Globalization has been viewed in terms of mutually beneficial trades for as long as most economists can remember

I will argue that this time, things are indeed different

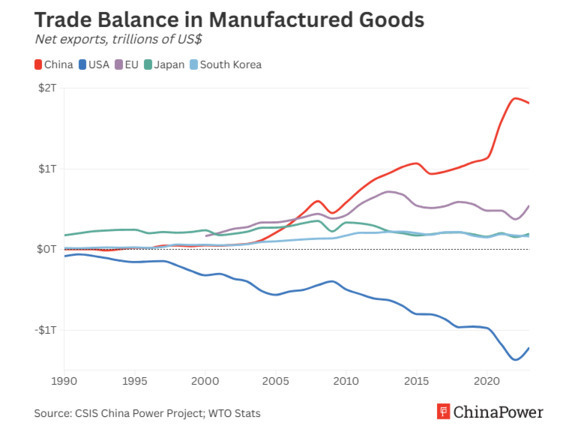

Staying on course gets harder with a China trade surplus in manufacturing goods surpassing $2 trillion, double the 11-months 2025 widely reported $1 trillion in total trade surplus which accounts for imports in commodities such as oil&gas and food

David Ricardo (1772-1823)’s concept of comparative advantage has laid the groundwork for international trade, entrusting each country with production of the goods for which it is most efficient

The corollary is that an efficient country leaves to others countries the production of goods for which it is less efficient

The requisites of global trade frame the evaluations by international organizations about the growth outlook and the financial stability of individual countries

When nations use their exports as potent drivers solely of their own growth, country-based recommendations are muddled and global stability is at risk

This is what 'mercantilism' is about

In its global setting, international trade has gone astray

Individual countries feel entitled to drive their economic growth with exports to support their industries ‘no holds barred’ – indefinitely and in ever increasing volumes

By manufacturing at huge scale and with unstinting national support, mercantilism 2.0 collapses Ricardo’s ‘comparative advantage’;

The underpinnings of global balance in international trade are displaced by the ‘survival of the fittest’, that is by "no rules at all"

As long as export giants, such as Germany, Japan or China, found willing counterparties to import their goods, namely the U.S. and euro-zone countries, uncomfortable arrangements kept chugging along

After remaining ‘manageable’ for so long, rising imbalances caused by mercantilism raise hard questions

- Is the risk in upending the foundational rules of international trade terminal?

- What are the consequences of roiling global trade when giant economies, namely China and the U.S., ignore these rules for their own benefit ?

- How are the countries holding on to principled trade regulations supposed to respond ?

These weighty issues can be framed in brutal simplicity

The cost in undermining the foundation of global trade will be - in the medium term - unbearable for all, including China and America

The countries most exposed to the aggressive Chinese and American trade policies – namely Europe and the global Emerging South – will have to act in support of the International Trade Organizations, the World Trade Organization (WTO) and the International Monetary Fund (IMF)

With policies reinstating shared responsibility in rebalancing global trade, there is a fighting chance to save international trade and the raison d'être of International Organizations

Global trade, losing out to national interests...

According to the IMF’s description of its own policy advice, specifically at the global level, all should be well

“A core responsibility of the IMF is monitoring the economic and financial policies of member countries and providing them with policy advice, an activity known as surveillance. As part of this process, which also takes place at the global and regional levels, the IMF identifies potential risks and recommends appropriate policy adjustments to sustain economic growth and promote financial stability”

It is easy to accuse the Fund of grandstanding when naked power bullies the IMF consultants into submission – no one wins, except the bully

Case in point, the 2025 Article IV Mission to the People's Republic of China, dated December 10, 2025, summarizes recommended measures to support domestic consumption and to reduce external imbalances (technocratic mumbo-jumbo for wild export surpluses in manufactured goods exports)

By focusing on economic growth (adopting the highly disputable over-estimation of 5% for 2025 of the Chinese authorities), the IMF lets the fox out of the henhouse...

The priority given to domestic consumer-led growth has been the mantra of Chinese officials for a long time and the IMF is treading the line knowingly : nothing much is in fact happening

Duly mentioned, the ‘reduction’ in external imbalances is in a supporting role - a perfunctory reminder in the face of explosive - and unaddressed - surpluses

The IMF is in a bind

To sustain economic growth of member countries, exports are part of the tool-kit and surpluses are recorded as 'a fact of life', not to be acted upon

Member countries are being monitored individually but global impact of the trade imbalances is only considered indirectly

And the power of dominant economies, commanding special IMF prudence, cannot be restrained, not just in China

- The U.S. Article IV Mission report for 2025 could not be found on line – the highly positive 2024 report was published in July 2024

Is free trade dying by a thousand cuts ?

