The old "global trade" order is coming to an end and the new world is waiting in the wings, still obscured by habit and reluctance to confront change

Germany’s manufacturing powerhouse is at a watershed and old certainties are cracking

The emergence of China on the global scene in 2001 had put a strong wind in the sails of Germany's export engine of cutting-edge industrial machinery and luxury cars, which reliably delivered economic growth year after year

The second phase of China's dominance - Trade China 2.0 targeting the entire value chain- has been gaining momentum, with deep forays in Germany's traditional industrial strengths

Germany has to find new venues for its vaunted manufacturing sector or to stand by as its traditional businesses are grinded to dust

In its economic guidance, Germany will need to address structural challenges on the domestic front and to recover its competitive edge on international markets

New ways of thinking remain stuck in limbo

To address both the domestic and the international dimensions of trade, Germany must lay out economic options to set the course of the country's future growth, and probably Europe's as well

- managing the long tail of slow but irreversible deindustrialization

- confronting China's explosive economic expansion to come....

From reliable client of German industrial perfection, from attentive student of its rigorous processes, China is today Germany's ceaseless competitor on global markets

A different matter altogether and a challenge of a very different magnitude...

China shock(s)

The German economic achievements in the early 2000's were inextricably linked to China's emergence as dominant exporter to the West

A division of labor of sorts entrusted China with the manufacturing of consumer goods on the grandest scale and Germany with the production of machinery tools and complex engineering, perfected over decades

From the mid-2000s to the end of the 2010s, German economy grew by 24% compared to French growth of 18%, and the technical superiority of its dense network of industrial firms seemed assured

In 2016, Chinese appliance giant Midea Group acquisition of premier German industrial robot manufacturer KUKA AG, a $5 billion takeover, could have flashed a warning for things to come

With German regulatory approval of the transaction in August 2016, the U.S. greenlighted the transaction on Dec. 30, 2016 (CFIUS and DDTC), a conveniently festive date for such a consequential decision...

Along with many other acquisitions, the KUKA deal mirrored the playbook laid-out in its successive 5-year industrial plans, the 2016-2020 'Made in China 2025' plan, the 14th 2021-2025 "Technological development' plan and the 15th plan (2026-2030) focused on 'self-reliance'

Strategic clarity on the Chinese end was met with what appears to have been complacency, self-confidence and incredulity in Germany and generally in the West

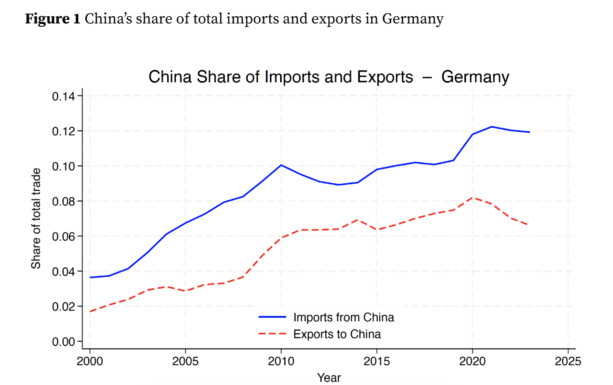

In the period 2001- 2007, the share of Chinese imports in total German imports doubled from 3.7% to 7.9%

Everything appeared fine since Germany's export share to China kept up, increasing by 227% from 3.3% of total German exports in 2007 to 7.5% in 2019

By 2020 however, China upended its trade pattern with Germany radically

Between 2020 and 2022 imports from China increased by more than 60%

The two core industries in Germany – cars and machinery tools – suffered a historic shift

- Car exports to China dramatically declined by almost 70% between 2022 and 2024

- A net importer of machinery tools from China since 2015, imports from China more than doubled between 2020 and 2022 and exports stagnated

The introduction of various disincentives (tariffs, termination of environmental bonuses on EVs) has curbed the growth of Chinese imports to Germany by 2024, only bringing global competition in sharper focus

With a strong and often dominant position across entire supply chains, China is competing with German exports globally, not just to China

The 2025 spurt in China's international trade expansion - a 2.0 export drive - has kept the country's economic growth on track in a difficult domestic environment

Initiated as a short-term cyclical adjustment, the market shares gained on export markets will cement durable dominance of Chinese brands

Germany is critically exposed because the German manufacturing sector is unusual by the size of the workforce – 5.5 million people – and its contribution to GDP – 18 to 20% - which remains much higher than for instance in France (11%)

Understandably Volkswagen, with major Chinese investments since the 1970's, and the German automotive lobby at large, could be a familiar sight in the corridors of the Berlin Bundeskanzlerambt, but not always for good reason

By lobbying on behalf of the Chinese interests of their industrial majors, German political authorities have been playing a dubious double game

