Long in the making, the projection of Chinese commercial power in the global automotive sector is unlikely to be side-tracked

'Car Electrification - Ties that Bind' hinted at the roadblocks Western legacy carmakers are encountering at every stage of the EV revolution

'China Electrical Vehicles - Logistics prevail' discussed the fine-tuned Chinese supply chain for electrical vehicles (EVs)

'EVs in Demand - a Whirlwind' highlighted the growth potential of the European EV market, straining the (mostly Chinese) production capacity globally available today

The commercial strategy of the Chinese car industry, in times of great risk for Western carmakers, is discussed in this note

With breathless reporting about Tesla's

Case in point....

Chinese car-and battery-maker BYD

Tesla's global sales in 2022 were of 1.3 million cars (+40% over 2021 sales)

The valuation of Tesla, however, was six-times BYD's ($625 billion vs. $100 billion), as of March 6, 2023

The deck might be reshuffled soon

Winner takes all ?

Industrial planning for world dominance

As case study of China's structured approach to industrial dominance, the supply chain has been battle-hardened with the creation of a large domestic market for EVs, a springboard to conquer export markets

Fit to purpose, an intricate web of mutually supportive entities has shouldered the considerable financial risk ...

...launching a novel industrial enterprise based - originally - on a fledging grasp of technology and paucity of consumer awareness

- articulate at the public levels of State and Provincial governments

- inclusive of state-owned and private enterprises

- mixing subsidies and access to bank capital

- framed by unstinting regulatory inducements

The great success encountered on the Chinese market has been commensurate with the audacity of the industrial plan

The EV line-up targeting the Chinese consumer, covering from the start the widest range of price points and boosted by subsidies and regulatory inducements, has blown past expectations

Market adoption rates targets of EVs in China - 25% by 2025 - were exceeded 3 years early - in 2022 - with domestic sales close to 6 million cars, an estimated 28% to 30% share in total sales of 20.6 million passenger cars

As it turns out, to establish a strong global presence, the industry's best laid-out plans might be constrained by booming Chinese domestic demand

By crowding out potential exports building on very strong interest in Europe, growth on the domestic Chinese market could hamper the roll-out of China's global ambitions

A matter of timing

Caught off guard by the highly successful domestic market penetration of electrical vehicles, China's vaunted supply chain might operate under unusual strain and uncertainty

Extending the current rate of EV sales growth for 2023-2025 in China as suggested by the industry analysts at Bloomberg New Energy Finance might double sales to 10/12 million EVs - a market penetration reaching 50%

This may prove over-optimistic but none of the Chinese carmakers, foremost BYD, SAIC and Tesla, wants to gamble on more conservative assumptions and loose momentum

There is no doubt that domestic sales of electrical vehicles, after incentives to buy EVs were sharply reduced in China in January, will be studied closely in the coming months

Building up production and driving sales with deep price cuts, these manufacturers are on a warpath, playing defense of their market share in China at any cost

Presumably, pressure on the upstream supply chain is already building

- According to company announcement, BYD reached in 6 months (as of November '22) a milestone with total sales since launch of the brands of three million new energy vehicles on the road, showcasing a massive “acceleration” in the EV industry

- Although exponential growth of EV adoption rates in Europe may be tempered by falling subsidies (in Norway or in Germany), European automakers need to stabilize their brands' market share by delivering electric vehicles, as soon as possible and in numbers, in a race to the finish (by 2035)

Pressure on the supply chains might go up and up, unrelentingly...

There will be no letting down...if exports to Europe take off as the Chinese planners are hoping

China's window of opportunity

In Europe, the key global EV market in terms of growth, regulatory inducement and charging station investments, the stakes could not be higher

Reporting globally on the 2025 EV market, industry analysts at Bloomberg New Energy Finance (NEF) project worldwide sales of 20.6 million EVs (6.6 million in 2022)

Europe and China are expected to account for 80% of all EV sales globally

- In Europe, adoption rate could double by 2025 from 20 to 40%, raising sales of a mix of mainly battery-powered EV, complemented by hybrid PHEV, to 4/4.5 million cars

- China, on current red-hot consumer EV momentum, might command 10 to 12 million EVs in 2025, implying an adoption rate above 40% as well, if the country stays the course (forecasting sales of 6 million EVs in 2022 on total sales of 21.5 million cars)

What is more, China could be manufacturing 60% of global electrical vehicles sold - between its home market (40%) and exports to Europe and (marginally) to the US

To challenge legacy car makers in Europe, China's electrical vehicle exports will be taking full advantage of broad line-ups targeting the mid-price range, of integrated supply chains and - not least - of cost

The many strengths of commercial EV roll-out

Long in the making, the line-up of electrical vehicles 'made-in-China' has been checking all the boxes of a frontal assault in Europe, on the world's largest car market (besides China itself)

Learning the hard way from the failure to make a mark in Europe in 2007-2008, the industry strived to improve design to consumer liking and to meet the most stringent safety expectations

