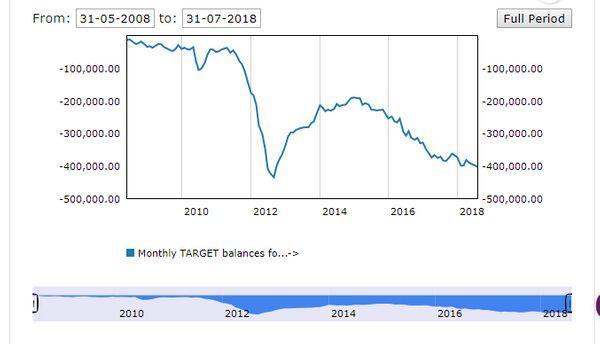

Liabilities started building up for Banca d’Italia from July ’11 – increasing to € 280bn by July’12

Liabilities at Banco de España, already significant in July ’11 (€56bn) worsened sharply to €434bn by August ’12 before easing

Imbalances during the sovereign debt crisis (2011/2012) had similar causes in Italy and in Spain, driven by

- foreign sales of Government bonds

- foreign withdrawal from interbank lending to Italian and Spanish banks

The ECB recognizes that TARGET balances increased as Eurosystem funding, provided during the sovereign debt crisis, was demand driven and subsequently flowed from vulnerable to less-vulnerable countries in the context of severe market stress – i.e. from Italy and Spain to the Bundesbank account at the ECB.

Capital flight by another name...

The Target2 balance of each country eased from early 2013 as the banks started to repay the loans, borrowed from the ECB under the so-called Longer-Term Refinancing Operations (LTROs), reducing liabilities to €165bn for Italy and €190bn for Spain by early 2015

Another lurch into deep liability territory is correlated with new Central Bank actions, aiming at increasing liquidity through ‘non-standard’ asset purchases by the ECB

- Launched in June ’14, cheap financing through targeted longer-term refinancing operations (TLTROs) benefited periphery banks disproportionately; banks in Italy and Spain account for over 60% of TLTRO holdings

- Introduced in March ’15 with the objective of sustaining growth, the public sector purchase program (PSPP), expanding asset purchases to sovereign bonds, drove liabilities of the two countries much higher; sales by foreign holders of Italian and Spanish public debt securities boosted the liabilities for both central banks

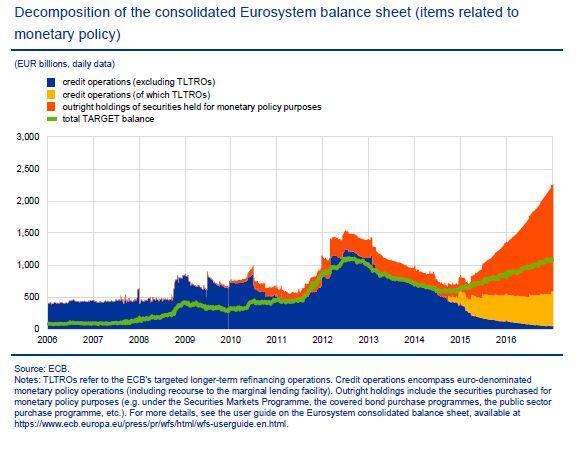

Insisting the policy was predominantly supply-driven, resulting from asset purchases by NCBs and the ECB rather than stress-related recourse to refinancing operations, the ECB’s September ’17 Bulletin on Target2 balances confirms

Around 80% of all security purchases by volume have been from non-domestic counterparties (i.e. counterparties located in a jurisdiction other than that of the purchasing central bank, including other euro area countries), while around 50% of purchases by volume have been from counterparties that are resident outside the euro area, most of which are concentrated in the UK

The decomposition – though dated from mid-2017 – is indicative of the global impact of the monetary policies on total Target2 balance