The foundational rules have always been interpreted with a degree of flexibility

Mercantilism, in the form of more or less egregious national support to exports, is not new

Creeping tolerance, justified in any international organization relying on a broad consensus, can outgrow its guardians and become its own finality

Obvious, ‘in-your-face’, abuse of the international trading rules by the Trump Administration has brought home the old truth that "might is right"

Justified by the strongly asserted policy of re-industrialization of America, all-around taxation of imports already is taking on a life of its own, with nascent political acquiescence for protectionist measures of indefinite duration

A death knell of free trade is looming, at the hands of its former most vocal American supporters, the Republican politicians

The call is out...

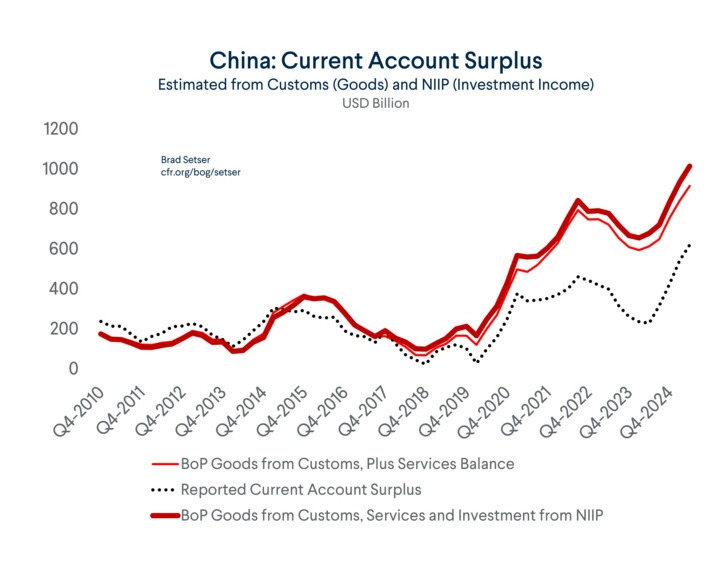

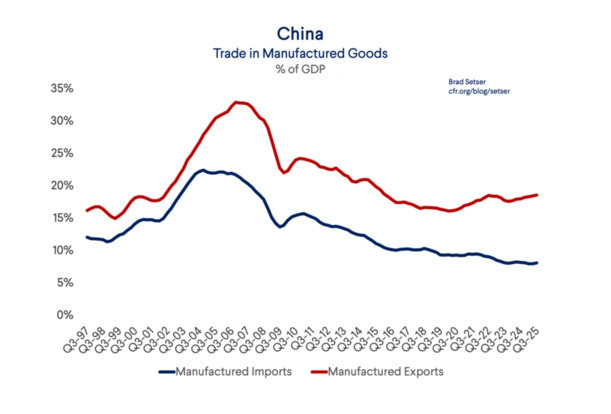

Reading China's Balance of Payments

As analyst Brad Setser explains on his blog at the Council on Foreign Relations, China’s GDP statistics are widely thought to be, well, works of performance art

In trade statistics, and regarding the all-important surplus, Chinese customs statistics of imports and exports check against the data reported by China’s trading partners (importers)

However, customs statistics do not correlate with Chinese balance of payments (BoP) records, published quarterly

The gap between the customs surplus and the current account surplus was large in the first half of 2024, dipped in the second half and in the first quarter of 2025 before widening again in Q2-2025

Noted by Mr. Setser, in a mild-mannered understatement, swings continue to impede clear measurement of the scale of China’s internal imbalances and contribution to global trade imbalances...

My assumption is that the customs surplus could be impacted periodically by the build-up of security stocks in commodities (such as energy and food), which the BoP data proceeds to smooth out

In a country’s BoP, the current account records the value of exports and imports of both goods (visible trades) and services (invisible trades) and international transfers of capital (net income from foreign sources and direct payments)

To minimize the visual impact of Chinese BoP surpluses on global trade, China adopted a new methodology in 2021

- raising BoP imports by bunching the cost insurance and freight with the goods (instead of accounting the costs to Services)

- making occasionally complex adjustments from the activities of multinational companies, and to the all important "Apple" trade

- running a deficit in foreign investment income of holdings topping $4 trillion, by ignoring (?) the former computation of flat 3 % return on foreign debt assets and an 8% return on foreign equities - and reducing the financial account surplus (by a lot)

With the methodology of 2021, the gap between reported Current Account surplus and Customs data reached approx. $400 billion in late 2024

- according to customs, the trade of goods & services surplus was recorded at just under $800 billion dollars (a $1000 billion goods surplus and a $225 billion services deficit, almost entirely from tourism)

- under the 2021 ‘methodology’, the China surplus shrunk drastically by half, to $400 billion, in 2024

Despite all the detailed forensic explanations, provided on Mr. Setser’s blog, the conclusion is brutally straightforward – Methodology is a matter of policy, which will not be discussed