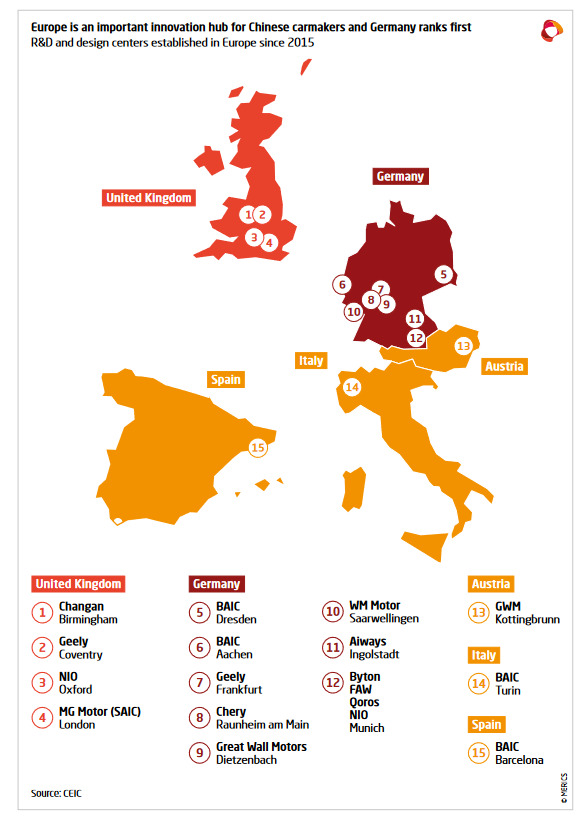

Since nothing beats learning from the locals, the Chinese carmakers established R&D beachheads in Europe

In a 2021 Merics report, no less than 15 different centers were located in 5 European countries - with very strong presence in Germany (8 locations)

The strategy is straightforward - winning over European drivers and large corporate customer fleets - with more affordable cars that come with top safety ratings, attractive looks and high-tech features

Tailoring software and design to the expectations of European customers, R&D is the hard edge of a commercial strategy to overcome the lack of brand recognition

New brands as yet unknown in Europe such as Aiways, BYD, JAC, NIO, Great Wall, Hongqi, Seres and Xpeng expect 2023 to be a 'make-or-break' year for their export push

After the poor launch performances, 15 years ago, marred by quality and security incidents, car safety has been a focus shared across Chinese manufacturers to establish a reputation for reliability

The European New Car Assessment Programme (NCAP) has become the prize to achieve credibility in the European market

So much so that two Chinese Euro NCAP testing facilities - in Chongqing’s Liangjing New Area (in 2019 and a first for Euro NCAP test facility outside Europe) and in Tianjin (2021) - have been accredited to enable Chinese carmakers to finetune their vehicles

A five-star European NCAP rating requires loading vehicles with active and passive safety features (such as extra airbags to collision avoidance, driver-assistance and driver-monitoring systems) going beyond legal requirements

Achieved by numerous cars in the line-up of each Chinese car manufacturer, the five-star rating demonstrates a commitment to stand up against marquee global brands

Significantly, the high safety ratings also open up the potentially large corporate car fleet and rental market for Chinese EVs, such German Sixt's October 2022 commitment to buy approx. 100 000 of BYD's 5-star Atto 3 SUVs

Mercantilism 2.0

Mercantilism as economic policy took hold from the 15th to the 18th centuries in Europe's major trading nations

Designed to maximize the exports and minimize the imports for an economy, as a means to enrich the beneficiary country, mercantilism was the opposite of free trade

The paradox of Chinese global EV strategy resides in a mercantile support of the home industry in every way, built on an assumption of reasonably free international circulation of goods (importing basic materials and exporting high-value cars)

.A noteworthy achievement, the strategy rested on

- a gamble - to establish car electrification as the global transportation standard

- a large domestic market - to support the build-up of strong global contenders

Successful on both accounts, the strategy defines the framework of competition for the near future

Market opportunities do not look promising for the Western legacy carmakers

- leaving a gaping window of opportunity for China because the West is late in the EV game

- poorly represented in the all-important mid-price range for individual - as well as fleet - buyers

- hardly prepared for the aggressive pricing large volume EV makers will command with plants running to full capacity

- at risk of arbitrary availability (and pricing) for batteries - majority-controlled by Chinese competitors and weighing 40% in EV cost

It is early days in the US for electrical vehicles

Consumer skepticism about the technology and high import duties (25%) are setting back Chinese interest in the American market - providing breathing space to the US legacy carmakers to get their act together

No so in Europe where lower duties (10%) and strong consumer interest offer attractive venues to Chinese importers, keen to make the most of the opportunity

Chinese carmakers will be caught between their ambition to stamp global brand recognition on the European market and legitimate fear of the political backlash in the cards if (when ?) the European automotive industry is reduced to shambles

"Treading water" will be the subject of a forthcoming note