Pushing persistently at the European Commission to keep trade with China open and free of tariffs, Germany voted against the modest anti-subsidy tariffs on Chinese car imports, as late as October 2024

Failing for years to take the measure of China's global forays in every export market, Germany finally might be ready to recognize the country's manufacturing jobs are at stake, impacted by market share losses across the world

Awareness of the giant sucking sound of de-industrialization has set the alarm bells ringing across manufacturing sectors everywhere

Caught on the backfoot, Western industrial strategies start out from a position of weakness

Credibility of global strategies, building on the strengths of Western industry to compete on equal terms with Chinese manufacturing giants in global markets, still takes a back seat to sovereign ambitions, one country at a time

Such delusions might leave all countries, and not just Germany, tragically unprepared

De-industrialization - writ large in four charts

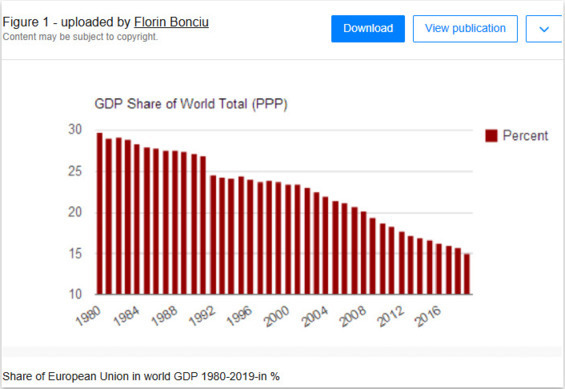

For comparison purposes, GDP weights by country must be estimated on “Purchasing Power Parity” (PPP) basis, equalizing the purchasing power of different currencies to eliminate differences in price levels between countries

Weight of the EU in world GDP dropped from 30% to approx. 20% in the two decades before China's WTO access between 1980 and 2001

The year 2002, with China's entry in the World Trade Organization (WTO), has been a breaking point in accelerating the downward trend

The European Union's share of World GDP dropped to approx. 14.3% In 2025 (again at PPP)

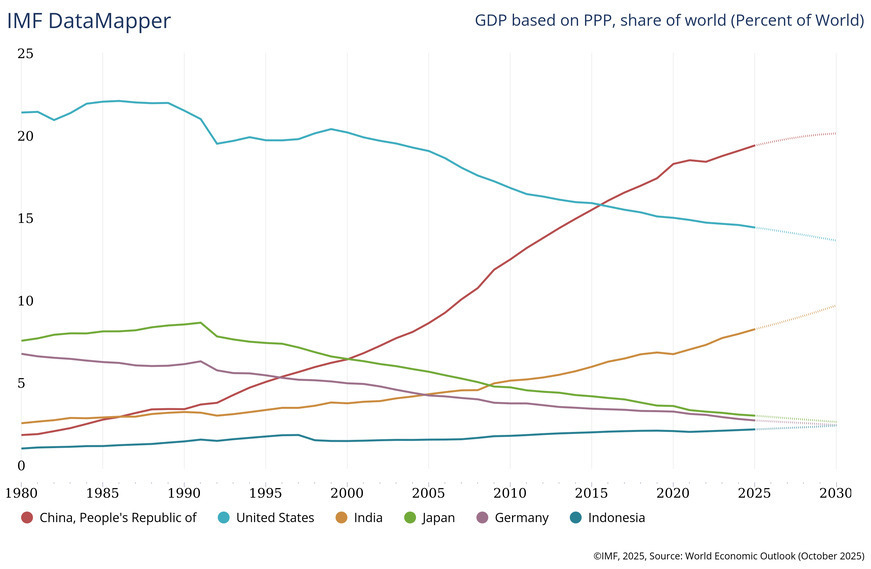

Germany's strength as manufacturing economy stood apart by holding on to a relatively stable global market share until 2001 at approx. 7% - just like industrial giants Japan (7.7%) and the U.S. (20% of world market share)

Trend lines of all three industrialized countries since 2001 - down to 3% for Germany and Japan - and to approx. 15% for the U.S. - reflect a profound rebalancing in relative weights, accounting for Chinese emergence on the world scene

The 2001 cliff following China's WTO entry signals either a lack of anticipation of the competitive challenge for Germany, Japan and the U.S. or, more probably, deliberate decisions to transfer manufacturing activities to China