By stonewalling on BoP methodology, the Chinese trade authorities secured the sole data set on which international financial institutions rely to make forecasts of China’s economic growth

And, even more significantly, by 'downsizing' the trade surplus while accounting for a growing GDP, China keeps a lid on an all-important IMF ratio - the current account balance in a percentage of country GDP

In the statistics of global imbalances for 2024, China's current account surplus - as a share of GDP - seemed to fade away, at 2% of GDP, below South Korea and Japan (above 5%)

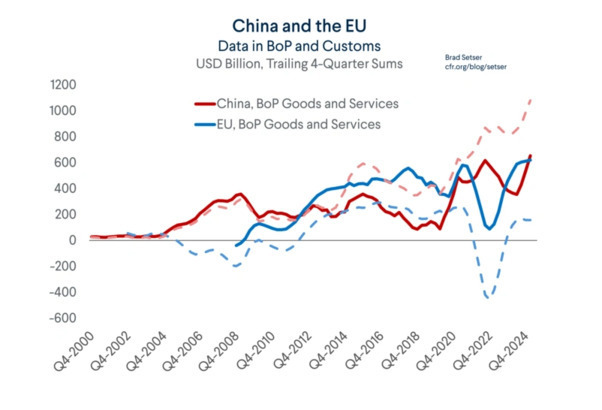

With the surplus 'downsized' and the GDP 'boosted' by dubious growth statistics, China offered the IMF a 'face-saving' escape by aligning - by the numbers if not in fact - with the European Union's BoP surplus

In official statistics, China’s BoP goods and services surplus of approx. $650 billion ended up just slightly above the EU’s surplus (approx. $620 billion) in 2024

Customs tell a very different story

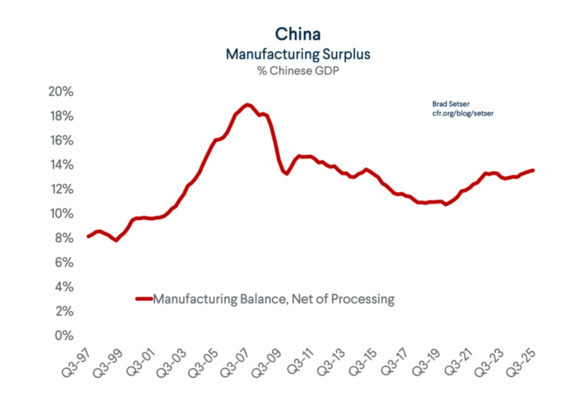

China's two trillion dollar manufacturing goods surplus

Mr. Setser extensively researched the growing discrepancy between trade statistics recorded by Chinese customs authorities and the data entered for record in the Balance of Payments

Extensively reported by commentators for its size, the rising total trade surplus, which surpasses $1 trillion over 11 months of 2025, does not signal the true extent of the trade imbalance on manufactured goods

It is with the surplus in manufactured goods and not in the broader grouping of ‘Goods’, that the magnitude of China’s challenge to global trade comes to light

China produces approx. 30% of the world’s global manufacturing added value, but domestic consumption accounts for just 18%

Data measures appear broadly consistent, even though the years of reference differ

- World manufacturing output for 2023 was $16.177 trillion

- In 2024, the total value-added industrial output in China reached about $5.65 trillion

Driven by its export-focused policies, vast capacity, and weak domestic (and import) demand, the consequences are foretold

Exports to foreign consumer markets are picking up the slack

In Mr. Setser’s and Commerz Bank’s Volkmar Bauer’s estimates, China's manufactured goods surplus exceeds $2 trillion, 10.5% of China GDP and 2% of global World GDP

- 10.5% of China GDP of $19.4 trillion would be $2.04 trillion

- 2% of global World GDP of $117.2 trillion projected by Statista in 2025 would be $2.34 trillion

- 5% of China’s Manufacturing GDP (Q3-2025) of $16.177 trillion world manufacturing GDP (UNIDO estimate Q3-2025) would be $1.7 trillion

What is to be done ?

Quoting Lenin's 1901 pamphlet setting out a roadmap for the Communist movement, the question is as existential in today's quite different context

Considering the magnitude of China's challenge, responses on the markets most at risk, and especially in the euro-zone, have been disorderly, confused and hesitant

- The members of the European Union must confront hard alternatives but they are not alone - the U.S. cannot hope to remain aloof .... and emerging markets, with their own growth ambitions at risk, should not be ignored

- The economic argument for trade based on comparative advantage cannot make sense much longer when one country, China, is nurturing this advantage in every segment of manufactured goods

- The creeping - but relentless - aggression of the Chinese yuan points to a major currency realignment

These issues (and many others) might bring China to the negotiating table in a rejigged mandate of the International Organizations, today well on the way to irrelevance

I optimistically hope to discuss these projections soon....