Fragmented financial markets

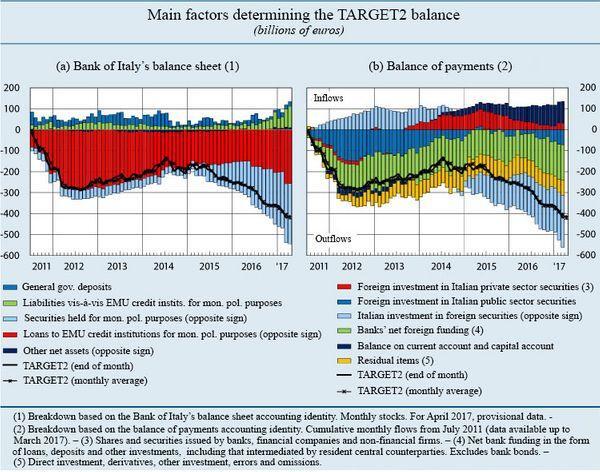

Each country’s Target2 balance is the net result of a variety of cross-border financial transactions (both incoming and outgoing) carried out by banks, governments and the non-financial private sector

The decomposition of the Italian balance of payments (as of April '17) highlights trends which are broadly representative of the Eurozone periphery

Paying special attention to the main factors of the balance of payments decomposition (right hand chart)

- foreign funding of Italian banks (green lines)

- (Italian) residents investing in foreign securities (light blue lines)

- foreign investment in Italian sovereign debt (dark blue lines)

the study of Banca d'Italia highlights the cumulative effect of the main drivers and places the technical explanation of the ECB, linking growing liabilities in peripheral countries to quantitative easing and excess liquidity, in a broader context

Quoting Banca d’Italia,

The widening of the TARGET2 debtor position reflects the decrease in Italian banks’ foreign funding and the rebalancing of residents’ portfolios towards assets other than Italian government securities and bank bonds, which has gone hand in hand with increased asset purchases and liquidity injections on the part of the Eurosystem

Foreign funding of Italian banks (green lines) has sharply decreased, in relation (at least in part according to Banca d'Italia) to ultra-low rates offered by the ECB induced systematic refinancing by the domestic bank system

Foreign investment in Italian sovereign debt (dark blue lines) clearly took advantage of the PSPP program of quantitative easing to sell holdings on a regular basis from March '15

- the monetary policy of the Bank of Italy faclitated these transactions with the purchase of government bonds from private investors, accounting for sales €90bn by April '17

But the main determinant of the sharp deterioration of the Target2 balance from early 2015 has been the non-financial private sector - and the same reallocation by private investors holds for the increased Spanish imbalance

(Italian) residents investment in foreign securities (light blue lines) – non-financial private sector and Italian households – have (in the words of Banca d'Italia) shifted portfolios investment from government securities and bank bonds towards insurance and asset management products. Returns on government securities are lower as a result of the Eurosystem’s asset purchase program. Bank bond placements have also decreased. Households are turning to insurance companies and professional advisors to invest their savings in mostly foreign assets.

- the reallocation to foreign bonds, mutual funds and shares has been marked since early '15 and the trend remains certanily unfortunate because the marked preference of Italian enterprise to invest abroad rather than in the Italian economy stands out. We are not aware of studies updating the trend since April '17

Target2 Italian imbalance, which grew €247bn from February '15 to €412bn in April ’17 in the Banca d’Italia study, remains on an upward trend, increasing to €470bn in July ’18

We do not know if the trends observed over 2015-2017 are continuing into 2018 but the assumption stands as there has been no policy change inducing a reversal

Indefinitely extended in time, such trends might ultimately support the logic of requalifying liabilities as debt (not accounted for in debt/GDP estimates today), the argument of capital flight or of stealth bail-outs

But what all 3 major factors affecting Italan (and Spanish) Target2 liabilities is an interest rate repression, leading both foreign and Italian investors to conclude that reasonable risk on the Italian economy is not correspondingly rewarded

Walking a fine line between a fragile banking system which requires support and a rate policy which recreates inter-bank lending and renewed interest in Italian debt, the ECB can be expected

- to encourage the long- overdue restructuring of the Italian banking system

- to tone down its purchase programs, not only halting further increase (as annouced for December '18) but withdrawing cautiously as bonds mature

Another - complementary - approach which might gain traction could focus on growth initiatives, financed by long term bonds, priced to attract italian as well as foreign investors and financial engineered with a partial ECB guarantee. As a pathway to return liquidity to Italy and reduce its liablities at the ECB, these 'no-name' euro-bonds might put German misgivings to rest....

In sum, Target 2 imbalances do not signal so much fragmentation as a dysfunctional financial market where growth projects are not supported and stimulated and where risk is not properly priced-in