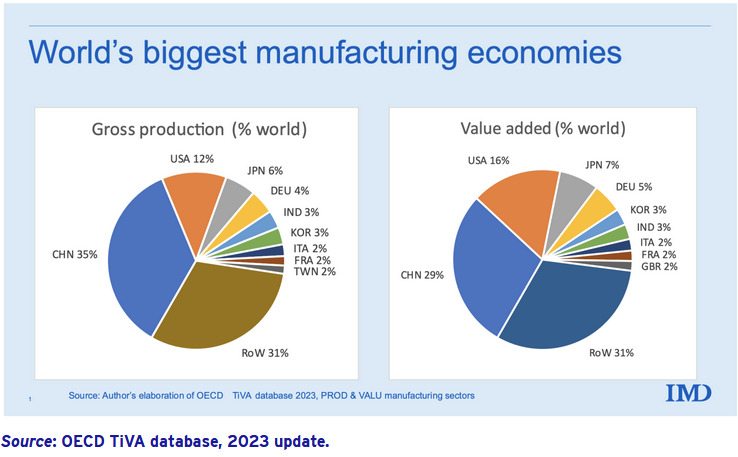

Gross production and value added in % of world offer a snapshot of the new balance of power (as of 2023), derived from such industrial arbitrage...one industrial relocation at a time

The data sets of country GDPs in Purchasing Power Parity and the chart of Value added (in % of World - above the right) are not the same but the observations are consistent

Germany is still leading the pack of EU economies by a wide margin - at 5% weighing more than 2 times its closest EU partners (France, Italy and the UK, each at 2%) but measured against Japan (7%), the country appears to be slipping...

China at 29% of World Value added and at 20% of World GDP in 2023 - up from approx. 3% in 1990 in World GDP statistical evidence - casts a very long shadow

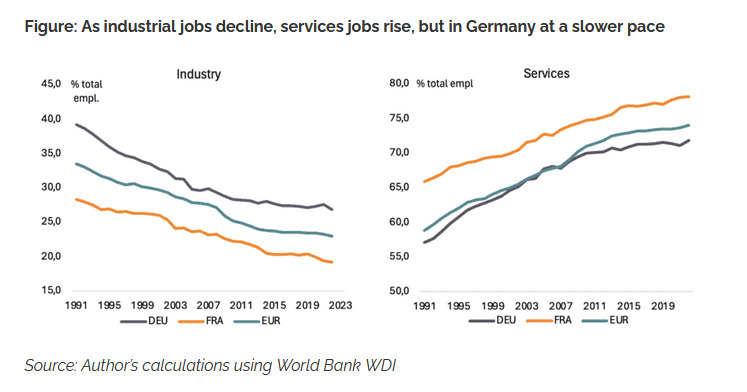

The decline of the share of manufacturing jobs in Germany, charted as DEU - dropping from 40% in 1990 to 27% (2023 data) - has been sharp in the 1990's, before the China 'shock' set in (chart on the left)

With a marked slowdown in industrial job losses since the early 2000's, Germany's industrial proved its resilience while its European competitors were battered

Germany has lost relative economic importance - but the drop from approx. 7% World GDP in 2001 to 3% did not impact the industry's volume significantly until 2023 (ignoring the sharp COVID-related fall)

This is about to change with the China shock 2.0 as jobs losses in automotive industries, in chemical concerns and in machine tool production are exposed to Chinese competition in Germany, in the European Union and across the world

What is to be done ?...in Germany and in Europe

What is to be done - to borrow the title from Lenin's 1901 pamphlet laying out the early formulation of the Bolshevik movement's plans - is multifaceted and necessarily flexible

- As discussed in Globalization, China and Trade Imbalance, the International Organizations, Trade and International Monetary Fund, need to be put to task to secure truthful Chinese trade statistics (they are not) and respect of commitments to which China subscribed upon acceding to the World Trade Organization (China does not)

- The European Union could mirror China's trade abuse, backhand subsidies, regulatory traps and technological transfer requirements on all the key industry segments the Continent needs to protect

- Sectors where no such protectionism is beneficial to the European industry (and consumers), no barriers should exist or be maintained (as for solar panels, where Chinese competition has eradicated European start-ups)

No global strategy is credible with the EU members - to say nothing of shared interests with Asian and Western countries in competition with China - if Germany is not fully on board...

Because Germany is not....a showdown is looming with its European partners

Germany's ambivalence is mirrored by the country's leading firms, in the car industry, in chemicals and pharmaceuticals, fully committed to expand their footprint in China

German companies - such as Volkswagen - lobbying at EU level for their Chinese interests are commendable for consistency with their own long-term interests, perceived as such

German interests within the EU and the interests of 'binational' companies, German in name but not always in act, do not overlap, whatever passport is carried by their CEO

Since countrywide strategies cannot gain much traction in the global context set out by China, a line needs to be drawn

None of this will be easy - and it all remains wrought with political risk

By laying out truthfully and crisply how the European economy will be supported in key sectors, targeting global markets (and which industries it will not), Europê could meet public understanding and appreciation

Ambivalent governments might be surprised ...